VA Bonus Entitlement and the Departing Residence Rule

Deal Deep Dive | May 2026 | GTG Financial | Santa Rosa, CA

TL;DR: What’s in This Post

- What bonus entitlement is and how it works across two properties

- How the VA departing residence rule works – and why it’s one of the best guidelines in the handbook

- Why conventional financing would not have worked for this borrower

- How a 100% disabled veteran in Texas ended up with a $2,193 monthly payment

- Why forward planning around VA entitlement matters before you need it

Not every deal is straightforward. Some of the most interesting ones come together through a combination of guidelines that most lenders either don’t know about or don’t take the time to work through. This one had two of them running at the same time, and getting it across the finish line required understanding how VA entitlement actually works at a deeper level than most borrowers, or lenders, ever get into.

Here is the full breakdown.

The Deal at a Glance

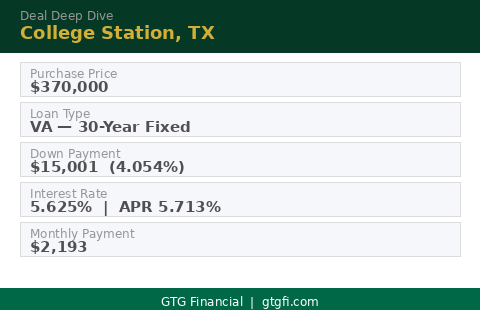

This was a $370,000 purchase in College Station, Texas on a VA loan. The borrower put down $15,001, which works out to 4.054%. That is an unusual number, and the reason for it gets into something most veterans have never heard of: bonus entitlement.

The interest rate came in at 5.625% with an APR of 5.713% on a 30-year fixed. The total monthly payment landed at $2,193. That number is lower than you might expect for a $370,000 purchase, and there are a few reasons for that which I will get into below.

The Down Payment: How Bonus Entitlement Works

This borrower already owned a home in San Diego. He purchased it in 2021 using his VA loan benefit, which means a chunk of his entitlement was already committed to that property. He was relocating to College Station and needed to buy a new primary residence, and the plan was to use his VA loan again on the new purchase.

This is what is called a bonus entitlement deal. The VA loan is not a one-and-done benefit. You can use whatever entitlement remains after the first purchase to buy again, even while still holding the first home. The amount of entitlement you have left relative to the new purchase price determines whether you need a down payment, and if so, how much.

In this case, the remaining entitlement covered most of the purchase but left a gap that required $15,001 down. That is where the unusual percentage comes from. It is not an arbitrary number. It is exactly what the math required to use the remainder of his entitlement on the new property.

The Rate: Why VA Was the Right Call

We got him a 5.625% interest rate with an APR of 5.713%. At the time, that was notably lower than what he would have seen on a conventional loan. On conventional financing, he would have had to put at least 5% down, paid mortgage insurance on top of that, and taken a higher rate. None of that made sense when VA was available and he had entitlement left to use.

He also did not plan to use his VA loan again in the near term, which made deploying the remaining entitlement here an easy call. You use the tool when the tool is available and the math supports it. This was one of those situations.

The Monthly Payment Breakdown

The $2,193 monthly payment is made up of just two things: principal and interest at $2,043, and homeowner’s insurance at $150. There is no mortgage insurance, because VA loans do not require it. And there are no property taxes in this payment, because this borrower is a 100% disabled veteran in the state of Texas, which provides a full property tax exemption for qualifying veterans.

That tax exemption is a Texas-specific benefit and not something that applies everywhere, but it is worth understanding if you or someone you know is a disabled veteran considering a move to a state that offers similar programs. It makes a significant difference in the monthly number.

The Main Challenge: The Departing Residence

Here is where this deal got interesting. He still owned the San Diego home and had a mortgage payment on it. When a borrower is leaving one home to buy another, the existing property becomes what the VA calls a departing residence. How that mortgage payment gets handled in the qualification calculation makes a big difference in whether a borrower can qualify for the new purchase.

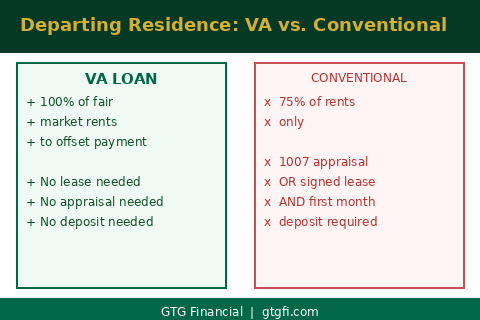

The VA handbook has one of the best guidelines I have seen on this. If you are moving from one property to another and using a VA loan on the new purchase, you can use 100% of fair market rents to offset the payment on the departing residence. Not as income. As an offset. So if his San Diego payment is $2,500 a month and he can reasonably rent that property for $3,500, you do not get to give him $1,000 of extra income. What you can do is wipe out the $2,500 payment entirely from his debt-to-income calculation.

That is a significant distinction, and it is one of the reasons VA financing made this deal work when conventional would not have.

Why Conventional Would Not Have Worked

On a conventional loan, the departing residence rules are much more stringent. You can only use 75% of rents received, not 100%. And to use any rental income at all, you typically need either a 1007 appraisal done on the departing property, which is a single family comparable rent schedule, or a fully executed lease agreement with a first month’s deposit collected.

Here is the problem with that. This borrower is living in the San Diego home right now. He is buying in Texas and will be moving in the next few weeks. How are you supposed to produce a signed lease with a deposit when the house is still your primary residence? You are not. And lenders know the trick of getting a family member to sign a lease. That does not fly either.

The VA guideline solves this cleanly. Fair market rents, verified through the appraisal process, are sufficient to offset the departing residence payment. No lease required. No deposit required. No impossible timeline to work around.

How It All Came Together

Between the bonus entitlement structure, the VA rate advantage, the absence of mortgage insurance, and the departing residence offset, this deal came together in a way that simply was not possible on conventional financing. The borrower got into a new home, kept the San Diego property, and ended up with a $2,193 monthly payment on a $370,000 purchase.

This is the kind of deal that does not happen without understanding the VA handbook at a deeper level. If you are a veteran with an existing home and you are thinking about buying again, the conversation about entitlement and departing residence guidelines is worth having before you are in the middle of a transaction. The planning part matters.

It really takes future planning to understand how to leverage your entitlement to the highest and best use.

If you are a veteran in Sonoma County or the North Bay thinking about your next move, or you have questions about how your current entitlement could work for you, reach out. That is exactly what we do.

Glenn Groves

Mortgage Broker | GTG Financial | Santa Rosa, CA

NMLS #1124642 | gtgfi.com

GTG Financial, Inc. NMLS #1595076 | CA DRE #02029711. Equal Housing Opportunity. Not a commitment to lend. Subject to credit approval and underwriting. Rates and terms subject to change without notice. Individual rates vary based on credit profile, property type, occupancy, loan amount, and other factors. nmls consumeraccess.org

Related Posts