July 2026 | GTG Financial | Santa Rosa, CA First-Time Buyer Down Payment: How Little…

The Market Isn’t Waiting on a Cut. It’s Waiting on Wednesday.

June 2026 | GTG Financial | Santa Rosa, CA

TL;DR: What’s in This Post

- Why Friday’s jobs report shifted the rate cut conversation

- How the Federal Reserve and mortgage rates actually work

- Where rate cut expectations stand right now

- Why Wednesday’s May CPI report is the number that matters most

Whatever number you had for Federal Reserve rate cuts this year, the market just lowered it. Friday’s jobs report came in stronger than almost anyone expected, and it changed the math on when, or whether, rates are coming down. Here is what it means for buyers who are waiting.

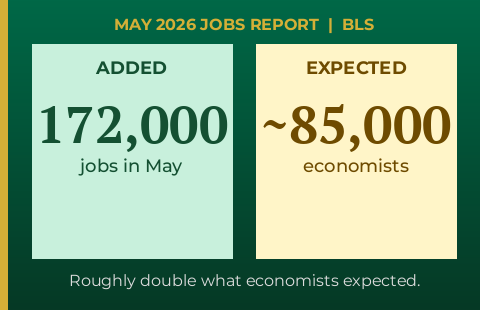

Friday’s Jobs Report Came In Hot

The economy added 172,000 jobs in May, according to the Bureau of Labor Statistics. That is roughly double what economists had expected. Job gains were led by leisure and hospitality, local government, and health care.

Strong job numbers are generally good news for the economy. But for buyers waiting on mortgage rates to drop, a hot jobs report is the wrong kind of good news. A strong labor market means the Federal Reserve has less pressure to cut rates. And when the Fed has less pressure to cut, mortgage rates stay higher for longer.

That is the connection between Friday’s report and your rate outlook right now.

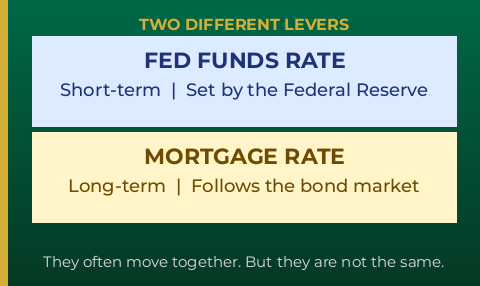

The Federal Reserve Does Not Set Your Mortgage Rate

This is one of the most common misunderstandings in real estate. The Federal Reserve sets the federal funds rate, which is a short-term rate that governs what banks charge each other to borrow overnight. That is not your mortgage rate.

Mortgage rates follow the bond market, specifically the yield on the 10-year U.S. Treasury. The two often move in the same direction, which is why people link them. But they are different levers. The Fed can hold its rate steady while mortgage rates move up or down based on what bond investors are pricing in about future inflation and growth.

Right now, futures markets are pricing in over a 95% chance the Fed holds steady at its next meeting, according to CME FedWatch. That is not a surprise given how strong Friday’s jobs number was.

Rate Cut Expectations Have Shifted

A few months ago, the conversation in financial markets was about how many Federal Reserve cuts to expect in 2026. Now the conversation has changed. Some are asking whether we get any cuts at all this year. A handful of market participants are even floating the possibility of a rate hike if inflation stays elevated.

That is a significant shift. And it matters for mortgage rates because the bond market, which drives those rates, prices in expectations about the future. If the market stops expecting cuts and starts pricing in holds or hikes, mortgage rates do not have a clear reason to fall.

That is the environment buyers are navigating right now.

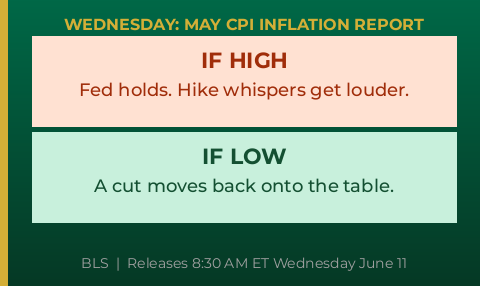

Why Wednesday Is the Number That Actually Matters

Wednesday morning, the Bureau of Labor Statistics releases the May inflation report. This is the Consumer Price Index, or CPI, and it is the single most important data point for the rate outlook right now.

If inflation comes in high, the Federal Reserve has even more reason to hold. Hike talk gets louder. Mortgage rates stay elevated or move higher. If inflation comes in low, a rate cut moves back onto the table and the bond market could respond by pulling rates down.

The jobs report told us the economy is still running. Wednesday’s inflation report will tell us what that economy is doing to prices. Those two things together will shape where rates go from here.

What This Means for Buyers Waiting on Rates

If you have a buyer who is waiting on rates to drop before making a move, here is the honest version of where things stand. The market is not waiting on a Fed cut anymore. It is waiting on Wednesday.

One inflation report will not resolve everything. But it will tell us which direction the next few months are likely to go. That is worth watching closely, and it is worth making sure your buyers understand what they are actually waiting on and why.

For the full weekly breakdown of what is moving rates, subscribe to GTG Weekly. Published every Monday, free.

Glenn Groves

Mortgage Broker | GTG Financial | Santa Rosa, CA

NMLS #1124642 | gtgfi.com

GTG Financial, Inc. NMLS #1595076 | CA DRE #02029711. Equal Housing Opportunity. Not a commitment to lend. Subject to credit approval and underwriting. Employment figures sourced from the Bureau of Labor Statistics Employment Situation Summary, May 2026. Rate probability figures sourced from CME FedWatch. Not a guarantee of future rate movement. nmls consumeraccess.org

Related Posts