July 2026 | GTG Financial | Santa Rosa, CA TL;DR: What's in This Post The…

HELOC vs Cash-Out Refinance (Marin HELOC Deal Deep Dive)

July 2026 | GTG Financial | Santa Rosa, CA

HELOC vs Cash-Out Refinance: How to Tap Your Home Equity Without Losing Your Low Rate

A HELOC lets you borrow against your home equity through a second loan, so your first mortgage and its low rate stay completely untouched. A cash-out refinance does the opposite: it replaces your entire mortgage, which means trading a low pandemic-era rate for today’s higher one across your whole balance. For a homeowner with a rate worth protecting, a HELOC is usually the smarter way to access equity.

Reviewed by Glenn Groves, Mortgage Broker, NMLS #1124642 · GTG Financial, Inc. NMLS #1595076 · Serving Sonoma, Marin, and the greater North Bay.

TL;DR: What’s in This Post

- Why a cash-out refinance can cost you your low rate

- How a HELOC lets you tap equity while keeping your first mortgage

- A side-by-side comparison of a HELOC and a cash-out refinance

- The catch: it’s an adjustable rate tied to the prime rate

- When a HELOC makes sense: improvements and debt consolidation

Millions of homeowners locked in a mortgage rate during the pandemic that they may never see again. So when they need cash, whether for a remodel, a pool, or to pay off high-interest debt, they hit a frustrating question: do I have to give up my great rate to get at my own equity? The answer is no. Here is a real Marin County example, and the tool that makes it possible.

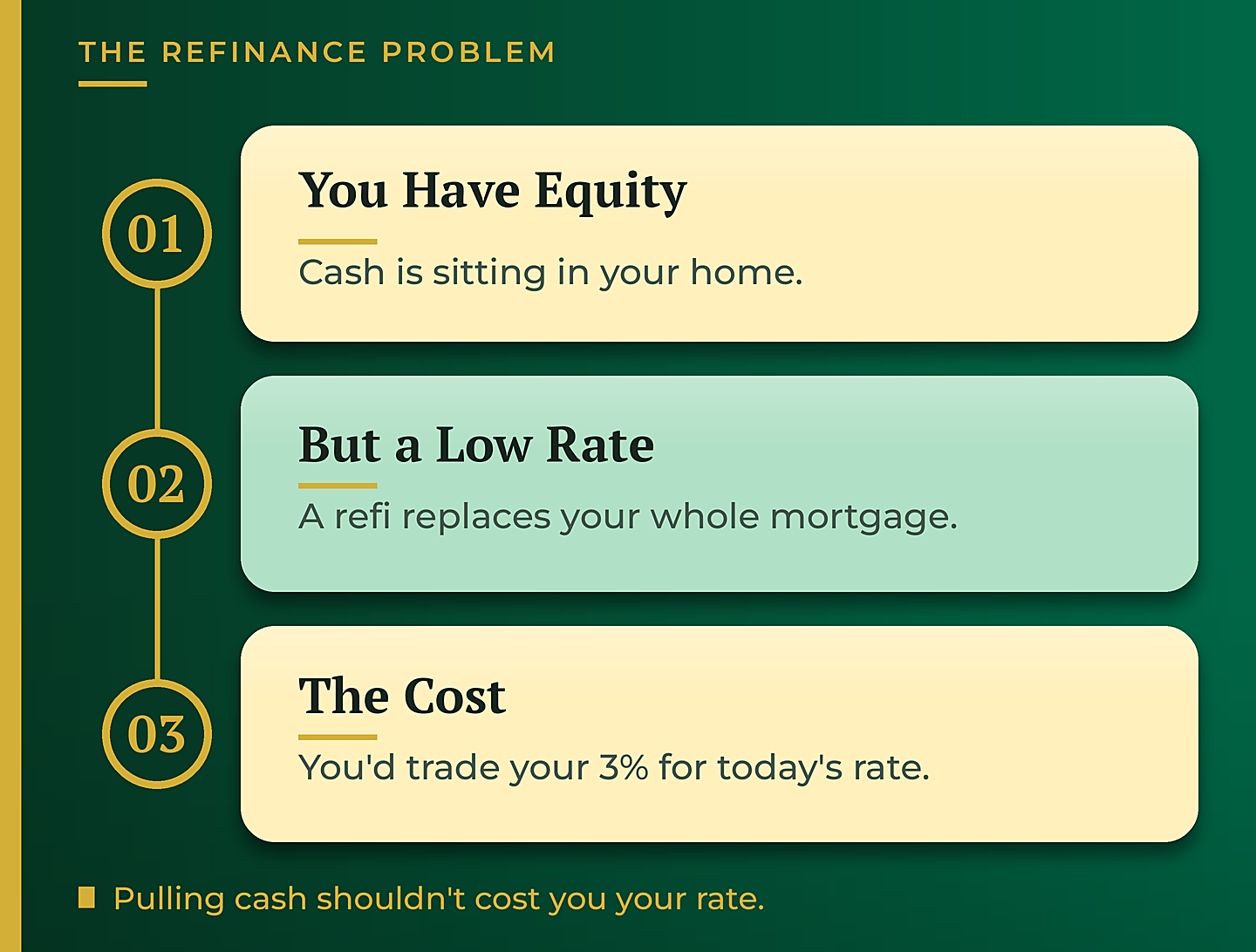

Why a Cash-Out Refinance Doesn’t Always Make Sense

Our Marin County client had a home worth about $1 million and only owed around $500,000. That is a huge equity position, and they wanted to use some of it to put in a pool. The instinctive move is a cash-out refinance: you replace your current mortgage with a new, larger one and pocket the difference.

But there is a catch. Their existing loan carried a Covid-era interest rate of 3%. A refinance would have wiped that out and replaced it with today’s higher rate across the entire balance. And here is where it gets expensive: every extra percentage point of rate on a $500,000 balance is roughly $5,000 a year. Refinancing the whole balance just to free up $100,000 could add thousands of dollars a year in interest on money they already had cheaply. For a relatively small amount of cash, that is a terrible trade.

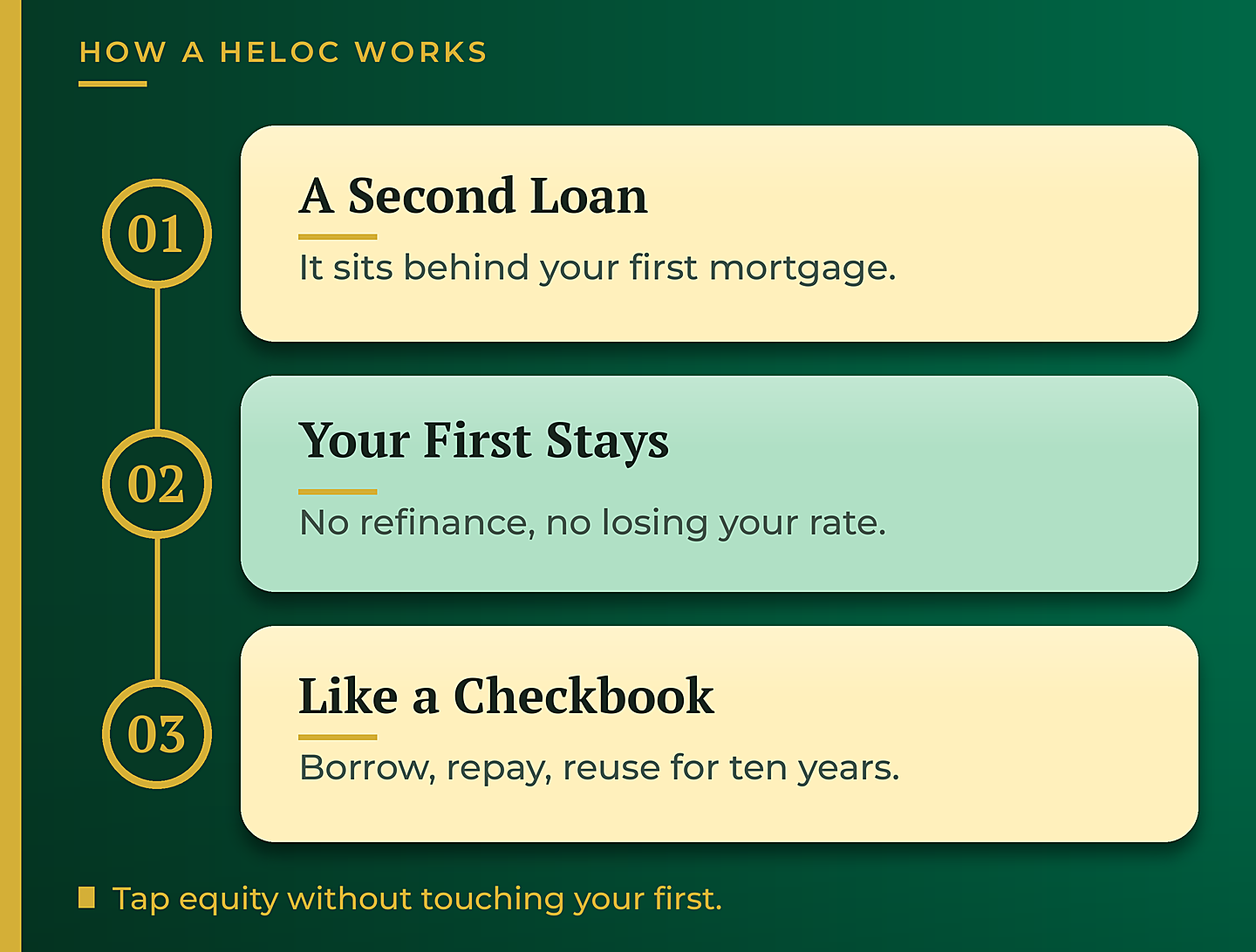

The HELOC: A Second Loan That Leaves Your First Alone

So instead of refinancing, we left their first mortgage completely untouched and added a second loan on top: a HELOC, or home equity line of credit. Think of it like a checkbook on your house. We opened a $100,000 line, and their 3% first mortgage never moved.

A HELOC is a revolving line of credit, which means you can draw on it, pay it back down, and draw again during the draw period, usually about ten years. You only pay interest on what you actually use. That flexibility is what makes it such a useful tool for equity-rich homeowners who do not want to disturb a great first-mortgage rate.

HELOC vs Cash-Out Refinance at a Glance

Both let you turn equity into cash, but they work in fundamentally different ways. Here is how they compare for a homeowner who already has a low first-mortgage rate.

| HELOC | Cash-Out Refinance | |

|---|---|---|

| Your first mortgage | Stays exactly as it is | Replaced with a new, larger loan |

| Your low rate | Protected | Lost on the entire balance |

| Rate type | Adjustable, tied to the prime rate | Usually fixed |

| How you access it | Revolving line: borrow, repay, reuse | One lump sum at closing |

| Best for | Homeowners with a rate worth protecting | When your current rate is already high |

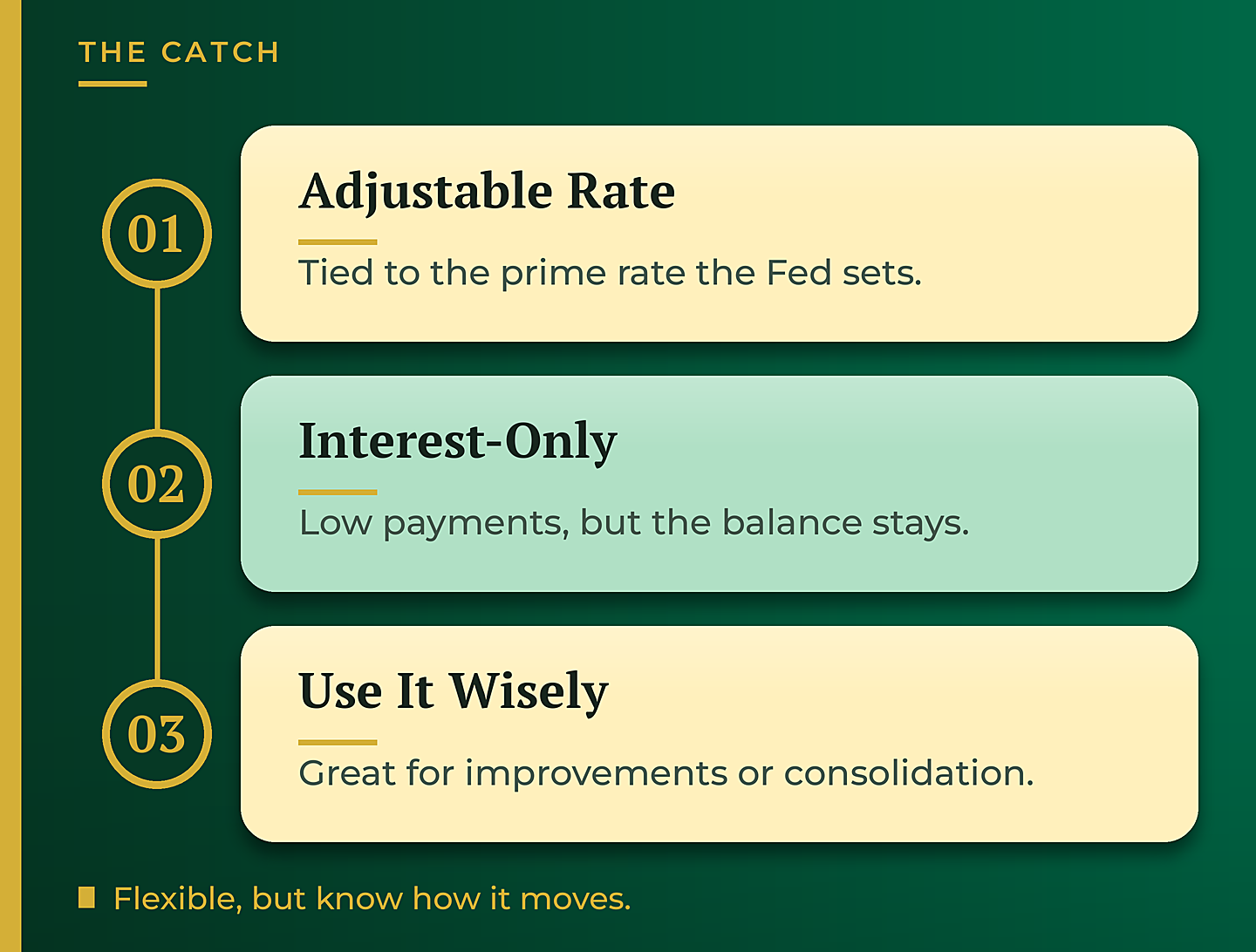

The Catch: It’s an Adjustable Rate

A HELOC is not a free lunch, and it is important to understand how it behaves. The rate is adjustable, usually tied to the prime rate, which is what the Federal Reserve influences. So when you hear that the Fed is moving rates, a HELOC payment can move with it.

The payments are also typically interest-only during the draw period. That keeps them low, but it also means the balance does not shrink unless you pay extra. On a line this size, a rate change usually moves the payment by a modest amount, but you should still go in with your eyes open about how the product works.

This is a real deal example shared for educational purposes. Individual results, rates, and terms vary. HELOCs are adjustable-rate and tied to an index such as the prime rate. Rates and figures shown are illustrative only and do not represent current available rates. Contact Glenn Groves for current rate information.

When a HELOC Makes Sense

A HELOC shines in a specific situation: you have real equity, and you have a first-mortgage rate worth protecting. Home improvements are the classic use, but so is debt consolidation. If someone is carrying $50,000 or $60,000 in credit card debt costing them around $2,000 a month, moving it onto a HELOC might drop that to a few hundred dollars a month.

The relief is real, but there is a discipline to it: that freed-up cash should go toward paying the line down faster, not toward taking on new spending. Used well, a HELOC is one of the most flexible tools available to a homeowner. It is also a common move across the North Bay, where longtime owners in Sonoma and Marin are often sitting on years of equity behind a rate they locked in during the pandemic.

Frequently Asked Questions

Can I get a HELOC without refinancing my first mortgage?

Yes. A HELOC is a second loan that sits behind your first mortgage, so your existing loan and its rate stay completely untouched. That is the entire reason to choose one when you already have a low rate.

Is a HELOC a fixed or adjustable rate?

A HELOC is typically adjustable, usually tied to the prime rate, which the Federal Reserve influences. When the Fed moves rates, your HELOC payment can move with it. A cash-out refinance, by contrast, is usually a fixed rate.

Is a HELOC cheaper than a cash-out refinance?

It depends on your current rate. If you locked in a low first-mortgage rate, a cash-out refinance replaces that rate on your entire balance, which can cost thousands of dollars a year. A HELOC only charges interest on the smaller amount you actually borrow, while leaving the low first-mortgage rate in place.

How long can I use a HELOC?

Most HELOCs have a draw period of about ten years, during which you can borrow, repay, and borrow again on the line. Payments during that period are often interest-only, so the balance does not shrink unless you pay extra.

The Bigger Picture

You do not have to choose between keeping your low rate and using your equity. For the right homeowner, a HELOC lets you do both. The key is having genuine equity and a first-mortgage rate that is worth protecting, then structuring the second loan so it fits your goal.

If that sounds like your situation, it is worth running the numbers on what a line could do for you. Reach out and we will map it to your specific home and rate.

Glenn Groves

Mortgage Broker | GTG Financial | Santa Rosa, CA

NMLS #1124642 | gtgfi.com

This article describes a real deal example shared for educational purposes. Individual results, rates, and terms vary by borrower and situation. HELOCs are adjustable-rate and tied to an index such as the prime rate, so payments can change over time. Rates shown are for illustrative purposes only and do not represent current available rates. Contact Glenn Groves for current rate information. GTG Financial, Inc. NMLS #1595076 | CA DRE #02029711. Equal Housing Opportunity. Not a commitment to lend. Subject to credit approval and underwriting. nmls consumeraccess.org

Related Posts