Understanding the Impact of Hurricane Season on Homeownership As we approach the peak of hurricane…

What I Tell Realtors Who Push Back on VA Buyers

VA Loan Series | May 2026 | GTG Financial | Santa Rosa, CA

TL;DR: What’s in This Post

- Where VA loan myths actually come from

- What a VA inspection really involves

- Why veterans have the lowest default rate of any major loan product

- What to say when a realtor pushes back on a VA offer

- Why working with the right lender changes everything

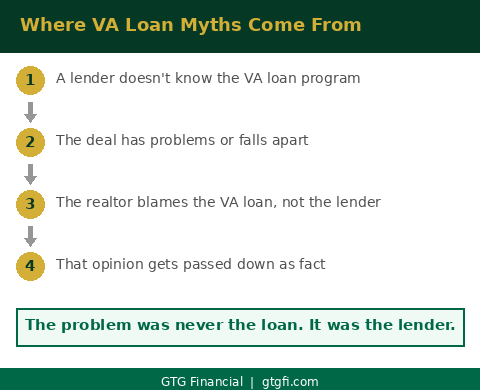

If you’ve spent any time working with realtors as a veteran buyer, you’ve probably run into it. The hesitation. The subtle suggestion that maybe a conventional offer would be stronger. The reputation that VA home loans are complicated, slow, or hard to close. I’ve heard every version of it, and after years in this business, I can tell you exactly where it comes from. Almost always, it traces back to one bad experience with a lender who didn’t know what they were doing. The problem was never the loan. It was the lender.

Where VA Loan Myths Come From

There’s a lot of bad information out there about VA loans, and most of it spreads the same way. A lender who doesn’t know the program takes on a VA file. The deal runs into problems. The realtor on the other side has a rough experience, blames the loan type, and carries that opinion into every future transaction. By the time it reaches you as a buyer, it’s been passed down as established fact.

The thing is, when VA loans are done correctly, they’re just as easy to work with as most other loan programs. The issue isn’t the loan. It’s whether the lender on the file actually knows how to work it. A lender who understands VA guidelines, communicates proactively, and knows how to navigate the process doesn’t create the kind of experience that turns into a myth. A lender who doesn’t, does.

So when a realtor tells you VA loans are difficult, the right question is: what was your bad experience, and who was the lender? That answer usually tells you everything.

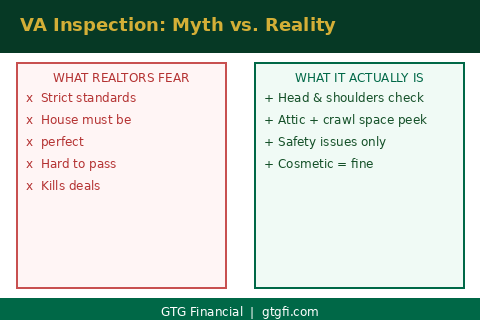

What a VA Inspection Actually Involves

One of the most persistent VA loan myths is that the appraisal and inspection process is unusually strict. That the house has to be in perfect condition. That any minor issue will kill the deal. I hear this constantly, and it’s just not accurate.

What actually happens is a head and shoulders check. The appraiser sticks their head up into the attic and looks around. If there’s a crawl space, they check that too. They’re looking for obvious structural or safety issues. Exposed wiring. Active moisture intrusion. Significant structural problems. Things that, honestly, should probably be addressed on any property regardless of loan type.

Cosmetic issues don’t factor in. A dated kitchen, worn carpet, paint that needs refreshing. None of that will hold up a VA appraisal. The standard is livability and safety, not perfection. If a property has issues that would fail a VA appraisal, it probably has issues a buyer shouldn’t be ignoring on any loan.

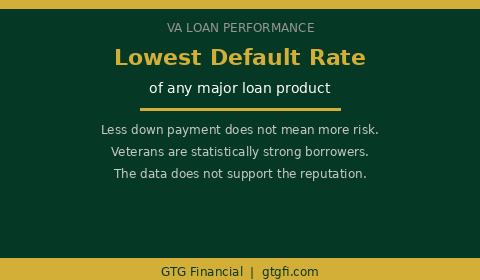

Veterans Are Not a Higher-Risk Borrower Category

A lot of VA loan pushback is built on the idea that a veteran putting less money down is somehow a weaker buyer. That a seller accepting a VA offer is taking on more risk than they would with a conventional buyer. The numbers don’t back that up.

VA loans have an incredibly low default rate compared to all other major loan products on the market. Veterans are not a higher-risk borrower category. The program exists because veterans have earned it, and the repayment history backs that up. A veteran with a VA offer is not a riskier buyer. In a lot of cases, they’re a stronger one.

The next time a realtor suggests that a VA offer puts a seller at a disadvantage, that’s a myth worth challenging directly. The numbers say otherwise.

What to Do When a Realtor Pushes Back on Your VA Offer

If you’re a veteran and you’ve run into resistance from a realtor, the move is simple. Ask them what their experience with VA loans has been and who the lender was. Nine times out of ten, their objection is with a specific lender’s execution, not with the loan itself.

I’m also happy to be a resource for realtors who have had rough VA experiences. Not to steal a deal from another lender, but because I think proper communication and clarity go a long way. If I can explain why something was handled a certain way, or walk through how we approach VA files, that’s a conversation worth having. Realtors who understand how a well-run VA loan works don’t push back on VA buyers.

Those that say VA loans are more difficult to work with, I would challenge that with: what’s your bad experience, and why is that now your opinion? Let me show you how to do it the right way.

If you’re a veteran ready to use your VA home loan benefit in Sonoma County or the North Bay, or a realtor who wants to understand how the process actually works when it’s done right, reach out. That’s exactly the kind of conversation we’re built for.

Glenn Groves

Mortgage Broker | GTG Financial | Santa Rosa, CA

NMLS #1124642 | gtgfi.com

GTG Financial, Inc. NMLS #1595076 | CA DRE #02029711. Equal Housing Opportunity. Not a commitment to lend. Subject to credit approval and underwriting. Rates and terms subject to change without notice. Individual rates vary based on credit profile, property type, occupancy, loan amount, and other factors. nmls consumeraccess.org

Related Posts