Introduction As we move deeper into the summer months, the real estate market often experiences…

Pre-Qualified vs Pre-Approved

July 2026 | GTG Financial | Santa Rosa, CA

Pre-Qualified vs Pre-Approved: What’s the Difference, and Which Do You Need?

A pre-qualification is an informal estimate based on what you tell a lender, with nothing verified. A pre-approval means your income, assets, credit, and debts have all been checked, so a seller knows you can actually close. For making real offers, pre-approved is the level you want.

Reviewed by Glenn Groves, Mortgage Broker, NMLS #1124642 · GTG Financial, Inc. NMLS #1595076 · Serving Sonoma, Marin, and the greater North Bay.

TL;DR: What’s in This Post

- What “pre-qualified” really means (almost nothing is verified)

- What “pre-approved” means: full verification a seller can trust

- The three stages side by side, including fully underwritten

- Why a broker may skip the fully underwritten pre-approval

- Which level you actually need to make strong offers

The lingo in real estate trips up a lot of first-time buyers, and pre-qualified versus pre-approved is one of the most confusing pairs of all. They sound almost identical, but they carry very different weight when you sit down to make an offer. Here is what each one actually means, in plain English.

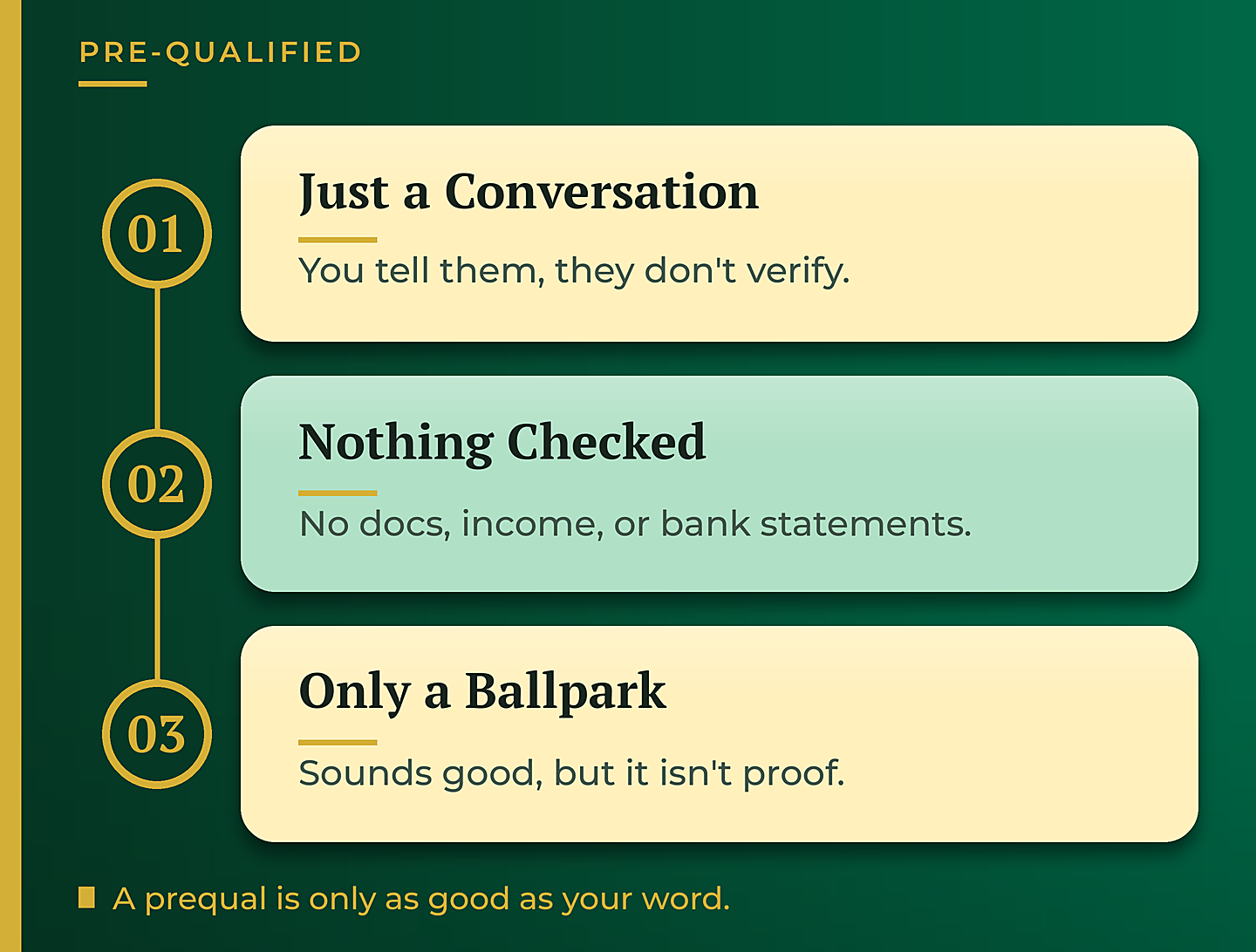

What “Pre-Qualified” Really Means (Almost Nothing)

A pre-qualification is a conversation, and not much more. We have a phone call, you explain your situation, and it sounds good. But at that point I have not seen any documents. I have not verified your bank statement, your income, or anything else. Everything you told me sounded fine, and that is all a prequal is built on.

That is why real estate agents tend to give a prequal letter very little weight. They understand the difference, and they will often call the lender to ask what was actually checked. A pre-qualification is only as good as your word, which is exactly why it does not carry you very far in a competitive offer.

What “Pre-Approved” Means: Full Verification

Pre-approved is a different animal. It means full verification of all the major pieces: what you do for a living, how much cash you have to work with, your credit score, and what kind of debts you carry. Instead of taking your word for it, we collect and review the documentation behind each one.

That verification is what makes a pre-approval letter something a seller can actually trust. In a competitive North Bay market, that trust is often what separates a winning offer from one that gets passed over. This is the level we take our borrowers to before they start writing offers.

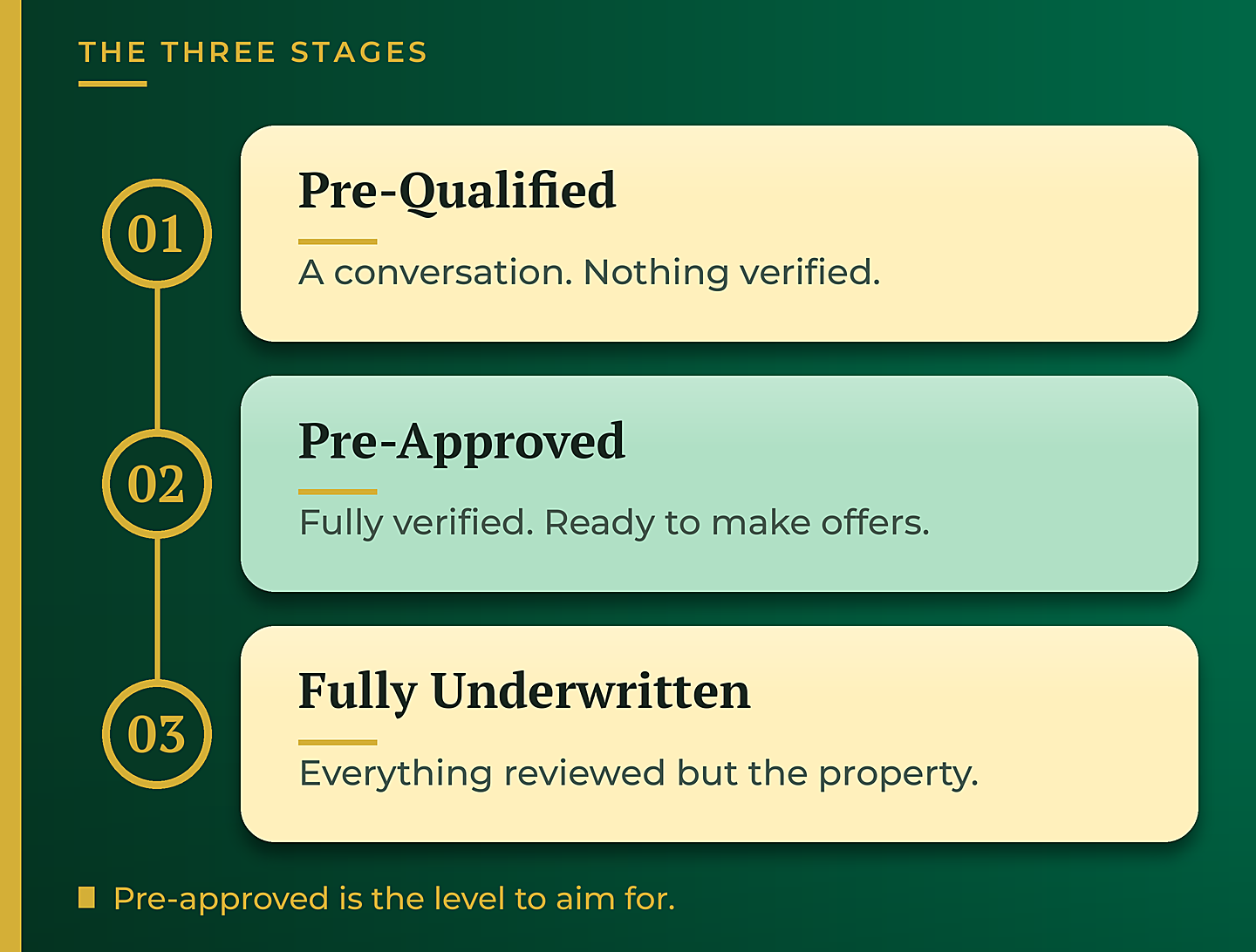

The Three Stages at a Glance

It helps to see all three levels side by side. Pre-qualified and pre-approved are the two most people compare, but there is a third stage, fully underwritten, that sits above them.

| Pre-Qualified | Pre-Approved | Fully Underwritten | |

|---|---|---|---|

| What happens | A conversation | Full document review | Sent to a lender to underwrite |

| What’s verified | Nothing | Income, assets, credit, debts | Everything but the property |

| Strength to a seller | Weak | Strong | Strongest on paper |

| Best for | A rough ballpark | Making real offers | Rare, tricky income cases |

The Third Stage: Fully Underwritten (and Why a Broker May Skip It)

Above pre-approved sits a fully underwritten pre-approval, sometimes called a TBD underwrite, for “to be determined” property. We take a borrower’s full file, review it in house, then send it to a lender who underwrites everything except the property itself, because there is no property yet.

A lot of agents are surprised to hear me say this, but I usually do not push a fully underwritten pre-approval. Here is why. As a broker, I have multiple lenders I can go to, and I want to keep playing the field for you until you are actually in contract. If I fully underwrite the file with one lender up front, I have essentially chosen that lender already, and I lose the flexibility to move if a better option appears. There are exceptions, like an unusually tricky income situation, but for most buyers the fully underwritten step trades away flexibility for very little extra benefit.

So Which One Do You Actually Need?

Of the three stages, pre-qualified, pre-approved, and fully underwritten, pre-approved is sufficient. It is what you need, and it allows complete flexibility. It is strong enough that sellers take your offer seriously, and light enough that we can still shop lenders on your behalf right up until you are in contract.

So the practical move is simple: get pre-approved before you start shopping. You will write stronger offers, you will move faster when you find the right home, and you will keep every option open behind the scenes.

Frequently Asked Questions

What is the difference between pre-qualified and pre-approved?

A pre-qualification is a conversation where you tell a lender about your finances and nothing is verified. A pre-approval means your income, assets, credit, and debts have all been documented and checked, so a seller can trust that you are able to close.

Is a pre-approval a guarantee I will get the loan?

No. A pre-approval is a strong, verified indication of what you qualify for, but it is not a commitment to lend. Final approval still depends on the property, updated documentation, and underwriting at the time of your actual purchase.

Do I need to be fully underwritten to make an offer?

Usually not. For most buyers, a pre-approval is enough to make strong offers. A fully underwritten pre-approval can help in unusually tricky income situations, but it is not required, and it can lock you into a single lender earlier than you need to be.

Why might a broker skip a fully underwritten pre-approval?

A broker works with multiple lenders and wants to keep shopping for the best terms until you are in contract. Fully underwriting your file with one lender up front effectively chooses that lender early and gives up that flexibility.

The Bigger Picture

Pre-qualified, pre-approved, and fully underwritten are not just jargon, they are three different levels of proof. Knowing which one you actually need saves you time, makes your offers stronger, and keeps you in control of the process.

If you are getting ready to buy, the best first step is a real pre-approval. Reach out and we will get you verified, keep your options open, and make sure your offer stands out when it counts.

Glenn Groves

Mortgage Broker | GTG Financial | Santa Rosa, CA

NMLS #1124642 | gtgfi.com

This article is for educational purposes and is not financial advice. A pre-approval is not a commitment to lend or a guarantee of financing; verification requirements, terms, and eligibility vary by borrower and situation, and final approval is subject to underwriting. Glenn Groves NMLS #1124642 | GTG Financial, Inc. NMLS #1595076 | CA DRE #02029711. Equal Housing Opportunity. nmls consumeraccess.org

Related Posts