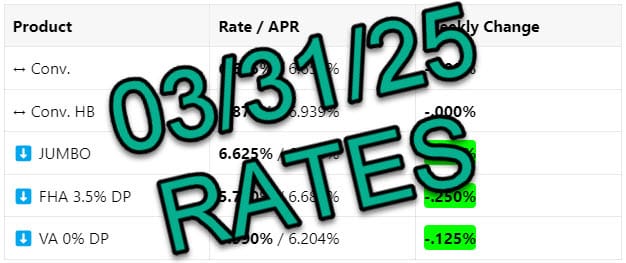

Mortgage Rates Ease ⬇️, Rocket To Purchase Mr. Cooper, Decades Party, Inflation Close But No Cigar.

Statement of Service for Active Duty Service Members

TECHNICAL

Statement of Service

Example Statement of Service

Understanding the Statement of Service for Active Duty Service Members: A Key Component in Home Loan Applications

For active duty service members, buying a home often comes with unique considerations and requirements. One essential document in this process is the Statement of Service (SOS). This document plays a critical role in verifying a service member’s active duty status and income stability, which are crucial for loan approval. Let’s dive into what a Statement of Service entails, why it’s needed, and how to ensure it’s completed correctly.

What Is a Statement of Service?

A Statement of Service is a formal document issued by the service member’s commanding officer or personnel office. It verifies specific details about their military service, including:

-

Full legal name

-

Social Security Number or service number

-

Branch of service

-

Rank and pay grade

-

Date of entry into active duty

-

Current duty status (e.g., active, reserve)

-

Expected discharge or separation date

-

Time lost (if applicable)

In essence, the SOS confirms a service member’s current standing in the military, their commitment level, and their ability to meet financial obligations over time.

Why Is It Required for a Home Loan?

When applying for a home loan, lenders need to assess the borrower’s financial stability and reliability. For active duty service members, the Statement of Service fulfills several key purposes:

1. Income Verification

The SOS helps lenders confirm a service member’s income. While many lenders also require Leave and Earnings Statements (LES), the SOS provides an additional layer of proof that the borrower is actively serving and receiving consistent pay.

2. VA Loan Eligibility

For those applying for a VA loan, the SOS is a required document. It helps establish eligibility for this benefit, ensuring that the applicant meets the service requirements to secure the loan.

3. Stability Assessment

Lenders want to know that borrowers have stable employment. The SOS assures lenders that the applicant is currently in good standing and unlikely to face interruptions in income due to military status.

4. Loan Underwriting

Underwriters need a comprehensive picture of the borrower’s financial and occupational situation. The SOS provides critical details that help them assess risk and determine loan terms.

How to Obtain a Statement of Service

Getting a Statement of Service typically involves requesting it from the appropriate office within your military branch. Follow these steps:

-

Contact Your Chain of Command or Personnel Office

Request the SOS through your unit’s administrative office or personnel support center. -

Ensure It Includes Required Information

Verify that all essential details are included. Missing information can delay the loan process. -

Provide to Your Lender

Submit the completed SOS to your loan officer promptly to avoid processing delays.

Tips for a Smooth Home Loan Process

-

Start Early: Request the SOS as soon as you start considering a home loan. Processing times can vary, especially in busy units.

-

Work with a Knowledgeable Lender: Choose a lender familiar with VA loans or working with military borrowers. They can guide you through the documentation process.

-

Keep Copies: Always keep a personal copy of your SOS for your records.

The Bottom Line

The Statement of Service is more than just a formality—it’s a vital document that ensures lenders have the information they need to approve your home loan. By understanding its importance and preparing ahead, active duty service members can navigate the home-buying process with confidence and secure the home of their dreams.

If you’re an active duty service member considering a home purchase, partnering with a mortgage expert experienced in military loans can make all the difference. Take the first step toward homeownership today!

Related Posts