Understanding Mid-Summer Mortgage Trends The peak of summer is upon us, and with it comes…

Seller Concessions vs. a Price Reduction – Take the Credit

July 2026 | GTG Financial | Santa Rosa, CA

TL;DR: What’s in This Post

- The price-vs-credit reframe: same to the seller, different for you

- Why knocking $1,000 off the price only saves about $7 a month

- How to put a concession to work: closing costs, rate buydown, repairs

- The IPC limits, and when a price reduction actually wins

There is a simple negotiation move that most buyers never think to make, and it can quietly save you far more than shaving money off the price. It is called a seller concession, and knowing when to ask for one instead of a price reduction is one of the highest-leverage decisions in the whole purchase.

Seller Concessions vs. a Price Reduction

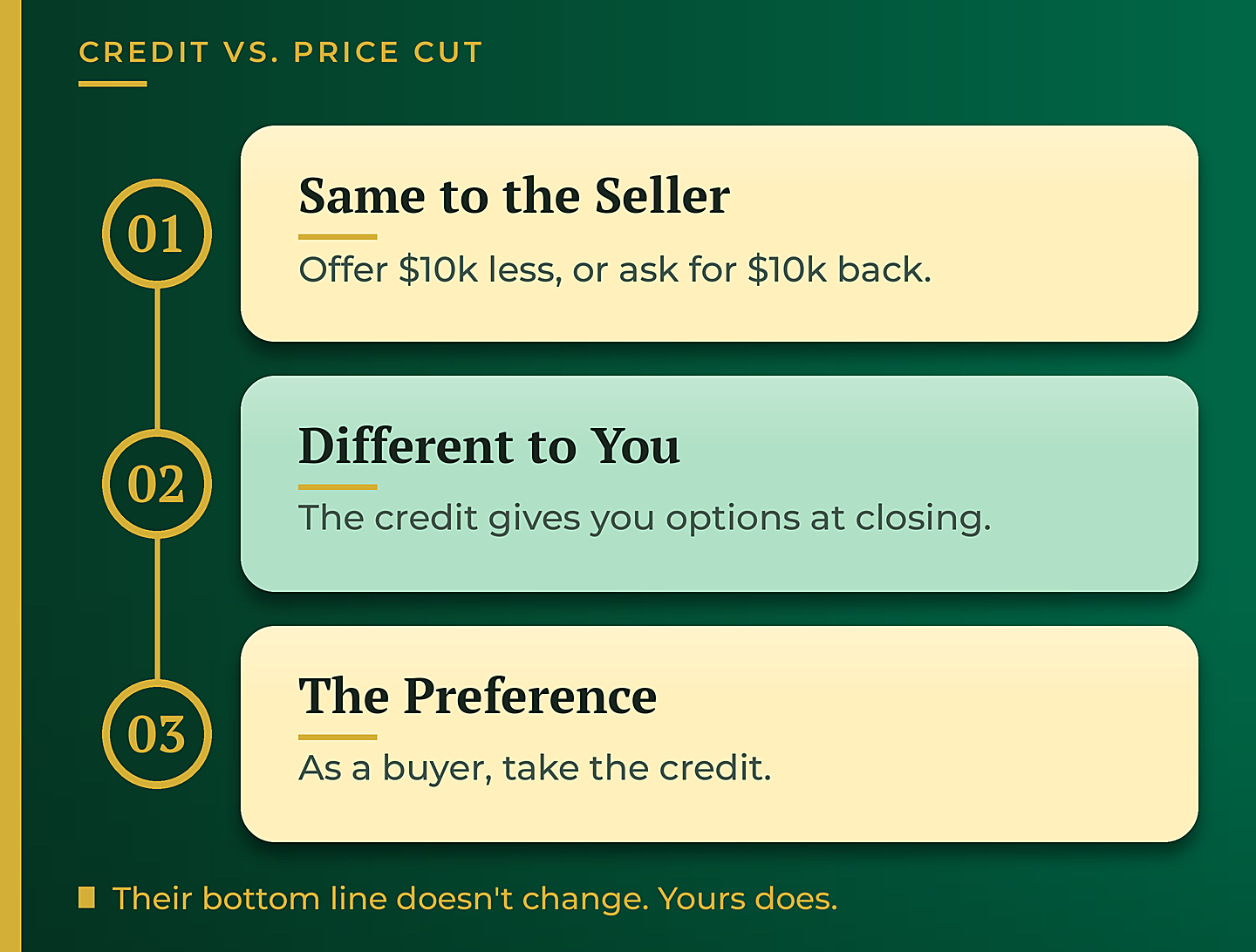

Here is the setup. Say a house is listed at $700,000. A lot of buyers instinctively offer $690,000. That is fine, but you could also offer the full $700,000 and ask the seller for $10,000 back as a credit. To the seller, the bottom line is exactly the same either way. They net the same money.

For you, though, the two are not the same at all. A price reduction just lowers the number. A credit is cash you can point at whatever you actually need. That flexibility is the entire reason a smart buyer usually prefers the concession.

The Math: Why a Price Cut Barely Moves Your Payment

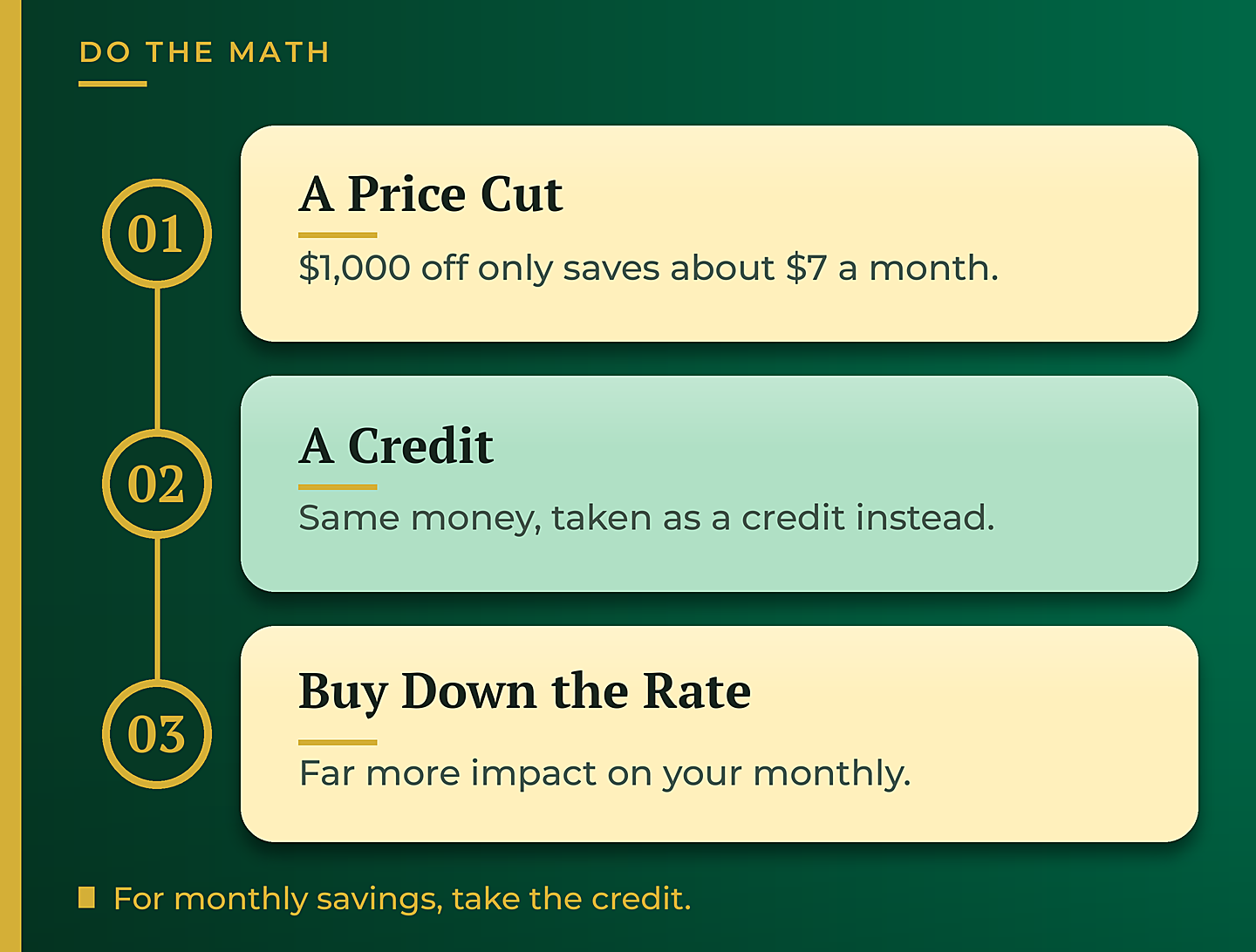

Run the numbers and it becomes obvious. Every $1,000 you knock off the purchase price, with the same loan structure, only lowers your monthly payment by about seven dollars. So a $10,000 price cut saves you roughly seventy dollars a month.

If your real goal is a lower monthly payment, you do not want the price cut. You want the credit at the same price, and you use it to buy down your interest rate. Dollar for dollar, buying down the rate does far more for the monthly than shaving the price ever will.

The dollar figures above are an illustrative example, not a quote. Rates shown are illustrative only and do not represent current available rates. Contact Glenn Groves for details on your situation.

What You Can Actually Do With a Concession

A concession is really just a credit, and there is very little you cannot do with it. You can use it to cover your closing costs so you bring less cash to the table. You can use it to buy down your interest rate, temporarily or permanently, through a seller-paid buydown.

It does not even have to be negotiated up front. Often a concession shows up halfway through the deal: inspections turn up a little dry rot or a gutter that needs fixing, and rather than reprice the home, the agents negotiate a credit. In the buyer’s eyes, that is simply less money you have to bring at closing, either to fix the issue or to keep.

The Limits (and When a Price Cut Wins)

Concessions are not unlimited. There is a cap called the interested party contribution limit, or IPC, and it ranges from roughly 3% to 9% of the purchase price depending on how much you are putting down and the loan program. At the prices we see locally, most buyers never run into it, but it is worth knowing.

And a price reduction is not always the wrong call. If you do not need the extra cash and the home is in great shape, a lower price will slightly lower your property tax basis over the years. It is situational. But when you are dealing with a few thousand dollars, the rule of thumb is simple: take the credit.

The Bigger Picture

Price and credit can look identical to the seller and be completely different for you. The smart move is to decide what you actually need, whether that is more cash at closing, a lower rate, or a lower long-term basis, and then structure the offer around that goal.

If you want to see how a concession could work on a specific home, or how buying down the rate would change your payment, reach out and we will run the numbers with you.

Glenn Groves

Mortgage Broker | GTG Financial | Santa Rosa, CA

NMLS #1124642 | gtgfi.com

The dollar figures in this article are an illustrative example, not a quote. Rates shown are for illustrative purposes only and do not represent current available rates. Seller concession and interested party contribution limits vary by loan program, occupancy, and down payment. Contact Glenn Groves for current rate information. GTG Financial, Inc. NMLS #1595076 | CA DRE #02029711. Equal Housing Opportunity. Not a commitment to lend. Subject to credit approval and underwriting. nmls consumeraccess.org

Related Posts