Introduction As the end of July approaches, many families are preparing for the back-to-school season.…

What Bay Area Buyers Get Wrong in Sonoma County

May 2026 | GTG Financial | Santa Rosa, CA

TL;DR: What’s in This Post

- Why Bay Area buyers almost always zero in on the Russian River area

- What makes river area properties different from a lending standpoint

- The unpermitted additions and unusual conversions that create complications

- Why working with a local lender makes the whole transaction easier

When buyers come up from the Bay Area, there is almost always a pull toward the river. The Russian River towns (Guerneville, Monte Rio, Forestville) represent exactly what they are looking for: a retreat from city life, something quieter, something different. That instinct makes complete sense.

What most of them do not realize until they are already in the process is that those properties come with a set of lending complications that most out-of-area lenders have never seen before.

The Dream: River Life in Sonoma County

The appeal of the Russian River area is real. These are genuine small towns with character, surrounded by redwoods, right on the water. For someone coming from San Francisco or Oakland, the idea of trading city life for a house on the river is a compelling one. And for the right buyer in the right situation, it absolutely makes sense.

The issue is not the properties themselves. It is the gap between what buyers expect the process to look like and what it actually looks like when you start working with a lender on some of these homes.

What They Don’t Expect

River area properties are unique. There is a lot of stuff that gets done to these homes over the years: an unpermitted sunroom here, a basement that got converted into something else, a church that was turned into a house. Just oddball stuff that buyers are not expecting to see and, more importantly, do not understand can create real lending restrictions.

It is not that lenders are hyper conservative about it. It is just genuinely unusual, and lenders are not always comfortable lending on properties with unpermitted additions or non-standard conversions. That discomfort can slow a deal, complicate an approval, or in some cases stop it altogether, especially if the lender has no local experience and is seeing the property type for the first time.

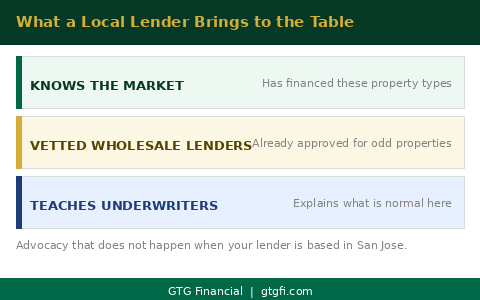

Why Local Knowledge Changes Everything

A local lender who knows Sonoma County knows these property types. We have wholesale lenders we work with who have seen the same condominium complexes and non-standard properties before. We have taken the time to vet them. And when something looks unusual to an out-of-area underwriter, we can go to bat and explain it. Because we know what is normal here and what is not.

Sometimes that means literally teaching an underwriting team why a property is priced the way it is. This is totally normal for this area. That kind of advocacy does not happen when your lender is based in San Jose and has never financed a property on the Russian River.

The result is a transaction that runs smoother for everyone involved: the buyer, the seller, and the realtors. A well-prepared local lender does not create surprises at the end of escrow.

What to Take Away

If you are coming from the Bay Area and looking at properties in the Guerneville, Monte Rio, or Forestville area, the first call you make should be to a lender who knows that market. Not a bank you already have a relationship with. Not an online lender. Someone local who has closed deals on these properties and knows exactly what to expect.

The property itself might be completely fine. The lending on it is a different story, and that story requires someone who already knows the ending.

Working with somebody who understands the intricacies of Sonoma County makes it way easier on the buyer, the seller, and the realtors. Everybody involved.

If you are buying in Sonoma County and want to talk through what your specific situation looks like, reach out. That conversation is free and there is no obligation.

Glenn Groves

Mortgage Broker | GTG Financial | Santa Rosa, CA

NMLS #1124642 | gtgfi.com

GTG Financial, Inc. NMLS #1595076 | CA DRE #02029711. Equal Housing Opportunity. Not a commitment to lend. Subject to credit approval and underwriting. Individual results vary based on credit profile, loan amount, property type, and other factors. nmls consumeraccess.org

Related Posts