Introduction With the Independence Day holiday just around the corner, many homeowners are considering home…

How to Read Scary Economic Headlines Without Panicking About Mortgage Rates

The news looks terrifying. Your phone is blowing up. Here is what is actually going on.

Whether you are a homebuyer trying to figure out if now is the right time to lock in a rate, or a Realtor fielding calls from nervous clients, you have probably noticed that scary economic headlines and actual mortgage rate movement do not always line up the way you would expect.

A massive jobs report drops. Inflation spikes to a two-year high. And mortgage rates… barely move. Or they move in the opposite direction of what every article predicted. It is confusing, it is frustrating, and it makes it really hard to make confident decisions.

I have been in the mortgage industry for years, and I want to give you a framework for understanding what is actually happening when the economic news cycle goes haywire. Not financial jargon. Not a lecture. Just a practical way to read the market that will make you more confident, whether you are sitting across from a lender or sitting across from a buyer.

Why Mortgage Rates Do Not Always React the Way You Expect

Here is the first thing most people get wrong. They assume mortgage rates move directly with whatever scary number just dropped. Hot inflation report? Rates must spike. Weak jobs report? Rates must fall.

It almost never works that cleanly.

Mortgage rates are driven by the bond market, specifically by mortgage-ba

cked securities and the 10-year Treasury yield. The investors trading in that market are not just reacting to today’s number. They are thinking about what the Federal Reserve will do next, how long current conditions will last, and whether the data actually signals a real change in the economy or is just temporary noise.

That distinction between a real signal and temporary noise is everything.

When a shocking number drops and the market shrugs, it is usually because traders have already priced in the expectation, or because they can see that the underlying data does not support the scary headline. Understanding that dynamic will save you from making decisions based on fear rather than facts.

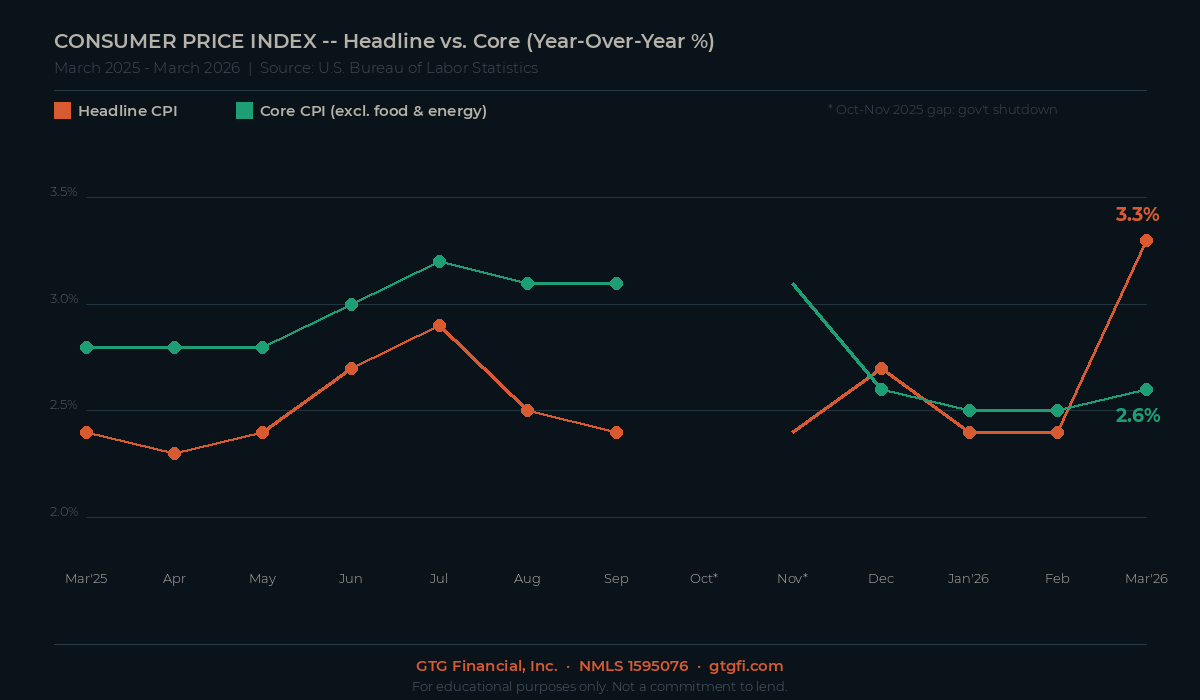

Headline Inflation vs. Core Inflation: Why the Difference Matters to You

One of the most practical things anyone in the housing market can understand right now is the difference between headline inflation and core inflation.

Headline inflation measures everything, including gas and food prices. Core infla

tion strips those out and focuses on the broader price trends in the economy.

Why does that distinction matter? Because gas and food prices are volatile. They can spike dramatically in a single month because of a supply disruption, a geopolitical event, or a hurricane, and then reverse just as fast. The Federal Reserve knows this, which is why they pay much closer attention to core inflation when deciding whether to raise or cut interest rates.

For homebuyers: When you see an alarming inflation headline, before you put your home search on hold, ask whether the spike is coming from energy prices or from something more deeply rooted in the economy. If gas prices drove the headline and core inflation stayed relatively calm, the Fed is much less likely to take aggressive action, and mortgage rates have less reason to move dramatically.

For Realtors: This is one of the most powerful things you can explain to a nervous client. Walk them through the headline vs. core distinction and you immediately position yourself as someone who actually understands the market. That builds trust faster than almost anything else you can do.

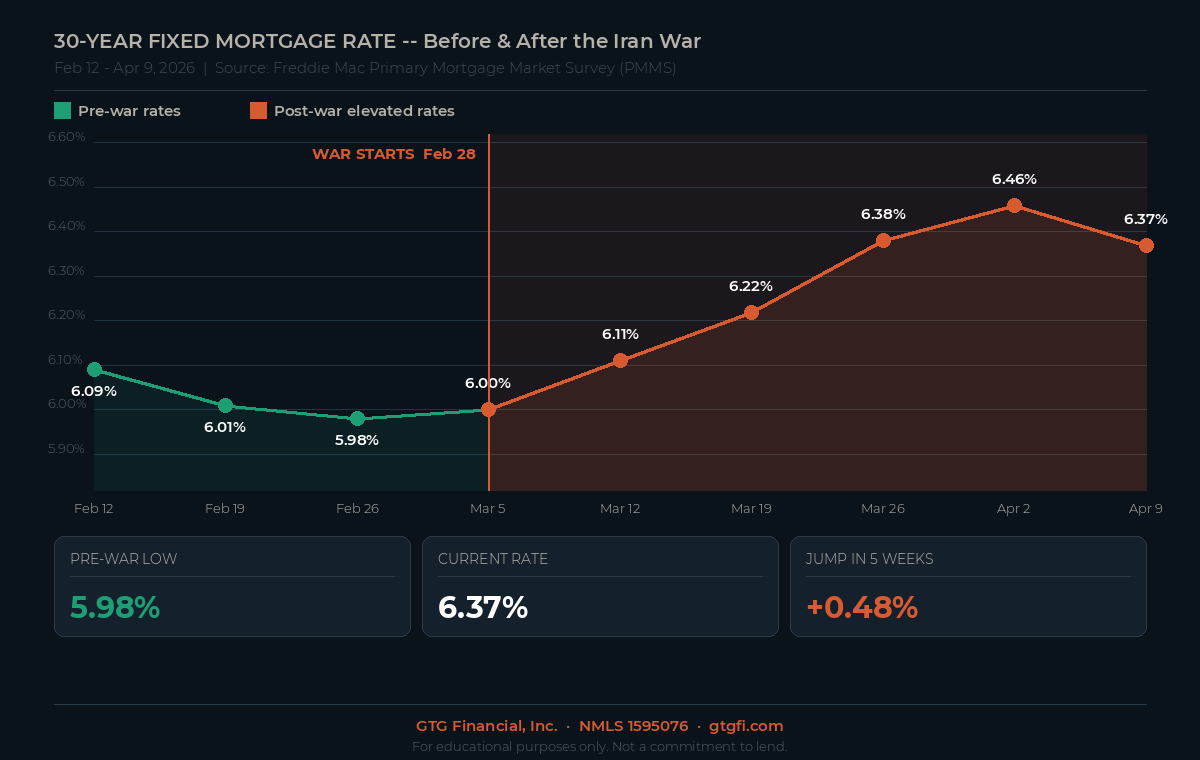

How Geopolitical Events Affect Your Mortgage Rate

Conflicts, sanctions, and supply disruptions can move mortgage rates in ways that feel random but actually follow a pretty consistent chain of events.

Here is how it works:

- A geopolitical event disrupts oil supply or creates global economic uncertainty

- Energy prices spike

- Inflation fears rise

- Investors sell Treasury bonds, fearing inflation will erode their returns

- Bond prices fall and yields rise

- Mortgage rates, which closely track the 10-year Treasury yield, move higher

The critical thing to understand is that this kind of rate pressure is often temporary. It is tied to a specific external event rather than a fundamental change in the health of the economy. When the situation resolves or markets adjust to a new reality, rates can normalize.

That does not make the higher rates any less real for buyers right now. But it does mean that making permanent decisions based on a temporary rate spike, whether that is panicking out of the market or deciding to wait indefinitely, is usually the wrong call.

The Jobs Report Is Not Always What It Looks Like

The monthly jobs report is one of the most watched economic releases in the country. It is also one of the most misread.

Here are a few things worth looking at beneath the headline number, whether you are a buyer trying to gauge the economy or a Realtor trying to advise your clients.

Where did the jobs come from? A big jump in employment is less meaningful if it is con

centrated in one sector, or if workers are simply returning from a strike rather than being newly hired. That is restoration, not growth.

What do the revisions say? Every month, the government quietly revises the prior two months of data. Those revisions can be significant, sometimes removing tens of thousands of jobs that were originally reported. The four-month trend tells a more honest story than any single headline.

How fast are wages growing? This is the number that actually matters most for inflation. Rising wages fuel consumer spending, which fuels price increases. When wage growth slows even in a month with strong job numbers, that is a quiet positive for the inflation picture and by extension for mortgage rates.

For Buyers: Why Waiting for the Perfect Rate Is Usually a Losing Strategy

I hear this from buyers constantly. “I’m going to wait until rates come down before I buy.” It feels like a smart, patient move. In most cases, it is not.

Here is the calculation most buyers are not running.

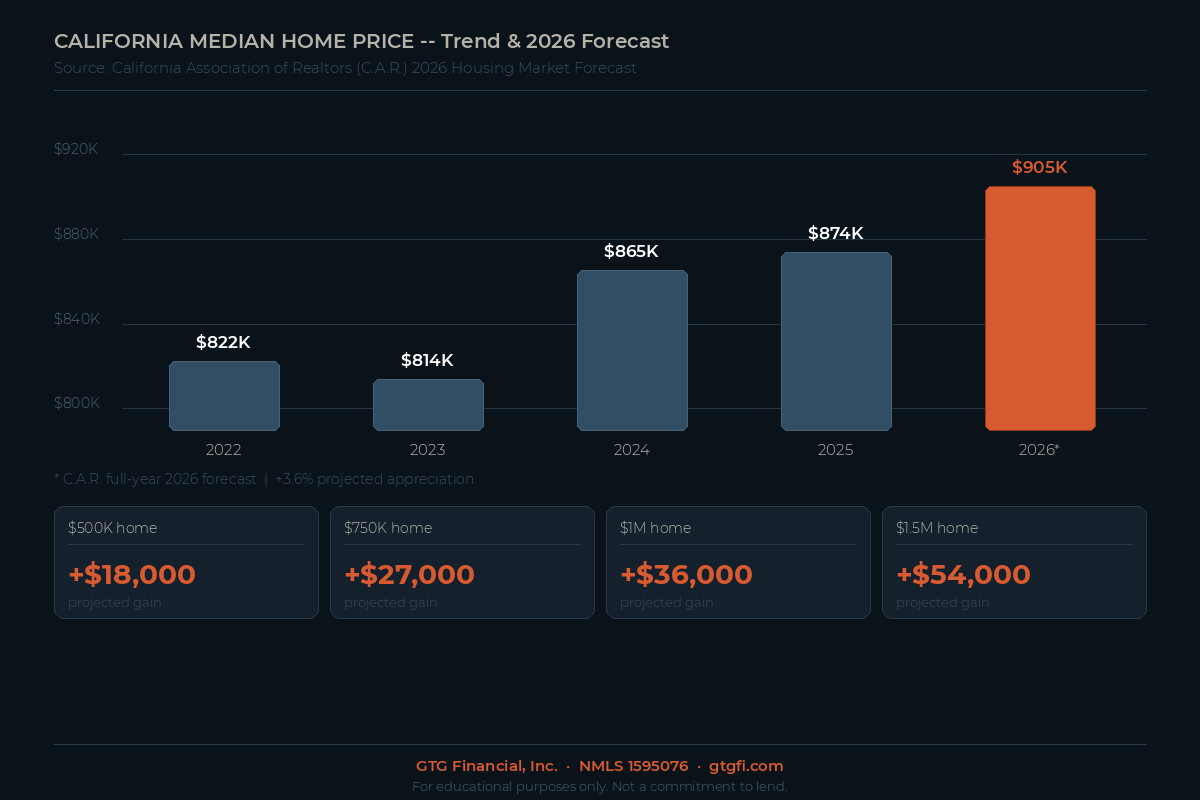

Home prices appreciate over time. In California, the California Association of Realtors projects home prices will rise 3.6% in 2026, reaching a projected record median of $905,000. On a $750,000 home, that is roughly $27,000 in equity growth in a single year, before you have done a single thing.

When you wait six months or a year hoping for a better rate, you are betting that the rate savings will outweigh the price increase on the home you are trying to buy. In most markets, most of the time, that math does not work in the buyer’s favor.

There is also the refinance option. Rates do not have to be perfect at the time of purchase. If you buy at today’s rate and rates drop meaningfully in the next two or three years, you refinance. You cannot go back and buy the same house at last year’s price.

The real question is not “what is the rate today?” It is “what does the cost of waiting actually look like for my specific situation?”

That is a conversation worth having with your lender before you decide to sit on the sidelines.

For Realtors: What to Tell Your Clients When the Market Feels Uncertain

When clients call in a panic over a scary headline, here is a simple framework that works every time.

Acknowledge the headline. Do not dismiss what they saw. It is real, it is in the news, and they are right to be paying attention. Dismissing their concern makes you look uninformed.

Put it in context. Explain the difference between the headline number and what is actually driving it. Is this a temporary energy spike or a systemic problem? Is core inflation calm even if the headline is loud? This is where your market knowledge becomes your competitive advantage.

Bring it back to their situation. Market conditions are interesting. Their timeline, their equity goals, and their financial picture are what actually matter. Help them think through their specific scenario rather than reacting to a national news cycle.

Give them a clear next step. Uncertainty paralyzes buyers. A clear, confident next step, whether that is getting pre-approved, connecting with a lender, or running the numbers on a specific property, gives them something to act on instead of something to worry about.

The Bottom Line

Economic headlines are designed to get your attention, not to help you make good decisions. The gap between what a headline says and what is actually happening in the mortgage market is often significant, and understanding that gap is one of the most valuable things you can do whether you are buying a home or helping someone else do it.

Rates move for specific reasons. Inflation data has layers worth understanding. And the cost of waiting for perfect conditions almost always outweighs the benefit.

The most confident buyers and the most effective Realtors I work with share one thing in common: they stay informed every week, not just when something scary happens.

Stay Ahead of the Market Every Week

Every Tuesday, I publish the GTG Weekly newsletter with a plain-English breakdown of what happened in the market, what it actually means, and what you should be talking to your clients or your lender about. No jargon. No noise. Just the information you need to make confident decisions.

It is free, and it takes about five minutes to read.

Subscribe at https://gtgweekly.beehiiv.com/

GTG Financial, Inc. | NMLS 1595076 | gtgfi.com | Equal Housing Opportunity

This post is for educational purposes only and does not constitute financial advice or a commitment to lend. Data referenced from Freddie Mac Primary Mortgage Market Survey®, California Association of Realtors, and the U.S. Bureau of Labor Statistics.

Related Posts