July 2026 | GTG Financial | Santa Rosa, CA First-Time Buyer Down Payment: How Little…

FHA Loans in Sonoma County – Who They’re Really For

July 2026 | GTG Financial | Santa Rosa, CA

TL;DR: What’s in This Post

- Why an FHA loan is not only for first-time buyers

- The mortgage insurance detail most people never hear (500 or 850, same cost)

- The 3.5% down move when cash is your tightest factor

- When conventional is actually the better deal for you

There is a persistent myth that FHA loans are only for first-time buyers with shaky credit. The truth is more useful than that. An FHA loan in Sonoma County can be the smartest move for a specific kind of buyer, and there is one detail about the mortgage insurance that most people never hear. Here is who FHA is really for, and who should skip it.

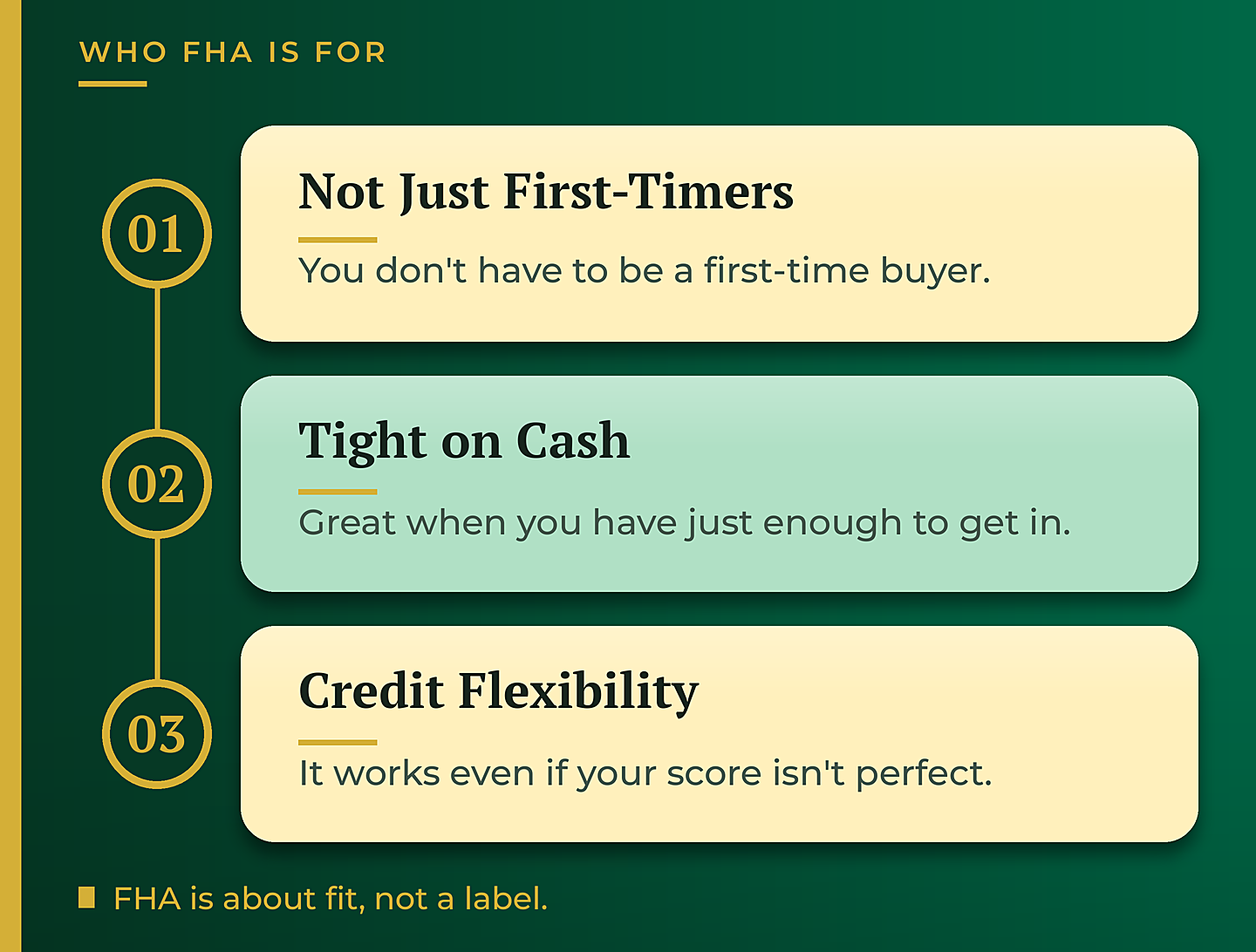

Who an FHA Loan Is Really For

First, the myth. You do not have to be a first-time buyer to use an FHA loan. FHA is often the right fit for someone who has just enough for the down payment, or whose credit score is not quite up to snuff. If money is your tightest constraint, regardless of your credit, FHA is frequently the move.

Part of the reason is the low barrier to entry. FHA asks for as little as 3.5% down. But the bigger reason is what happens with the mortgage insurance, which is where most people are surprised.

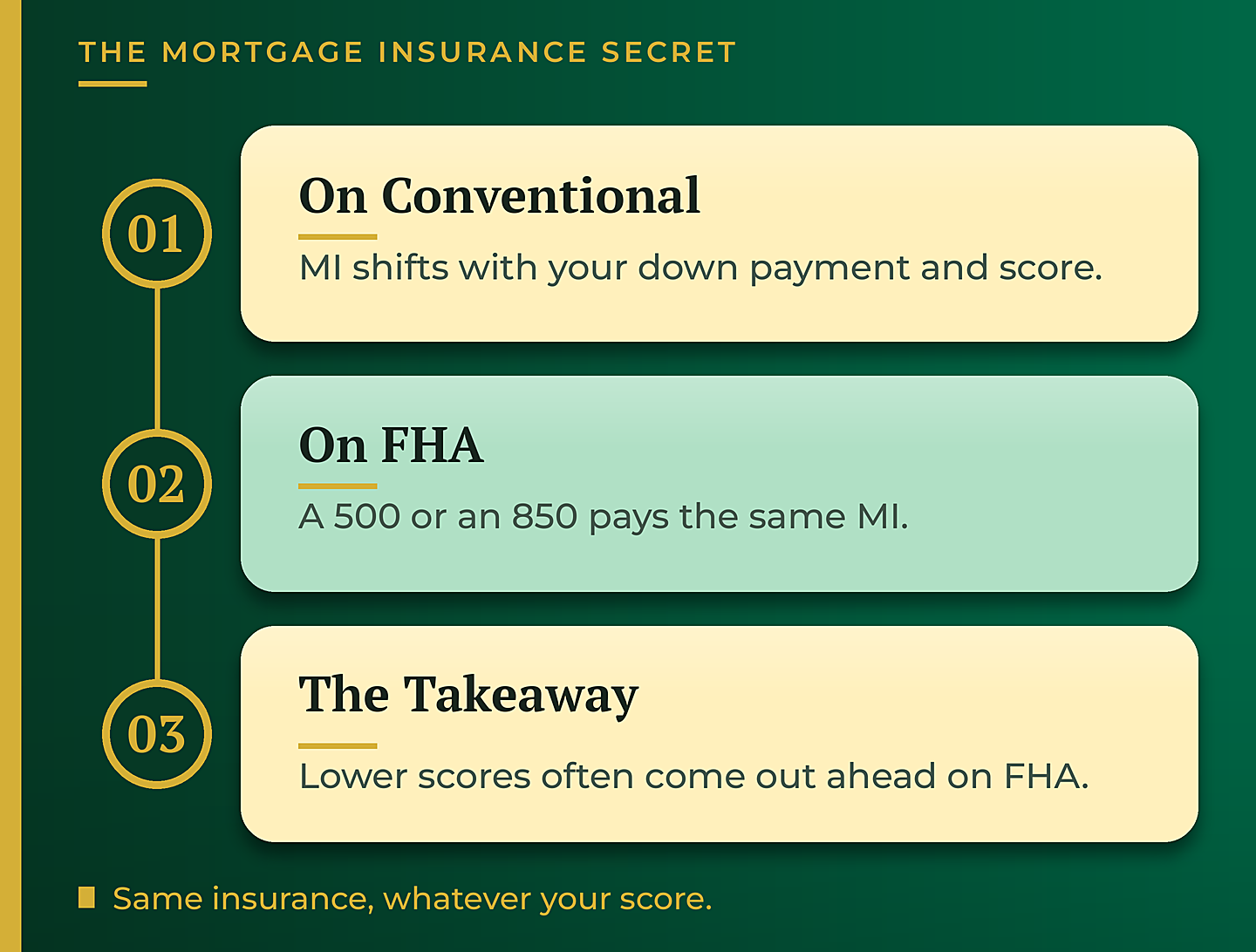

The Mortgage Insurance Most People Miss

Here is the detail that changes the math. On a conventional loan, your mortgage insurance is priced off your down payment and your credit score, so a lower score means a higher monthly cost. On FHA, that is not how it works. You can have a 500 FICO score or an 850, and everybody pays the same mortgage insurance. It does not change based on your credit.

That single fact is why FHA so often wins for buyers with lower or middle credit scores. On conventional, a lower score pays noticeably more for mortgage insurance than a high one. On FHA, they pay the same, so the buyer with the lower score frequently comes out ahead.

Figures and credit-score examples are general and illustrative only, not a guarantee of eligibility or pricing. Rates shown do not represent current available rates. Contact Glenn Groves for details on your situation.

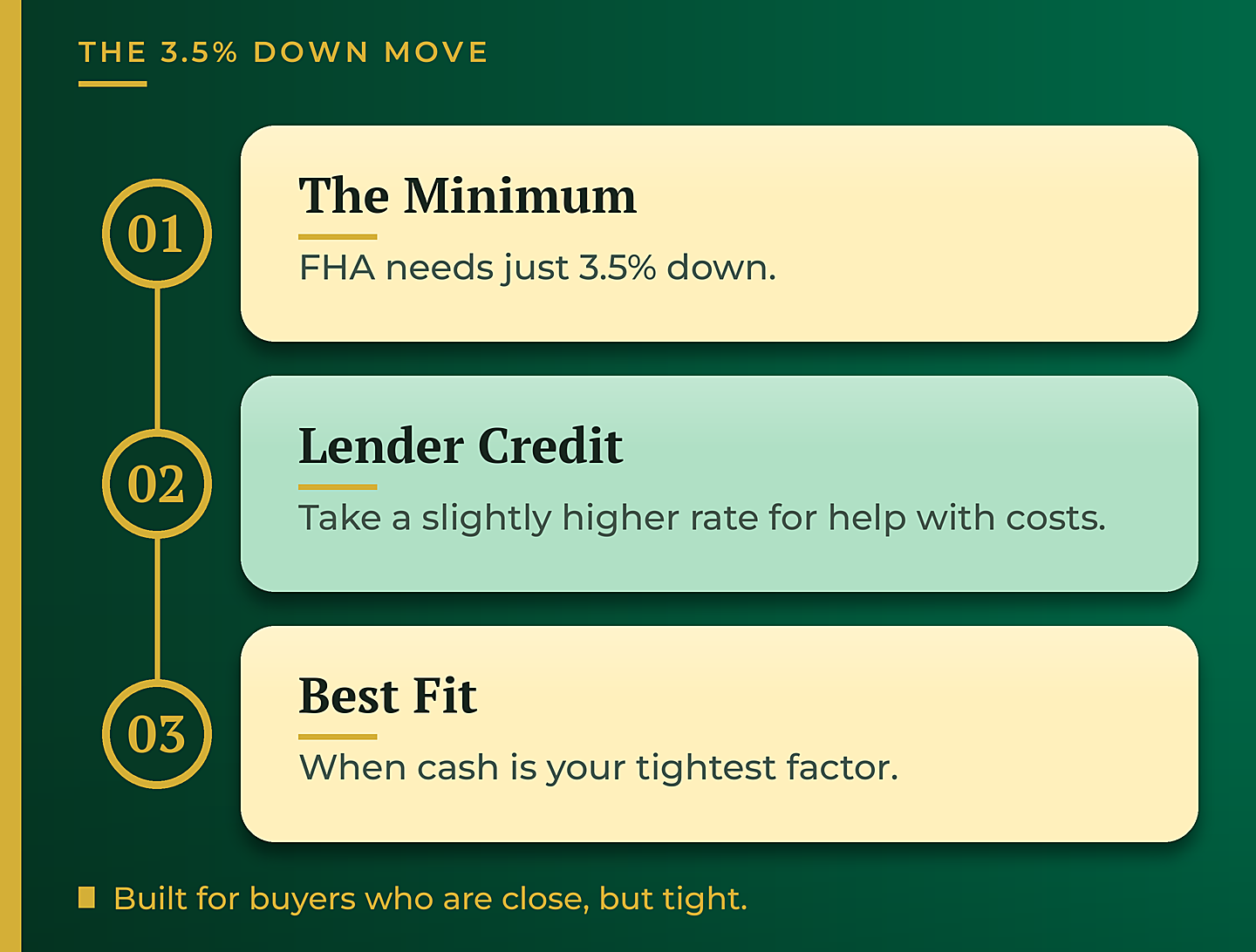

The 3.5% Down Move

When cash is the tightest factor, FHA gives us another lever. We can take a slightly higher than market interest rate and, in exchange, have the lender cover a chunk of your closing costs. It sounds backwards at first, why would you choose a higher rate, but if you have just enough for the down payment and not much left over, that lender credit can be the difference between closing and not closing.

This is the kind of structuring that a broker can shop across lenders. The goal is not the flashiest rate on paper. It is the combination of rate and cost that actually gets you into the home with the cash you have.

When to Skip FHA

FHA is not for everyone. If you have enough for the down payment and the closing costs, and your credit score is above roughly 740 or 760, conventional is usually the better deal. At that point your conventional mortgage insurance is inexpensive, and you avoid FHA’s structure entirely.

This is exactly why we never just hand someone one option and say they fit in a box. We put FHA and conventional side by side so you can see which one actually wins for your numbers. It might be FHA. But you should see why.

The Bigger Picture

FHA is not a consolation prize or a first-timer’s loan. It is a tool, and for the right buyer in Sonoma County it can be the best tool on the table. The only way to know is to compare it honestly against conventional, with your real numbers, before you fall in love with a house.

Learn more about our FHA loan options, or reach out and we will run the side-by-side comparison for you.

Glenn Groves

Mortgage Broker | GTG Financial | Santa Rosa, CA

NMLS #1124642 | gtgfi.com

Credit-score examples and figures are general and illustrative only and are not a guarantee of eligibility, approval, or pricing. Rates shown are for illustrative purposes only and do not represent current available rates. FHA loan eligibility and terms are subject to FHA guidelines. Contact Glenn Groves for current rate information. GTG Financial, Inc. NMLS #1595076 | CA DRE #02029711. Equal Housing Opportunity. Not a commitment to lend. Subject to credit approval and underwriting. nmls consumeraccess.org

Related Posts