Introduction With the Independence Day holiday just around the corner, many homeowners are considering home…

Condo Mortgage California: How SB 326 Almost Killed the Deal

Deal Deep Dive | April 2026 | GTG Financial | Santa Rosa, CA

TL;DR: What’s in This Post

- What SB 326 is and why it matters for condo transactions in California

- Why a lender pumped the brakes on this $605,000 deal

- How a ratified HOA bid and a direct Fannie Mae submission got it done

- What a bigger lender would have done instead

- The condo insurance detail most buyers don’t think to ask about

- What realtors working with condo buyers need to know before the offer goes in

Most condo deals in California close without much drama. The HOA documents come in, the buyer reviews them, the lender checks the association’s financials, and the transaction moves forward. But there’s a layer of California condo law that catches buyers, realtors, and even some lenders off guard, and when it surfaces mid-transaction, the difference between a lender who knows how to navigate it and one who doesn’t is the difference between a deal that closes and one that doesn’t.

This is a deal where we were ten days from losing it entirely. Here’s what happened and how we got it done.

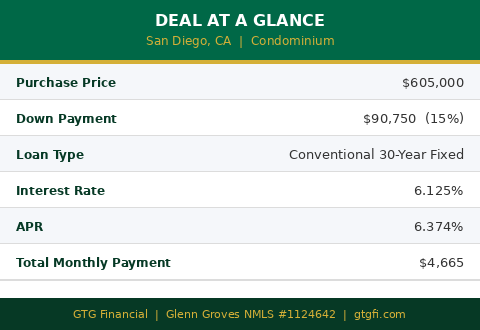

The Deal at a Glance

Example for educational purposes only. Not a commitment to lend. Subject to credit approval and underwriting. Rates and terms subject to change without notice. Individual rates vary based on credit profile, property type, occupancy, loan amount, and other factors.

Purchase price was $605,000 on a condominium in San Diego. The buyer came in with 15% down on a conventional 30-year fixed loan. We got them a 6.125% interest rate with an APR of 6.374%. Total monthly payment came out to $4,665, which breaks down across five line items: principal and interest at $3,124, homeowners insurance at $149, property taxes at $574, mortgage insurance at $167, and HOA dues at $650.

The homeowners insurance number is lower than you might expect on a $605,000 property, and that’s intentional. More on that later.

What SB 326 Is and Why It Matters for Condo Buyers

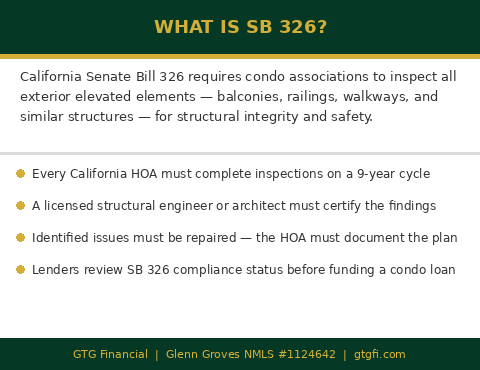

California Senate Bill 326 requires condo associations to inspect all exterior elevated elements on a 9-year cycle. That means balconies, railings, walkways, and similar structures. The inspection has to be performed by a licensed structural engineer or architect, any issues found have to be documented, and the HOA is responsible for getting those issues repaired. The law added Civil Code Section 5551 to the Davis-Stirling Act, which governs California HOAs.

The law was passed in response to structural failures that injured and killed residents. It’s a serious piece of legislation with real consequences for associations that don’t comply — associations that missed the January 2025 inspection deadline now face daily penalties and potential liability exposure. And it has a direct impact on condo transactions because lenders, following Fannie Mae and Freddie Mac guidelines, review SB 326 compliance status before funding a loan. For a plain-language overview of what the law requires, this summary from El Cerrito’s city government is a useful reference.

Most of the time this isn’t a problem. The HOA has completed its inspection, everything is in order, and the transaction moves forward. But there’s a specific scenario that creates real friction: when the HOA has completed the inspection, identified issues, has a repair plan in place, but the actual work hasn’t started yet. That’s exactly what we ran into here.

The Problem: Inspection Done, Work Not Started

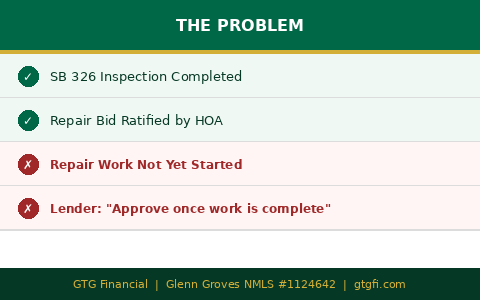

This association had done everything right. The SB 326 inspection was complete. They had a ratified repair bid from a contractor covering everything that was flagged. The work was scheduled to begin within two weeks. By any reasonable measure, the situation was under control.

The lender didn’t see it that way. Their position was straightforward: we can approve the loan once the work is completed. That doesn’t fly for a real estate timeline. Telling a buyer and seller to put a transaction on hold until a contractor finishes a repair scope of unknown duration isn’t a solution. It’s a dead end.

A bigger lender in this situation would have looked at the collateral, noted the open SB 326 items, and withdrawn the loan. The file would have been closed and the deal would have died. That’s not a criticism of every large institution, but it reflects the reality of how they operate at scale. Complex file, non-standard condition, no clear path through their system, move on.

The Fix: A Ratified Bid and a Direct Line to Fannie Mae

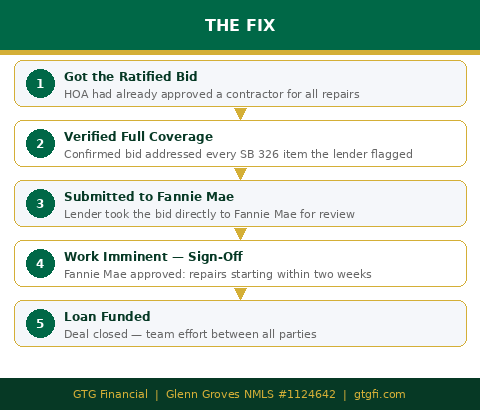

We went back to the HOA and pulled the ratified bid they already had. This was a formal, signed agreement between the association and the contractor covering every item that showed up on the SB 326 inspection. We went through it line by line to confirm every flagged item was accounted for in the repair scope.

With that documentation in hand, we submitted it directly to Fannie Mae. Not through a standard underwriting channel with a note attached. Directly to Fannie Mae for review. The question we were asking them to answer was this: given that the work is imminent and the full scope is contractually committed, can the loan fund now?

They said yes. Because the work was scheduled to begin within two weeks and the repair commitment was fully documented, Fannie Mae signed off on the loan funding ahead of completion. We closed the deal.

It was a team effort. Everybody involved, listing agent, buyer’s agent, great communication. We put the puzzle together and got the deal done.

The Condo Insurance Detail Most Buyers Miss

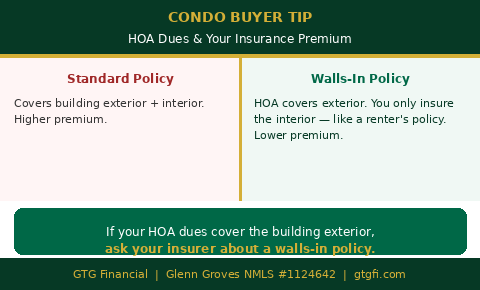

I mentioned the homeowners insurance number on this deal was $149 a month, which is lower than most people expect on a $605,000 property. The reason is the HOA dues.

At $650 a month, this association’s dues are covering the building exterior. That’s standard for a condo association of this size. When the HOA covers the exterior, the buyer doesn’t need a standard homeowners policy that covers everything. They need what’s called a walls-in policy, sometimes called an HO-6. It’s essentially a glorified renter’s policy. It covers your personal property, your interior finishes, and your liability. It does not cover the building exterior because the HOA already does.

The result is a significantly lower insurance premium. Most buyers don’t ask about this when they’re running numbers on a condo purchase. It’s worth asking about, because it can meaningfully change the payment picture.

What Condo Buyers and Realtors Need to Know in Sonoma County

SB 326 compliance issues aren’t rare. Condo associations throughout California are at various stages of their inspection and repair cycles. In Sonoma County, where a meaningful portion of the condo inventory was built in the 1980s and 1990s, associations are actively working through their SB 326 obligations right now.

If you’re a buyer writing an offer on a condo, SB 326 status should be part of your due diligence conversation before the offer goes in. The HOA documents will tell you where the association stands. What they won’t always tell you is how your lender is going to respond to what they find there.

If you’re a realtor working with condo buyers, the question to ask your lender before an offer is simple: how do you handle SB 326 compliance issues if the inspection has been done but the repairs aren’t complete yet? The answer to that question tells you a lot about whether that lender is going to get your buyer to the finish line or hand the file back two weeks before closing.

This deal was saved because we knew the question to ask Fannie Mae and we had the documentation to back it up. That’s the difference between a lender who knows the program and one who doesn’t. If you have a condo deal in Sonoma County or anywhere in the North Bay and you want to understand what the HOA compliance picture looks like before you’re in the middle of it, reach out. That’s the kind of conversation worth having before the offer is written.

Glenn Groves

Mortgage Broker | GTG Financial | Santa Rosa, CA

NMLS #1124642 | gtgfi.com

GTG Financial, Inc. NMLS #1595076 | CA DRE #02029711. Equal Housing Opportunity. Example for educational purposes only. Not a commitment to lend. Subject to credit approval and underwriting. Rates and terms subject to change without notice. Individual rates vary based on credit profile, property type, occupancy, loan amount, and other factors. nmls consumeraccess.org

Related Posts