Introduction With the Independence Day holiday just around the corner, many homeowners are considering home…

Deal Deep Dive — Delayed Financing

June 2026 | GTG Financial | Santa Rosa, CA

TL;DR: What’s in This Post

- How a client bought a $1,350,000 Santa Rosa home all cash using a 60-day IRA margin loan

- What delayed financing is and how the refi works the day after close

- Why a conforming loan at $832,750 gave him the best of both worlds

- What you have to have in place before you try this

Cash buyers close faster, negotiate harder, and win more deals. Most people assume that means you need cash sitting somewhere outside of a retirement account. This deal shows a different way to get there.

The Deal

The property was in Santa Rosa at a $1,350,000 purchase price. The borrower had enough cash in an IRA and was old enough to access it. Rather than put 20 to 25% down and finance the rest through a traditional loan, he took a 60-day margin loan against the IRA to become a cash buyer outright.

No financing contingency. More leverage at the table. The ability to close in ten days and waive conditions that a financed buyer cannot. Cash talks, and in a competitive situation, that matters.

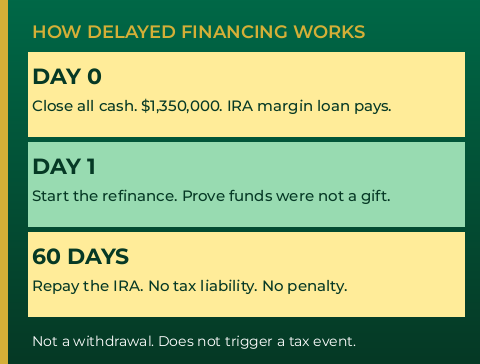

How Delayed Financing Works

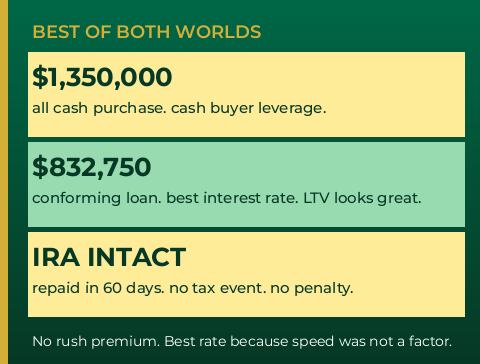

He closed on the property for $1,350,000. The day after close of escrow, the refinance process started. This is delayed financing: you purchase all cash, then immediately refinance to pull your money back out.

The key requirement with the lender is proving that the funds used to purchase the property were not a gift. They were his funds, and that documentation needs to be clean. Once that is established, he had a 60-day window to repay the margin loan to his IRA without incurring any tax liability or penalty.

That window is the whole game. The margin loan against the IRA is not a withdrawal. It does not trigger a tax event. It just temporarily moves money out of the IRA, gets the deal done, and comes back in through the refinance proceeds before the 60-day clock runs out.

The Numbers

The refinance came in as a conforming loan at $832,750. His LTV looked great. And because we did not need to take speed into account anymore, we could go after the cheapest lender we could find, knowing we had 45 to 60 days to get it done. No rush premium. Best rate available for a conforming loan.

That is the part people miss when they think about cash offers. It is not just about winning the deal. It is about being able to optimize the financing on your own terms afterward, without a clock running on a rate lock or a seller’s patience.

“Cash talks. Let’s close in ten days, waive contingencies. He didn’t have to wait on the financing piece. We got to do it on our own terms.”

Glenn Groves | GTG Financial

What You Have to Have in Place First

This strategy only works if you have already done the work upfront. You do not want to go into this headlong thinking you can borrow against your assets, purchase a property, and figure out the refinance later. You still have to qualify for that new loan.

In this case, the borrower was income-qualified as a financed buyer before he ever went in as a cash buyer. The property was also reviewed ahead of time to confirm it would qualify for conventional financing after close. There was a short delay before the appraisal was ordered because a few items needed to be addressed on the property. That was factored in from the beginning.

The deal works because of the preparation, not in spite of it. If the refinance had not been viable, the entire structure falls apart. That conversation has to happen before you make the offer, not after.

If you have retirement assets and are looking at a competitive purchase, this is worth a conversation. The right setup makes a cash offer possible without permanently moving money out of a tax-advantaged account.

Glenn Groves

Mortgage Broker | GTG Financial | Santa Rosa, CA

NMLS #1124642 | gtgfi.com

GTG Financial, Inc. NMLS #1595076 | CA DRE #02029711. Equal Housing Opportunity. Not a commitment to lend. Subject to credit approval and underwriting. Individual results vary based on credit profile, loan amount, property type, and other factors. nmls consumeraccess.org

Related Posts