Understanding the Summer Housing Market The summer months, stretching from the Fourth of July to…

The Rent Paradox – Why Paying Rent Doesn’t Mean You Qualify

June 2026 | GTG Financial | Santa Rosa, CA

TL;DR: What’s in This Post

- Why paying rent on time does not prove you qualify for a mortgage

- How a lender measures you differently than a landlord does

- What debt-to-income is, and why the back-end ratio is what matters

- How newer credit models like Vantage are starting to factor in rent

It is one of the most common frustrations we hear from renters. You have paid $4,000 or $5,000 a month, on time, for years, and a lender still tells you that you may not qualify for a mortgage payment lower than your current rent. It feels backwards. The reason comes down to how a lender measures you, and it is a very different test than the one your landlord ran.

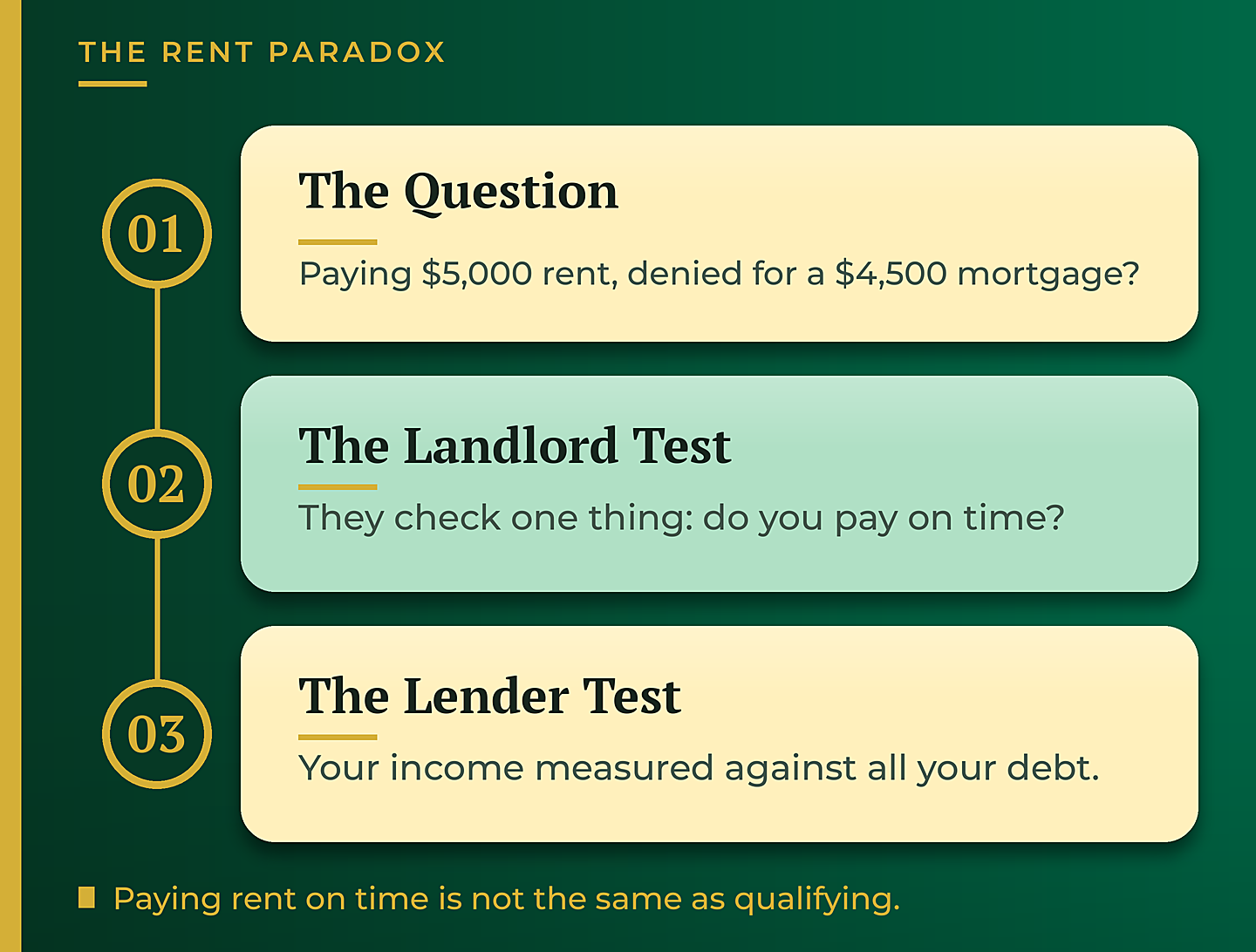

A Landlord and a Lender Ask Different Questions

When a landlord decides whether to rent to you, they are mostly asking one thing: do you pay on time? Sometimes they glance at your credit score. That is roughly the whole test. A mortgage lender is doing something far more involved. They weigh your income against the proposed payment and every other debt you carry.

That is why someone paying $5,000 in rent can be told they do not qualify for a $4,500 mortgage. The rent proves you are responsible. It does not prove your income can absorb the new payment once the lender adds your car loan, student loans, credit cards, and anything you have cosigned. Borrowing several hundred thousand dollars is a different animal than renting.

How Debt-to-Income Actually Works

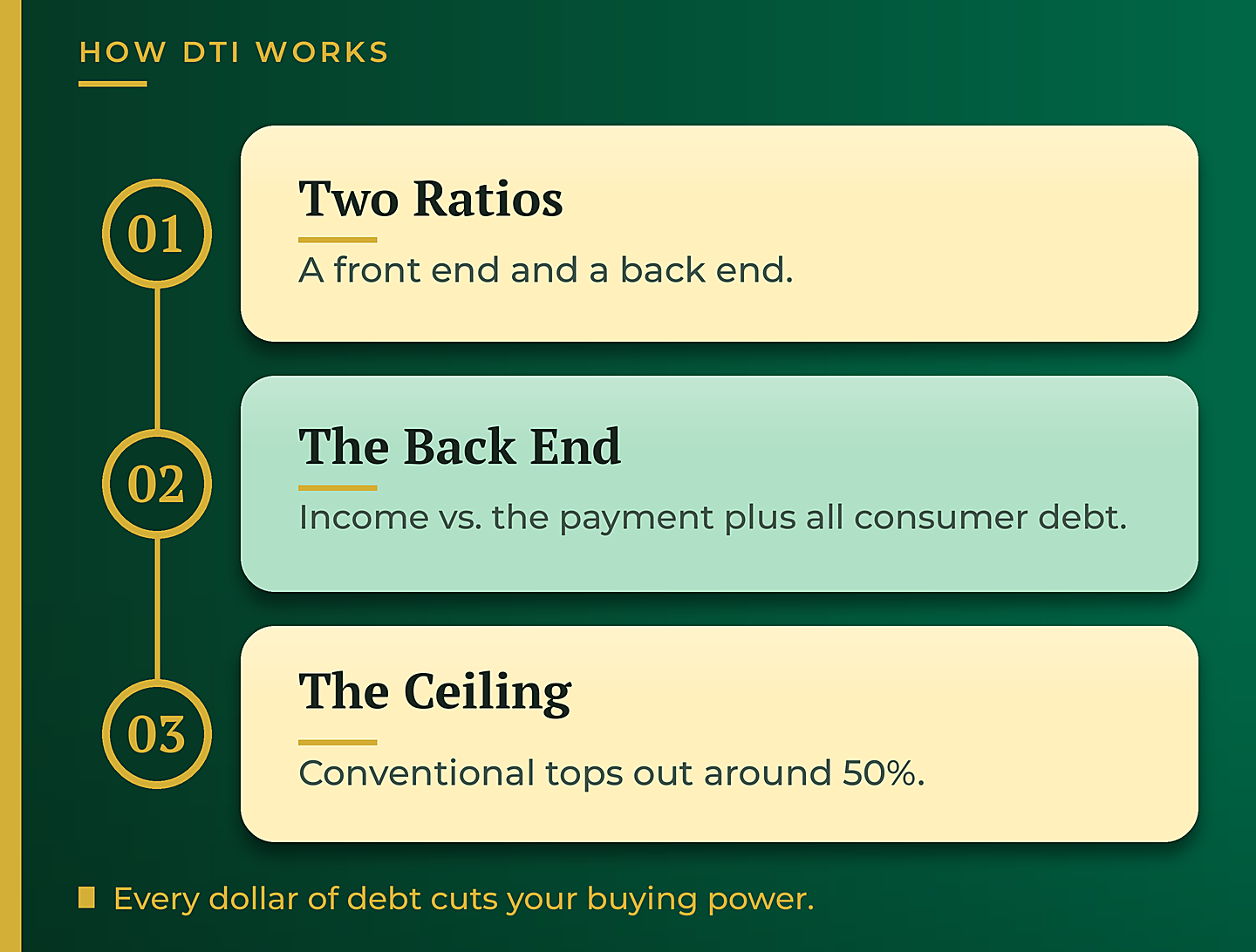

Debt-to-income, or DTI, is exactly what it sounds like: your debt measured against your income. There are two ratios. The front end looks at just the housing payment against your income. The back end, the one that usually matters, looks at the housing payment plus all of your other monthly consumer debt. That back-end number is what trips most people up.

The mechanics are simple. If you earn $10,000 a month, on paper you might carry around a $5,000 payment. But if you already have $1,000 a month in other debt, that number drops to roughly $4,000. Every dollar of monthly debt directly reduces your buying power. For most conventional loans the back-end ceiling lands near 50 percent, and other programs vary from there.

What Counts, and What Is Changing

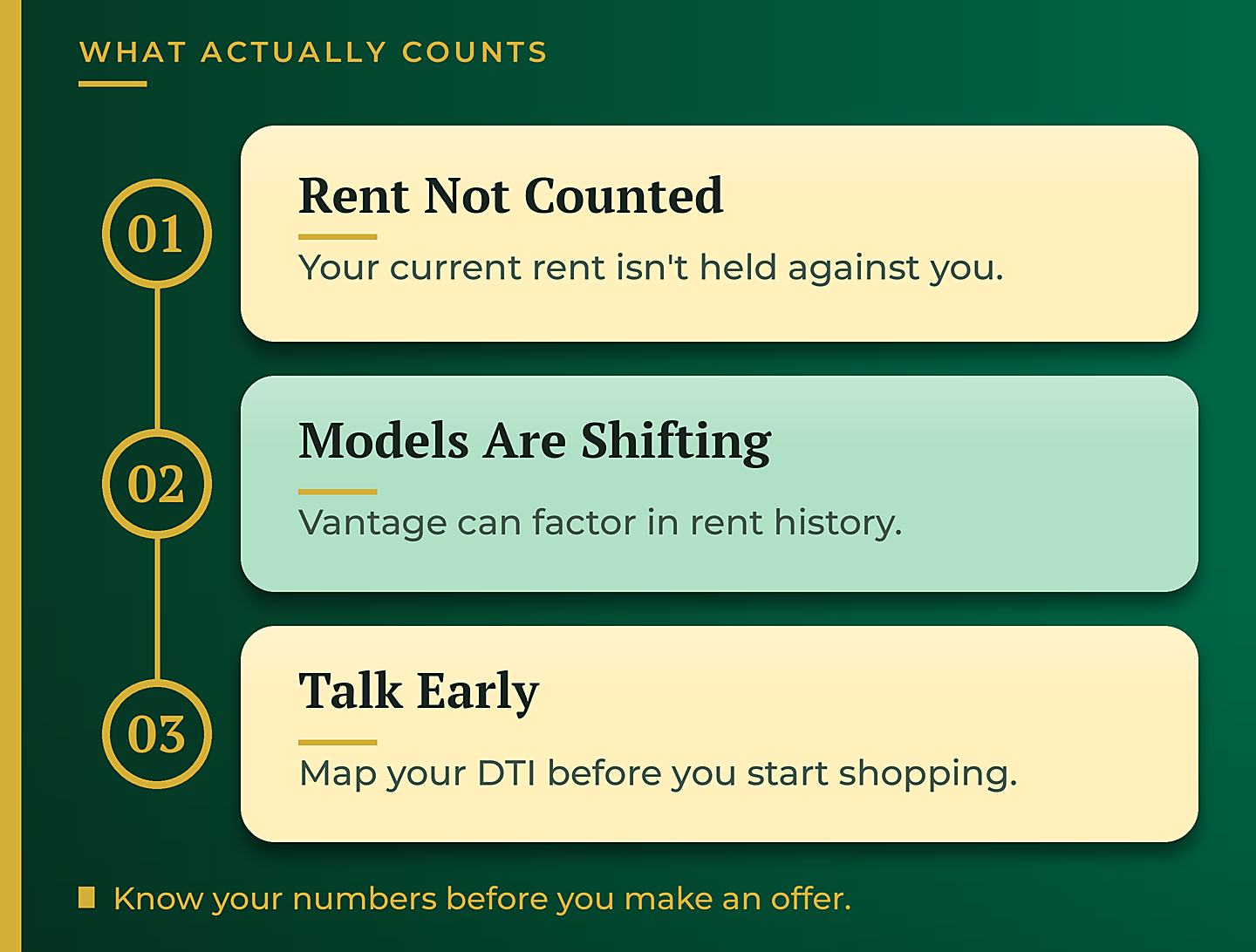

There is good news buried in here. The rent you pay right now is not held against you, because once you buy you will not be paying it anymore. Your current rent is not the obstacle. The other debt sitting alongside your income is.

The rules are also shifting. Newer credit scoring models, like Vantage, have started to take rent history into account, where traditional models often did not. That can help some borrowers, though rent history alone does not replace the full debt-to-income picture a lender has to build. If you want to understand how much these models can diverge, we break it down in our post on FICO vs. Vantage credit scores. The smartest move is to have a professional map your DTI before you start shopping, so you know your real number going in.

The Bigger Picture

Paying rent on time tells a landlord you are reliable. Qualifying for a mortgage is a different question, and it rewards understanding your debt-to-income before you fall in love with a house. Know your numbers ahead of time and you can pay down the right debts, structure your offer correctly, and avoid being told no on something that felt like an easy yes.

Glenn Groves

Mortgage Broker | GTG Financial | Santa Rosa, CA

NMLS #1124642 | gtgfi.com

GTG Financial, Inc. NMLS #1595076 | CA DRE #02029711. Equal Housing Opportunity. Not a commitment to lend. Subject to credit approval and underwriting. Individual results vary based on credit profile, loan amount, property type, and other factors. nmls consumeraccess.org

Related Posts