Introduction As the end of July approaches, many families are preparing for the back-to-school season.…

How Much Cash Do You Actually Need to Buy in Sonoma County?

May 2026 | GTG Financial | Santa Rosa, CA

TL;DR: What’s in This Post

- Why $50,000 is the number most first-time buyers in Sonoma County should be targeting

- What actually makes up that figure beyond the down payment

- The impound account — what it is and why it shows up at closing

- How seller credits and family gifts can help you close with less

- What VA buyers need to know about coming in at zero

Most first-time buyers in Sonoma County make the same mistake before they ever talk to a lender. They pull up a mortgage calculator, see a 3% down payment on an $850,000 home, and start mentally budgeting around $25,000. Then they sit down at the closing table and realize the number they needed was closer to twice that.

Here is the full picture before that happens to you.

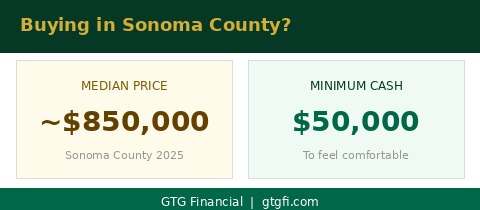

The Number: $50,000

The minimum amount of cash you want to have to feel comfortable as a first-time buyer in Sonoma County — comfortable meaning you can look at multiple loan options and not be squeezed — is about $50,000. That is not a conservative number invented to scare you. It is a practical floor based on what a typical transaction actually costs here.

With a median home price around $850,000, a 3% down payment gets you in at roughly $25,500. That number is accurate. The problem is that it only covers one piece of the transaction, and there are several others waiting behind it.

What Is Actually in That $50,000

Once the down payment is accounted for, you are still looking at $12,000 to $15,000 in closing costs and prepaids. This is the piece that catches most buyers off guard. It covers escrow fees, title fees, the appraisal, credit reports, and all the other third-party costs that go into a transaction. None of it is optional and very little of it is negotiable.

On top of that, if you are putting less than 10% down, your lender will require something called an impound account. That adds another layer of cash you need at closing, which we will get into in a moment.

Add it all up and $50,000 is the number that gets you to the closing table without feeling like you are scraping the bottom of your account.

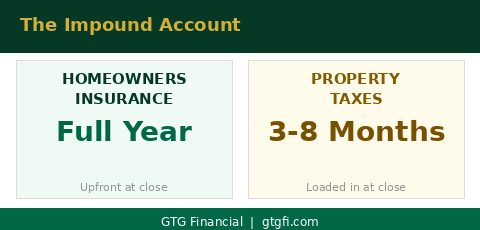

The Impound Account

An impound account — also called an escrow account — is a forced savings account your lender sets up to collect property taxes and homeowners insurance alongside your monthly mortgage payment. Instead of paying those bills yourself twice a year and once a year respectively, your lender collects a portion each month and pays them on your behalf when they come due.

The catch is that you have to fund the account upfront at closing. That means a full year of homeowners insurance comes out of pocket on day one. Property taxes are more variable: depending on where you are in the tax calendar, you will typically need to bring in anywhere from 3 to 8 months of taxes. On an $850,000 home in Sonoma County, that is a real number that needs to be in your account before you can close.

This requirement kicks in when you put less than 10% down. Most first-time buyers in this price range are in that category, so it applies to the majority of people reading this.

Closing Costs: What Makes Up the $12,000-$15,000

The closing costs bucket is made up of several different line items. Escrow and title fees are typically the largest chunk, running somewhere in the range of $4,000 to $6,000 depending on the purchase price and the companies involved. Appraisal and third-party reports — credit reports, flood certifications, and similar items — generally add $600 to $2,000. The rest is a mix of prepaids and miscellaneous lender fees that fill in the remaining gap to get you to that $12,000 to $15,000 total.

The good news is that some of this is negotiable, just not with your lender. Seller concessions are one of the most common ways buyers in Sonoma County offset closing costs. If the seller agrees to credit you a portion of the purchase price back at closing, that money can be applied directly against these costs. Family gifts are another route — we see them regularly on first-time buyer transactions and they are fully allowed on most loan programs as long as they are documented properly.

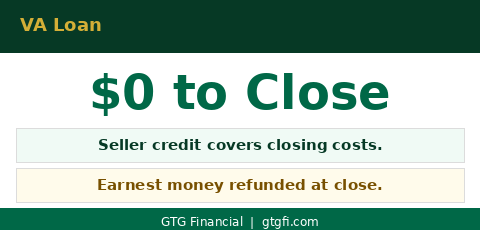

The VA Exception

If you have VA eligibility, the math changes significantly. We have closed deals where the borrower came in with nothing out of pocket. The seller provided a credit of $12,000 to $15,000 that covered all the closing costs, and the buyer put in a $5,000 earnest money deposit that was refunded to them at the close of escrow. The net cost to the borrower was zero.

That is not a guarantee — it depends on the seller agreeing to the credit and the deal penciling out — but it happens, and it happens regularly on VA transactions in this market. If you have a VA benefit and have not explored what that actually means for your cash position, that conversation is worth having before you assume you need $50,000 in the bank.

What to Take Away

The $50,000 figure is a practical floor, not a magic number. Some buyers will need more depending on the price point, the time of year, and where their taxes land. Some will need less if they negotiate seller concessions or have family help. The number can move. What matters is understanding what it is made of before you start the search, not after you fall in love with a house.

The buyers who get into trouble are the ones who find out about closing costs and impound accounts for the first time when they are already in escrow. By that point there is not a lot of room to maneuver. The better position is to know the full picture going in so you can set realistic targets and make smart decisions about what to offer and how to structure the deal.

$50,000 is a safe number to have in the bank. Know what it covers before you need it.

If you are buying in Sonoma County and want to understand exactly where you stand on cash before you start shopping, reach out. That conversation is free and there is no obligation.

Glenn Groves

Mortgage Broker | GTG Financial | Santa Rosa, CA

NMLS #1124642 | gtgfi.com

GTG Financial, Inc. NMLS #1595076 | CA DRE #02029711. Equal Housing Opportunity. Not a commitment to lend. Subject to credit approval and underwriting. Dollar figures referenced are estimates based on typical Sonoma County transaction costs as of Q1 2026 and subject to change. Individual results vary based on purchase price, loan program, property tax timing, and other factors. nmls consumeraccess.org

Related Posts