Introduction As the end of July approaches, many families are preparing for the back-to-school season.…

Self-Employed Mortgage Planning

June 2026 | GTG Financial | Santa Rosa, CA

TL;DR: What’s in This Post

- Why self-employed borrowers need to start the mortgage conversation years before they are ready to buy

- How traditional tax-return-based qualifying works against self-employed income and what to do about it

- What a bank statement loan is and when it makes sense

- What a planning conversation with a mortgage broker actually looks like at the two- or three-year mark

Most self-employed borrowers wait. They assume the conversation starts when things look cleaner — when income is more stable, when the business has been running longer, when they actually feel ready to buy. By the time that moment arrives, the window to set things up correctly has usually passed. The work that makes a mortgage possible for a self-employed borrower almost always happens years before the purchase.

Why Self-Employed Borrowers Need to Start Earlier

Self-employed income does not qualify the same way W-2 income does. Traditional mortgage approval uses your tax returns — typically two years — to establish income, then averages that number. If your income is growing, year one pulls down what a lender will count in year three. If you have not been self-employed for at least two years, many conventional loan programs will not count that income at all.

None of that is a problem that fixes itself once you decide you are ready to buy. It is a problem you solve in advance, by understanding what your documentation will look like at the time of purchase and making decisions now that put you in a stronger position later. That might mean how you are structuring your business, how you are managing deposits, or simply understanding that a bank statement loan may be the better path and what you need to do to prepare for it.

A mortgage professional can look at your taxes, your income trajectory, and your plans and tell you exactly what needs to happen over the next two or three years. That roadmap is the whole point of an early conversation. Most borrowers who come in already in the buying window do not have time to change anything. The ones who come in two or three years out almost always have options.

What a Bank Statement Loan Actually Is

For self-employed borrowers, a bank statement loan is worth understanding early. Instead of qualifying based on tax returns, this loan type uses 12 to 24 months of bank statements to establish income. The lender averages your deposits over that period and uses that number to qualify you.

This matters because self-employed borrowers often write off significant business expenses, which reduces their taxable income — exactly what helps at tax time but hurts when a lender is looking at what you bring home on paper. A bank statement loan looks past the return and at the actual cash flowing through the business. If deposits tell a different story than the tax return, this program accounts for that.

It is also a multi-year process to position yourself well for it. The deposit history needs to be there, consistent, and clean. Understanding that you are heading toward a bank statement loan changes how you think about managing your accounts in the years leading up to a purchase. The earlier you know that is the route, the more time you have to set it up right.

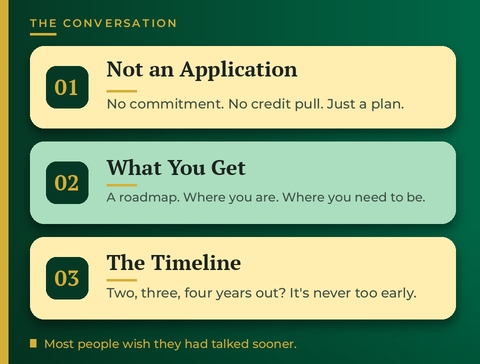

What the Conversation Looks Like

The planning conversation is not a mortgage application. There is no commitment, no credit pull unless you want one, and no pressure to be further along than you are. It is a strategy session: here is where you are, here is where you need to be, and here is what the path looks like to get there.

If you are two, three, or four years out, that conversation can be 20 minutes. You walk away with a clear picture of what your income documentation will look like, whether a bank statement loan or a conventional loan makes more sense for your situation, and what decisions between now and then will move the needle. That is information you can actually use.

The most common thing we hear from self-employed borrowers who come in close to ready is that they wish they had come in sooner. Not because the loan is impossible — often it is not — but because a conversation two years earlier would have changed a few decisions that made things harder than they needed to be. It is never too early to know what the path looks like.

The Bigger Picture

Self-employed borrowers have more options than they often think. A bank statement loan exists precisely because traditional documentation does not always reflect what a successful business owner actually earns. But taking advantage of those options requires knowing they exist and positioning yourself for them in advance. That process starts with a conversation, not a contract.

If you are self-employed and thinking about buying — even if it feels like years away — that is exactly when to reach out. The earlier the conversation happens, the more it can actually help.

Glenn Groves

Mortgage Broker | GTG Financial | Santa Rosa, CA

NMLS #1124642 | gtgfi.com

GTG Financial, Inc. NMLS #1595076 | CA DRE #02029711. Equal Housing Opportunity. Not a commitment to lend. Subject to credit approval and underwriting. Individual results vary based on credit profile, loan amount, property type, and other factors. nmls consumeraccess.org

Related Posts