June 2026 | GTG Financial | Santa Rosa, CA TL;DR: What's in This Post Why…

FICO vs. Vantage Credit Score — What Mortgage Buyers Need to Know

June 2026 | GTG Financial | Santa Rosa, CA

TL;DR: What’s in This Post

- What FICO and Vantage are and how they differ as credit scoring models

- Why Vantage often scores higher on the same borrower

- How large the gap between the two models can be in practice

- How GTG Financial uses both sets of scores to guide borrowers

- What to do if you were previously told your credit score was not high enough

There are now two credit scoring models that matter for your mortgage. For most of the history of the mortgage industry, FICO was the only name in the room. That has changed. Understanding both models and how they interact with your approval could be the difference between a denial and a path forward.

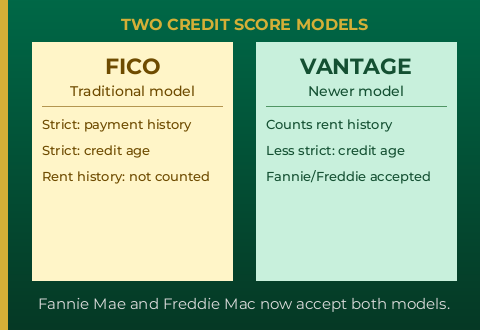

The Two Credit Scoring Models

FICO has been the industry standard for mortgage lending for decades. It is a well-established model that most lenders have used as the default when pulling credit for a loan application. Vantage is a newer scoring model, developed by the three major credit bureaus as an alternative approach to measuring creditworthiness.

The significant development in recent years is that Fannie Mae and Freddie Mac have issued guidance indicating they will accept loans underwritten using the Vantage credit scoring model. That decision opened the door for lenders to begin pulling and using Vantage scores alongside FICO scores, which is now changing how some mortgage professionals approach the credit evaluation process.

Why Vantage Usually Scores Higher

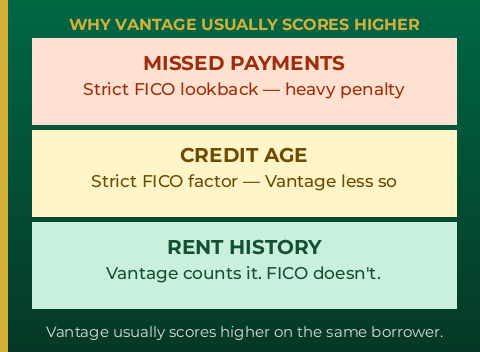

The two models do not weigh the same factors the same way. FICO is considerably more strict when it comes to missed payments. If you missed a payment within the last couple of years, FICO penalizes that heavily. FICO also places significant weight on the length of your credit history. A shorter credit history, even with a clean payment record, can pull your FICO score down.

Vantage takes a different approach. It takes into account rent history, which FICO does not factor in at all. For borrowers who have been reliably paying rent for years but have a thinner or younger credit file, that distinction can be significant. Vantage also places less emphasis on the length of time you have had credit, which means borrowers who are newer to traditional credit lines are not penalized as sharply.

The result is that on the same borrower with the same underlying financial history, Vantage will often produce a meaningfully higher score than FICO. Not always, but often enough that it is worth knowing about.

The Score Gap in Practice

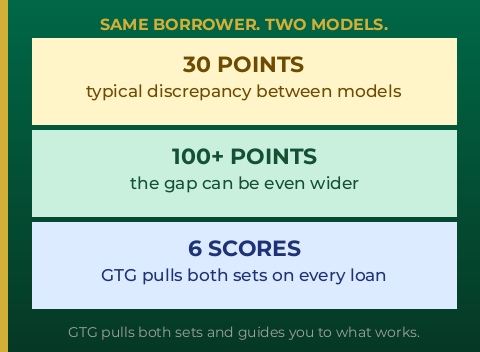

The size of the gap between a borrower’s FICO and Vantage scores varies. Sometimes the discrepancy is around 30 points. In other cases, the gap can be 100 points or more on the same borrower. The difference depends on the specifics of the borrower’s credit profile, including how the major credit bureaus are reporting their history and how each model weighs those factors.

A higher Vantage score does not automatically mean a better outcome. The real-world impact depends on which lenders are currently accepting Vantage scores, what products those lenders offer, and what interest rates they are pricing. More lenders are expected to adopt Vantage over time, but the landscape is still evolving.

How GTG Financial Approaches Credit Scoring

At GTG Financial, the approach is to pull both sets of scores on every loan. That means six scores per borrower: three FICO scores and three Vantage scores. The goal is to have the full picture from the start, so that the borrower can be guided in the direction that actually works best for them given the current lender landscape.

Running both models is not standard practice across the industry. Many lenders still rely exclusively on FICO scores, which means a borrower who might benefit significantly from Vantage could be evaluated on an incomplete picture of their creditworthiness. Having access to both sets of scores gives the conversation a much broader foundation.

If Your Credit Score Has Held You Back Before

If you were told previously that your credit score was not high enough to qualify, or that your score was negatively affecting the interest rate you were being offered, it may be a good time to revisit that conversation. The introduction of Vantage as an accepted model is a genuine change in how credit can be evaluated for mortgage purposes, and for some borrowers it represents a meaningful shift in what is possible.

“If people were told previously that their credit score wasn’t high enough or it was just detrimental to the type of pricing, the interest rate that they were receiving, it may be a good time to revisit that conversation and look at what the Vantage scoring model can offer them.”

Glenn Groves | GTG Financial

Credit scoring is not static, and the tools available to evaluate it are evolving. If your situation has changed, or if it has been a while since you last had a full credit review with a mortgage professional, it is worth having that conversation again with the current options in front of you.

Glenn Groves | NMLS #1124642 | GTG Financial, Inc. NMLS #1595076 | CA DRE #02029711 | Equal Housing Opportunity | Not a commitment to lend. Credit score information is for educational purposes only. Score results vary by model, lender, and individual credit profile. Not all lenders accept Vantage credit scores. Consult a licensed mortgage professional regarding your specific situation. nmls consumeraccess.org

Related Posts