Understanding the Summer Housing Market The summer months, stretching from the Fourth of July to…

The VA IRRRL – How the Streamline Refi Really Works

July 2026 | GTG Financial | Santa Rosa, CA

TL;DR: What’s in This Post

- What a VA IRRRL (the streamline refi) is, and what it skips

- Why the “4% refi” offers flooding your mailbox are usually a trap

- How a real no-cost refinance actually works

- A Santa Rosa example: a full percent lower, nothing added to the loan

If you are a veteran, your mailbox is probably full of offers promising to get you a rate “right in the fours.” Most of it is smoke. A VA IRRRL, the VA’s streamline refinance, is a genuinely useful tool. But it only helps when the math actually works in your favor, and the versions arriving in your mailbox usually make sure it does not. Here is how it really works, plus a recent Santa Rosa example.

What a VA IRRRL Actually Is

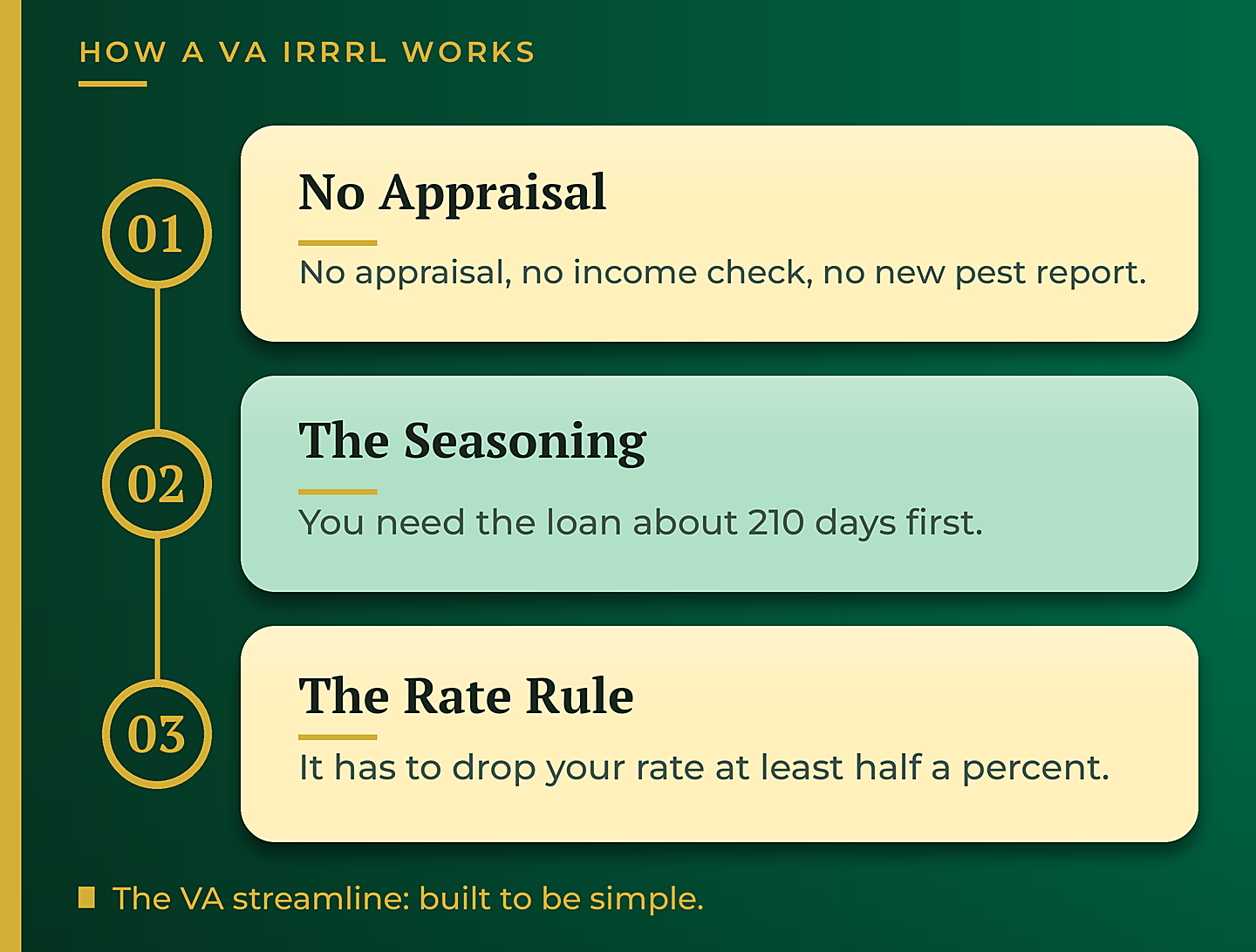

A VA IRRRL, short for Interest Rate Reduction Refinance Loan, is one of the simplest refinances in the business. There is no appraisal, no income verification, and no new pest report. Because there is so little to check, it can move quickly.

To qualify, you generally need to have had the loan about 210 days, roughly seven months, and the new loan has to lower your interest rate by at least half a percent. That is essentially it. The whole point of the program is to make it easy for a veteran to lower the rate on an existing VA loan without jumping through the hoops of a full refinance.

Why the “4% Refi” Spam Mail Is a Trap

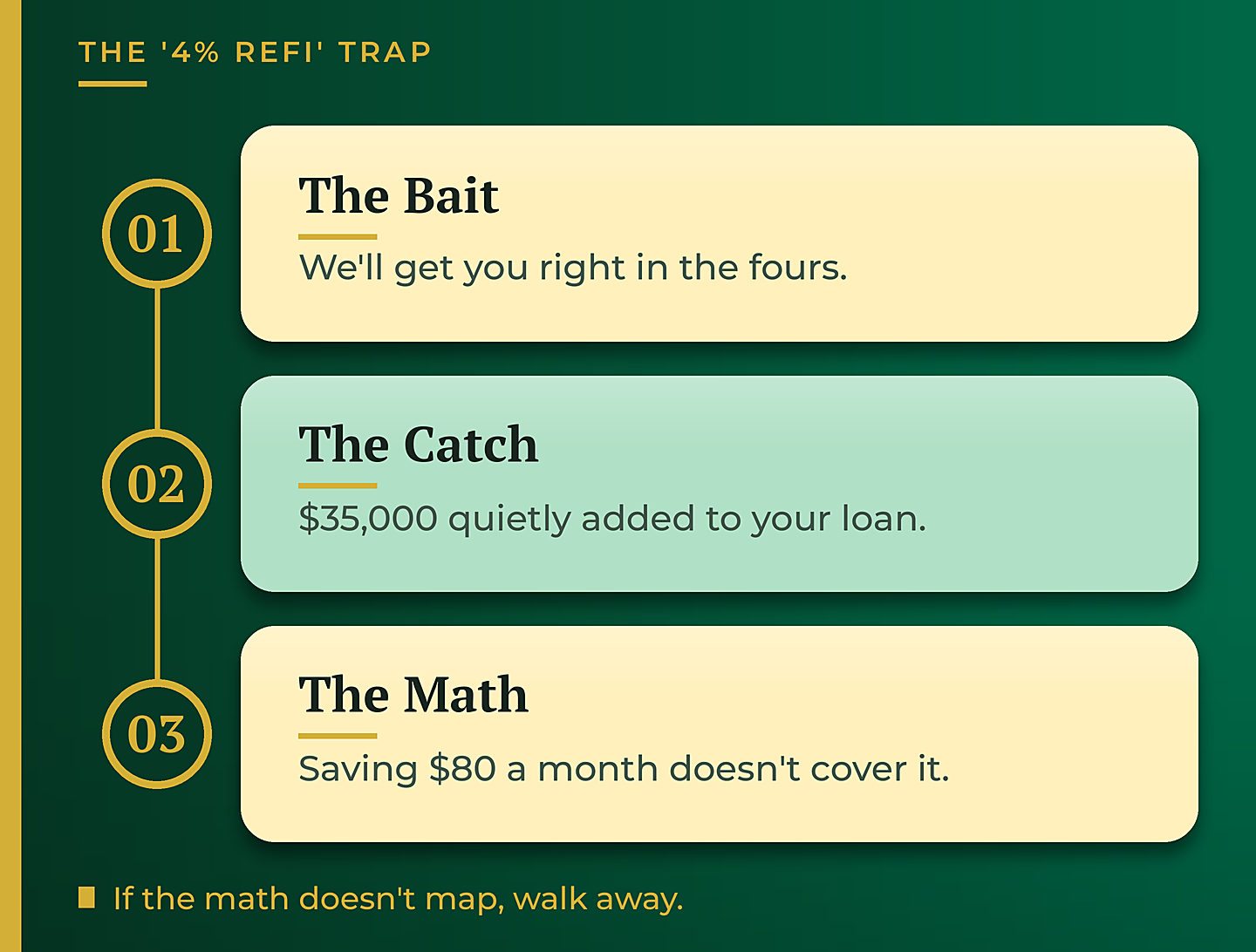

Veterans get hammered with mailers promising a rate in the fours. Here is the catch: those eye-catching rates almost always come with a large cost baked into the loan. You take the low rate, and suddenly your balance is $35,000 higher than it was.

The pitch is always the same. “Aren’t you glad you’re saving $80 a month?” But add $35,000 to your loan to save $80 a month, and the math simply does not map. Any time a refinance offer buries the cost inside your balance instead of putting it in front of you, that is your signal to slow down and add it up.

The No-Cost Way to Do It: A Santa Rosa Example

Here is how we ran a recent one in Santa Rosa. The loan was about $650,000. We could have chased the absolute lowest rate on the sheet, but instead we opted for a mid-tier rate and had the lender cover roughly $5,000 in closing costs. That way, nothing got piled onto the balance.

The result: we dropped their rate by about a full percent, saving them hundreds of dollars a month, with no cost added to the loan. That is the whole difference between a refinance that genuinely helps you and one that just relocates your problem into your balance.

Rates shown are for illustrative purposes only and do not represent current available rates. Contact Glenn Groves for current rate information.

When It Makes Sense (and When to Wait)

The right structure depends entirely on the person. This particular borrower is planning to sell in about two years, so the no-cost approach mattered even more. There was money on the table today, and no reason to eat into their future profit by adding to the loan for a rate they will only keep for a short while.

For a veteran planning to stay long term, a slightly lower rate that carries some cost might pencil out better over time. The point is never to chase a headline number. It is to run your specific situation and pick the option that actually leaves you ahead.

The Bigger Picture

A VA IRRRL is a real benefit you earned through your service. But the version that shows up in your mailbox is engineered to look great on the outside and cost you on the inside. Done right, a streamline refinance lowers your payment without quietly growing your loan.

If you are a veteran wondering whether now is the time, it is worth a short conversation to run the actual math on your loan. The answer might be yes, it might be not yet, but either way you will know instead of guessing off a postcard.

Glenn Groves

Mortgage Broker | GTG Financial | Santa Rosa, CA

NMLS #1124642 | gtgfi.com

Rates shown are for illustrative purposes only and do not represent current available rates. Contact Glenn Groves for current rate information. VA IRRRL eligibility and terms are subject to VA guidelines. GTG Financial, Inc. NMLS #1595076 | CA DRE #02029711. Equal Housing Opportunity. Not a commitment to lend. Subject to credit approval and underwriting. nmls consumeraccess.org

Related Posts