Understanding the Impact of Hurricane Season on Homeownership As we approach the peak of hurricane…

Debt to Income (DTI)

June 2026 | GTG Financial | Santa Rosa, CA

TL;DR: What’s in This Post

- Why a perfect credit score does not guarantee mortgage approval

- What debt to income ratio actually is and why the back end number is the one that matters

- Which types of consumer debt knock you out of qualification and by exactly how much

- How reallocating down payment funds can open up your DTI more than the extra equity would

A high credit score is not a green light. It tells the lender you pay your bills. It does not tell them you can afford this particular mortgage on top of everything else you already owe. The number that quietly kills more deals than most people expect is debt to income. And most buyers do not know how it works until it is already a problem.

What DTI Actually Is

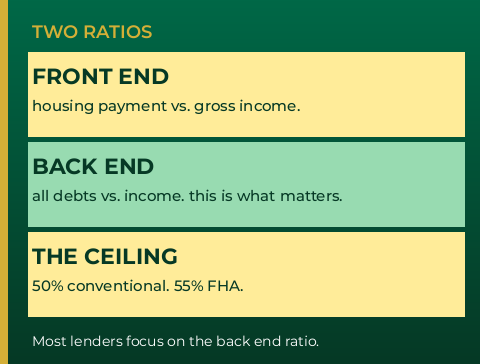

Debt to income in plain English is exactly what it sounds like. It is your debt versus your income. There are two ratios that go into a mortgage qualification: a front end and a back end.

The front end is just the housing payment compared to your gross monthly income. The back end is your gross income measured against the monthly payment plus every other consumer debt you carry. That is the number most lenders care about, and that is the one that tends to catch people off guard.

For conventional financing, the back end ceiling is 50 percent. FHA goes up to 55 percent. VA works differently, using residual income rather than a strict DTI percentage, which is why VA borrowers can sometimes qualify at ratios that would get rejected on a conventional loan.

What Breaks It

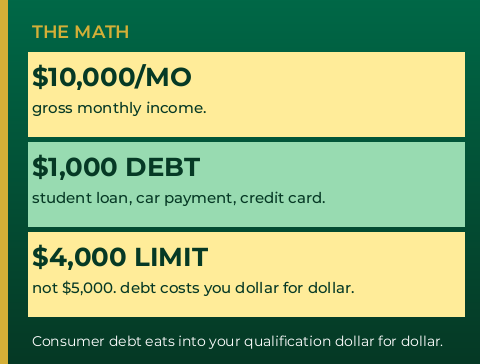

The math is straightforward once you see it. Say you make $10,000 a month gross. On paper, you should be able to carry about a $5,000 a month mortgage payment at a 50 percent back end ratio. That is true, assuming you have no other debts.

But if you have $1,000 a month in consumer debt, that number drops to $4,000. The mortgage payment you can qualify for shrinks dollar for dollar with every debt the lender has to count against you.

The debts that most commonly create problems are student loans, car payments, credit card minimums, and cosigned debt for other people. That last one is often a surprise. If your name is on a loan, even if someone else is making the payments, it counts against your DTI. The lender has no way to confirm you will not end up responsible for that payment at some point.

How to Fix It

Looking for a cheaper house is one option. But the move that actually solves the problem most of the time is satisfying existing debt before you close. Pay stuff off. Get the monthly obligations down. That is what moves the back end ratio.

The play that often surprises people is the down payment reallocation. If you are sitting on 20 percent down, reallocating 5 percent of that to eliminate a car loan or knock out a few credit cards can do more for your qualification than keeping that equity in the deal. You end up with a slightly higher LTV, but you actually qualify for the property you want. The math works out.

The conversation has to happen before you start shopping. Once you are in contract and the lender runs the numbers, your options narrow fast. Coming in early, with tax returns and a current list of debts, is how you find out whether the fix is simple or whether there is real work to do.

“This is not the whole Dave Ramsey you should spend 26% of your income thing. I’m sorry. It’s expensive to live here.”

Glenn Groves | GTG Financial

The Bigger Picture

DTI limits exist for a reason. A lender that approves a borrower at 55 percent back end is betting that person can handle their life on 45 cents of every dollar they earn. In a high cost of living market, that math gets uncomfortable fast. The goal is not to push the ratio as high as it will go. The goal is to understand where you sit before you start making offers.

If you are unsure where your DTI lands, bring your tax returns and a list of your monthly debt obligations to that first conversation. It takes ten minutes to get a clear picture, and it will save you from finding out the hard way somewhere in the middle of escrow.

Glenn Groves

Mortgage Broker | GTG Financial | Santa Rosa, CA

NMLS #1124642 | gtgfi.com

GTG Financial, Inc. NMLS #1595076 | CA DRE #02029711. Equal Housing Opportunity. Not a commitment to lend. Subject to credit approval and underwriting. Individual results vary based on credit profile, loan amount, property type, and other factors. nmls consumeraccess.org

Related Posts