Introduction As the end of July approaches, many families are preparing for the back-to-school season.…

You Don’t Need 20% Down: What You Actually Need to Buy a Home

Evergreen | May 2026 | GTG Financial | Santa Rosa, CA

TL;DR: What’s in This Post

- The actual minimum down payments for VA, FHA, and conventional loans

- Why maxing out your down payment is not always the right call

- What every $1,000 in down payment will likely do to your monthly payment

- How mortgage insurance pricing buckets typically work and why crossing a threshold matters more than the exact percentage

- Why keeping cash liquid after closing is part of a healthy purchase plan

The 20% down payment myth is one of the most stubborn pieces of misinformation in real estate. It shows up constantly. Buyers think they need to save for years before they can even consider buying, when in reality they could have been in a home long ago. This post breaks down what the actual numbers look like and why maxing out your down payment is not always the right call.

What You Actually Need to Buy a Home

Let’s start with the basics. If you are using a VA or USDA loan, the minimum down payment is zero. Nothing. You can purchase a home with no money down if you qualify for either of those programs. VA is for eligible veterans and service members. USDA covers certain rural areas and has income limits, but it is a real option for a lot of buyers who do not know it exists.

If you are using FHA, the minimum is 3.5% down. One thing that surprises a lot of people: you do not have to be a first-time homebuyer to use FHA. The main requirement is that the property has to be a primary residence. That opens it up to a much wider range of buyers than most realize.

On the conventional side, first-time buyers can access programs with as little as 3% down through products like Fannie Mae HomeReady and Freddie Mac Home Possible. For everyone else, the standard conventional minimum is 5% down. Either way, you are nowhere near 20%.

In practice, most buyers we work with end up somewhere between 5% and 10% down. That range tends to hit the sweet spot between a manageable payment and keeping enough cash on hand after closing.

The Case Against Maxing Out Your Down Payment

Sometimes we work with buyers who have the ability to put 20 or 25% down, and they choose not to. That is not a mistake. It is a deliberate decision based on how they want to structure their finances.

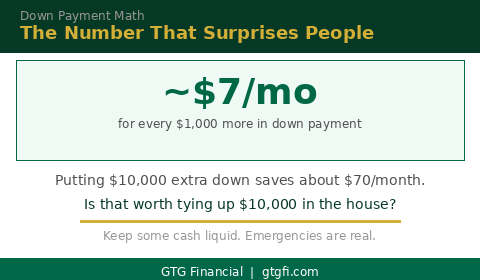

Here is the number that tends to change how people think about this: every $1,000 you put toward a down payment will likely affect your monthly payment by roughly $7. So if you are deciding whether to put an extra $10,000 into the down payment, you are probably looking at roughly $70 less per month in exchange for tying up $10,000 in the house. For a lot of people, that trade does not make sense.

We do not want buyers spending every last dollar to buy a house. It is a bad idea to tie all of your money up in equity, because getting that money back out is much harder and slower than most people expect. A home equity loan takes time and qualification. A savings account is just there. Keeping some cash liquid after closing is part of a healthy purchase plan, not a sign that you under-prepared.

How Mortgage Insurance Pricing Actually Works

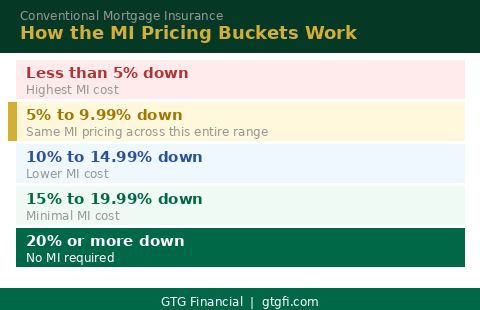

If you are putting less than 20% down on a conventional loan, you will typically have mortgage insurance. Mortgage insurance is often treated like a dirty word, but understanding how it is priced takes most of the fear out of it.

MI pricing on a conventional loan is generally driven by two factors: how much you are putting down and what your FICO score is. The down payment side typically works in buckets. Putting 5% down and putting 9.99% down will often land you in the same MI pricing bucket. It is crossing into a new threshold that tends to change what you pay.

This matters because people sometimes assume that every dollar toward the down payment is improving their mortgage insurance rate. That is not how it works. You want to be thoughtful about which threshold you are targeting and whether the extra cash to get there is worth it compared to what you would save on MI. Sometimes it is. Sometimes the money is more useful sitting in your account.

The other factor is your FICO score. A higher score can offset a lower down payment when it comes to MI pricing. A buyer with an 800 FICO putting 5% down will generally see a much better MI rate than someone with a 640 FICO putting 5% down. These variables work together, and the right structure depends on the specific numbers in front of us.

Run the Numbers Before You Decide

The right down payment for you is not a universal answer. It is a function of your income, your reserves, your FICO score, the loan program you are using, and what you are trying to accomplish financially. The 20% benchmark made more sense in a different lending environment. Today it is largely just noise.

What I tell buyers is to look at what the payment looks like at 5%, 10%, and 20% down and then make a decision with real numbers in front of them. Most of the time, the difference is smaller than they expected, and they end up choosing something in the 5 to 10% range that leaves them with liquidity and a payment they are comfortable with.

Every $1,000 you throw at the down payment moves the monthly by about seven bucks. That’s it.

If you are in Sonoma County or the North Bay and you want to run through what the actual numbers look like for your situation, reach out. That conversation is free and usually pretty eye-opening.

Glenn Groves

Mortgage Broker | GTG Financial | Santa Rosa, CA

NMLS #1124642 | gtgfi.com

GTG Financial, Inc. NMLS #1595076 | CA DRE #02029711. Equal Housing Opportunity. Not a commitment to lend. Subject to credit approval and underwriting. Rates and terms subject to change without notice. Individual rates vary based on credit profile, property type, occupancy, loan amount, and other factors. nmls consumeraccess.org

Related Posts