Introduction As the end of July approaches, many families are preparing for the back-to-school season.…

VA Appraisal and Tidewater

June 2026 | GTG Financial | Santa Rosa, CA

TL;DR: What’s in This Post

- Why a low appraisal on a conventional loan is a dogfight and a VA appraisal is not

- What Tidewater is and exactly how the 48-hour process works

- How VA buyers can escalate directly to the Regional Loan Center

- What your options actually are if you are stuck with a low appraisal on a conventional loan

When an appraisal comes in below the purchase price, what happens next depends almost entirely on what type of loan you are using. For conventional and FHA buyers, it is an uphill battle. For VA buyers, the process is completely different. Most people do not know this going in.

There are really two distinct tiers when it comes to low appraisals. There is VA, and then there is everybody else.

Everybody Else: Be Prepared for a Dogfight

For conventional and FHA buyers, fighting a low appraisal is possible but far from guaranteed. If the appraiser missed comps or left out relevant data, a strong agent and a strong lender can go back to the appraisal management company and request a reconsideration of value. But just understand that the appraiser did the legwork. Their report is semi set in stone.

If you are going in just to take a swing and see if you can recover on a large appraisal gap, be prepared for a dogfight. You need a strong lender, a strong agent, good communication between both, and an extra week of time that was not originally being accounted for.

VA Tidewater: A Completely Different Process

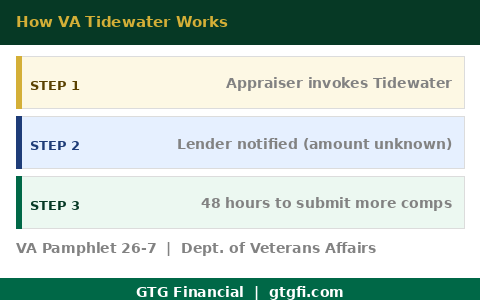

VA is very unique with low appraisals because of a process called Tidewater. They actually make it pretty easy.

Here is how it works. If a VA appraiser determines that the value is going to come in below the purchase price, they are required to contact the lender before submitting the final report. They invoke Tidewater. They cannot tell you how much lower the value will be, whether it is $5,000 or $100,000 below the purchase price. But they give you a heads up and say you have 48 hours to provide additional comparable sales.

They want to help. The message is essentially: I just do not have what I need to give you this value. Give me more comps and I will take another look. This is the opposite of how it works with conventional appraisals, where the report comes back through the appraisal management company and the appraiser is largely unreachable after the fact.

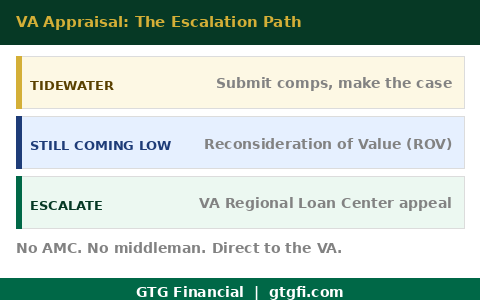

If Tidewater Still Comes In Low

If the value still comes in low after Tidewater, VA buyers have one more option that conventional buyers do not. You can go over the appraiser’s head. You submit an appeal directly to the VA Regional Loan Center with a formal reconsideration of value request. You are not going around the appraiser in a way that is going to offend anyone. It is a recognized part of the VA process.

It is not a guaranteed outcome, but it is a legitimate path that we have been successful on multiple times. The fact that VA has no appraisal management company in the middle makes all of this possible. The appraisal order goes directly to the VA, we see who is assigned immediately, and there is direct communication throughout the process rather than waiting on an AMC to relay information back and forth.

What to Do if You Are Stuck on a Conventional Low Appraisal

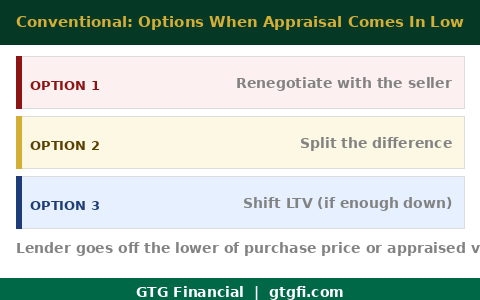

If you are a conventional buyer and the reconsideration of value does not move the needle, you still have options. The most common is renegotiating with the seller. Depending on the market and how the original offer was structured, the seller may be willing to come down to the appraised value.

You can also split the difference, where the seller drops the price partway and the buyer covers the remaining gap. And if the buyer is already putting a significant amount down, it is often possible to simply shift the loan to value percentage. The lender uses the lower of the purchase price or the appraised value, but if the buyer was putting 30 percent down on a million dollar purchase and the appraisal came in at $900,000, they may be able to bring the same $300,000 to the table without any extra cash out of pocket. The LTV just shifts.

VA is very unique with low appraisals because they have what is called Tidewater. They actually make it pretty easy.

If you are a veteran and want to understand how your VA appraisal rights work before you are in the middle of a deal, reach out. That conversation is free and there is no obligation.

Glenn Groves

Mortgage Broker | GTG Financial | Santa Rosa, CA

NMLS #1124642 | gtgfi.com

GTG Financial, Inc. NMLS #1595076 | CA DRE #02029711. Equal Housing Opportunity. Not a commitment to lend. Subject to credit approval and underwriting. Individual results vary based on credit profile, loan amount, property type, and other factors. nmls consumeraccess.org

Related Posts