Introduction As June unfolds and summer is in full swing, many families are considering making…

Divorce Refinance — How to Remove a Spouse from the Mortgage

June 2026 | GTG Financial | Santa Rosa, CA

TL;DR: What’s in This Post

- Why a quit claim deed does not remove a spouse from the mortgage

- Two paths: waiting for the decree vs. refinancing mid-divorce

- How a court-ordered cash out gets rate and term pricing

- The math on a real deal: $600K property, $450K refi, $150K payout

- Why you cannot keep your original interest rate in a divorce

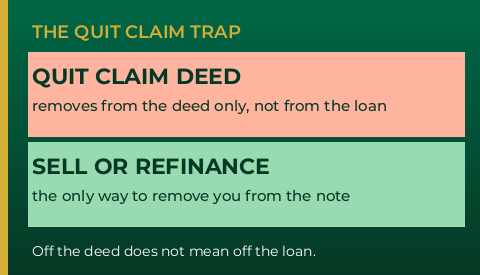

One of the most common misconceptions in a divorce involving a shared home is that signing a quit claim deed takes care of everything. It does not. The deed and the mortgage are two separate documents, and what happens to one does not automatically affect the other. Understanding the difference before any paperwork is signed can save both parties a significant amount of time, money, and legal exposure.

The Quit Claim Misconception

A quit claim deed transfers ownership of the property from one party to another. When a departing spouse signs a quit claim deed, they are giving up their ownership interest in the home. That is all it does.

The promissory note is a separate document. If both parties signed the original mortgage, both parties remain legally obligated on that loan regardless of what happens on the deed. A quit claim deed does not change that. The lender still holds both signatures, and both people are still liable for the debt.

The practical consequence of this is significant: you can quit claim off the deed, give up your ownership in the property, and still find yourself on the hook for the mortgage if the remaining party ever stops making payments. That exposure does not go away until the loan itself is either paid off, sold, or refinanced.

To actually remove a party from the mortgage, the property must be sold or refinanced. There is no other path.

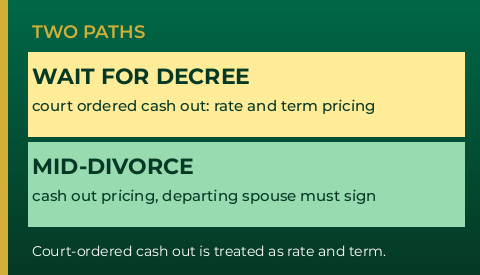

Two Paths: Waiting for the Decree vs. Mid-Divorce

When one spouse wants to keep the property and buy out the other, there are two timing scenarios, and the distinction between them has a direct impact on pricing.

Path A: Wait for the divorce decree. If both parties can wait until the divorce is fully finalized with the county and the marital settlement agreement is in place, the refinance is classified differently by lenders. When the decree specifically states that one party is keeping the property and provides a defined window to remove the other from the loan and deed, that transaction is treated as a court-ordered cash out. Lenders do not apply the additional pricing layer that normally comes with a cash out refinance. It is treated like a rate and term refinance, which means meaningfully better interest rates.

Path B: Refinance mid-divorce. In many cases, waiting for the decree is not practical. Divorce proceedings in some counties can take six months or longer, and both parties may want to resolve the property question before that. A mid-divorce refinance is absolutely doable, but it carries standard cash out pricing. The departing spouse must also remain involved in the process. Because the parties are still legally married at the time of closing, the departing spouse needs to sign a quit claim deed and a closing disclosure acknowledging that their legal spouse is refinancing without them. This requires a degree of cooperation between both parties through the transaction.

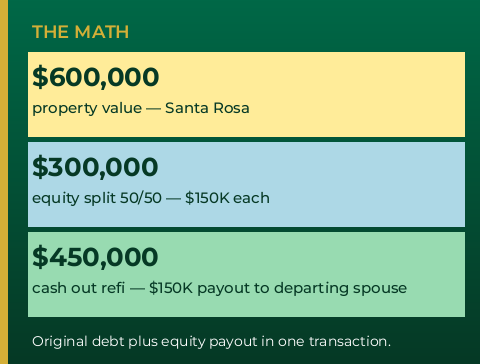

The Math: How a Divorce Buyout Works

Here is an example based on a real deal. A couple in Santa Rosa owned a $600,000 property. They owed $300,000 on the existing mortgage, leaving $300,000 in equity. The equity was being split equally, meaning each party was entitled to $150,000.

The staying spouse needed to do a cash out refinance for $450,000. That number covers the original $300,000 loan balance plus the $150,000 equity payout to the departing spouse. The departing spouse walks away with their share in cash. The staying spouse takes over the property with a new loan at their name alone.

The structure is straightforward once the equity position is clear, but it requires knowing the current value of the property, the outstanding loan balance, and how the equity is being divided. Those numbers drive everything.

What About Alimony and Child Support?

In some divorces, the equity in the home can be used to simplify ongoing financial obligations. If there is an alimony or child support arrangement in play and the equity is sufficient, it is sometimes possible to structure the equity split so that the monthly obligation is paid out as a lump sum instead of a recurring payment.

As an example: if one party owes $4,000 per month in support for a defined number of years, the total obligation over that period could potentially be calculated and baked into the equity payout at closing rather than structured as monthly payments. The departing spouse receives a larger lump sum at closing, and the recurring payment obligation is eliminated.

This kind of structuring requires close coordination with the divorce attorney. All parties need to be on the same page about what is happening and agree that the arrangement is fair. It is not the right fit for every situation, but for cases where there is meaningful equity and a defined support obligation, it is worth having the conversation before the divorce is finalized.

The Rate Reality

The piece that surprises most people going through this process is what happens to their interest rate. If both parties are on the note and one needs to be removed, there is no way to keep the original rate. A refinance is required, and that means a new loan at current market rates.

“You can’t keep your original interest rate. If both parties are on the note and the deed, you’re going to have to refinance to remove them from at least the note.”

Glenn Groves | GTG Financial

It is worth noting that you can remove a party from the deed without refinancing through a quit claim — but as discussed above, that does not remove them from the loan. The note requires a refinance. The sooner both parties understand that, the better positioned they are to plan around current rate conditions and structure the deal in the way that makes the most sense for everyone involved.

These situations are more common than most people expect, and there is usually a path forward. The key is getting the full picture early, before decisions are made that are difficult or impossible to reverse.

Glenn Groves | NMLS #1124642 | GTG Financial, Inc. NMLS #1595076 | CA DRE #02029711 | Equal Housing Opportunity | Not a commitment to lend. Loan terms, pricing, and refinance eligibility vary by borrower, lender, and situation. This post is for informational purposes only and does not constitute legal or financial advice. Consult a licensed mortgage professional and a qualified attorney regarding your specific situation. nmls consumeraccess.org

Related Posts