Introduction As the end of July approaches, many families are preparing for the back-to-school season.…

You Can Use Your VA Loan More Than Once

VA Loan Series | May 2026 | GTG Financial | Santa Rosa, CA

TL;DR: What’s in This Post

- Why most veterans think their VA loan is a one-time benefit, and why that’s wrong

- How VA entitlement actually works across multiple properties

- What one-time restoration is and how to use it

- What happens after one-time restoration is used

- Why forward planning around your entitlement matters more than most veterans realize

There’s a widely held belief among veterans that the VA loan is something you use once. You buy your house, you use your benefit, and that’s the end of it. I understand why that belief exists. The VA loan is marketed as a benefit, and benefits tend to feel finite. But the reality of how VA entitlement works is a lot more flexible than most veterans are ever told, and that gap has cost people a significant amount of money over the years.

The biggest mistake I see veterans make with their entitlement is not understanding that the VA loan can be used multiple times, across multiple properties, while still carrying each one. The second mistake is not thinking far enough ahead to plan how to use it.

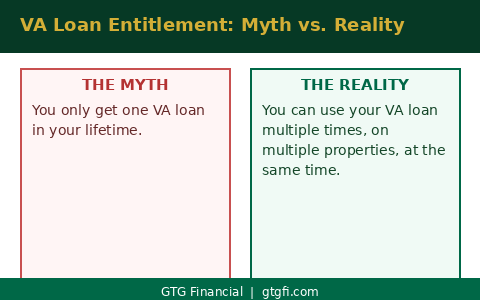

The Myth: One VA Loan, One Time

The myth is simple: you only get one VA loan in your lifetime. Use it, and it’s gone. That’s not accurate. VA entitlement isn’t a single-use coupon. It’s a benefit you can deploy on multiple properties at the same time, and it can be restored and reused under the right conditions.

Where the myth comes from is understandable. If you use your full entitlement on one home, it can feel like the benefit is spent. And in a narrow sense, that’s true. The portion of your entitlement tied to that property isn’t available for a new purchase without some action on your part. But the entitlement itself is still yours. The mechanics of accessing it again are just what most veterans are never told about.

How VA Entitlement Actually Works

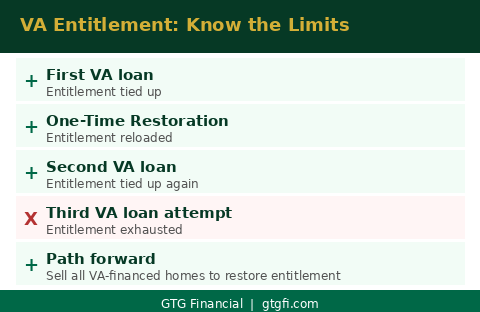

When you purchase a home using your VA loan, a portion of your entitlement is committed to that property. Think of it as being tied up rather than used up. You still own the benefit. You just can’t deploy that specific portion again until the underlying obligation changes.

Here’s what that looks like in practice. You buy your first home with your VA loan and tie up a chunk of your entitlement. You later want to buy a second primary residence, maybe a PCS move, a job change, a growing family. You can use whatever entitlement remains to purchase that second home while still holding the first. Most veterans don’t know this part. You don’t have to sell the first home to use your VA loan again. You can carry both properties at the same time, with different portions of your entitlement allocated to each.

The strategic question is what happens next, and what your options are when you want to free up entitlement that’s already committed.

One-Time Restoration: The Tool Most Veterans Never Hear About

I’ll be honest: I didn’t learn about one-time restoration until later in my career, when I ran into it on a deal. It doesn’t come up in most VA loan conversations, and that’s a problem, because it’s one of the most powerful tools a veteran has for managing their entitlement over time.

Here’s how it works. If you have a home with a VA loan on it and you want to free up that portion of your entitlement, you can refinance that property into a conventional loan. The VA loan is paid off, the property is now carrying a conventional mortgage, and that chunk of entitlement is released. You can then apply for what’s called a one-time restoration, which formally reloads your entitlement back to full.

The name tells you the limitation: you can only do it one time. One refinance-and-restore sequence per lifetime. If you use your reloaded entitlement on another property and later want to free that up the same way, the one-time restoration option is gone. Your entitlement stays committed until you sell all homes that have ever carried a VA loan, regardless of whether they’ve since been refinanced into conventional.

What Happens After One-Time Restoration Is Used

This is the part that matters most for long-term planning. After one-time restoration is used, the math gets rigid. You can still use VA financing on a third property (the bonus entitlement concept, using whatever is left), but once that’s committed, there’s no way to reload it again short of selling every property that has ever had a VA loan on it. It doesn’t matter if those properties have been refinanced into conventional. The VA tracks the history, not just the current loan type.

The way I look at it, it’s kind of like a shell game, completely legal, but one that requires you to think several moves ahead. The veterans who get the most out of their entitlement are the ones who understood early that this benefit is a long-term strategic asset, not just a transaction.

It really takes future planning to understand how to leverage your entitlement to the highest and best use.

What Veterans in Sonoma County Should Be Thinking About

In a market like Sonoma County, where median home prices sit around $850,000, the stakes around entitlement planning are high. A veteran who saves their entitlement, or restores it strategically, can purchase a home at that price point with zero down payment and no mortgage insurance. That’s a significant financial advantage. A veteran who used their entitlement without a plan and exhausted it on lower-value purchases in earlier markets is locked out of that advantage unless they take specific action.

If you’re a veteran and you’re not sure where you stand with your VA entitlement, how much you’ve used, whether you’re eligible for one-time restoration, or how to sequence future purchases to get the most out of the benefit, that conversation is worth having before you need it. The time to plan is before you’re in the middle of a transaction, not after. Reach out and we can walk through exactly where you stand.

Glenn Groves

Mortgage Broker | GTG Financial | Santa Rosa, CA

NMLS #1124642 | gtgfi.com

GTG Financial, Inc. NMLS #1595076 | CA DRE #02029711. Equal Housing Opportunity. Not a commitment to lend. Subject to credit approval and underwriting. Rates and terms subject to change without notice. Individual rates vary based on credit profile, property type, occupancy, loan amount, and other factors. nmls consumeraccess.org

Related Posts