Introduction As the end of July approaches, many families are preparing for the back-to-school season.…

Still Waiting to Buy?

May 2026 | GTG Financial | Santa Rosa, CA

TL;DR: What’s in This Post

- The one question that usually reframes the whole decision for buyers on the sidelines

- Why waiting for rates or the market rarely works out the way people expect

- What renting is actually costing you versus what a mortgage locks in

- The two things that actually matter when deciding whether to buy

A lot of people have been sitting on the sidelines for a while now. They watched rates spike. They saw prices hold. They told themselves they would buy when things settled down. And they are still waiting.

I hear this all the time. My response is usually a single question, and it almost always changes the conversation.

The Question That Changes Things

If you knew what you know now, would you have bought five years ago?

Almost everyone says yes. And that is the point. At the time, there were reasons not to. The market felt too hot. Prices seemed unsustainable. There was always something to wait for. In hindsight, the people who bought five years ago are sitting on meaningful equity, locked into a payment that has not changed, while the people who kept renting have watched their monthly costs climb year after year.

We have been waiting for the market to pop for about 15 years now. It has not happened. There is a fundamental supply and demand issue in California that is not going away, especially in Sonoma County and the North Bay. Prices are sticky on the way down and have consistently recovered and moved higher over time.

None of that means you should buy a house just to buy one. The decision still has to make sense for your situation. But if you have been telling yourself the market is going to correct and that is why you are waiting, it is worth asking honestly whether you would have made the same call five years ago, and how that worked out.

What Renting Is Actually Costing You

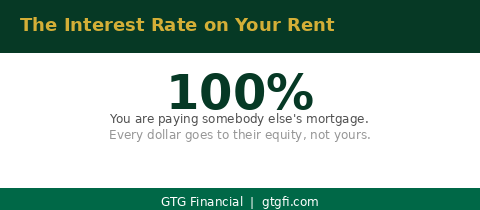

Here is the line I use: the interest rate on your rent is 100%.

Every dollar you pay in rent goes to your landlord’s equity, not yours. There is no amortization working in your favor. There is no appreciation accruing to your balance sheet. You are paying the full cost of housing every month and walking away with nothing to show for it on paper.

A mortgage has interest too, and in the early years it is front-loaded. But there is principal reduction happening, there is potential appreciation working in the background, and there is a fixed principal and interest payment that does not move based on market conditions or a landlord’s decision at renewal time. Rents in Sonoma County have gone in one direction over the past decade. A mortgage payment from 2019 is the same principal and interest payment today.

That is not an argument that renting is always wrong. There are situations where it makes sense. But when someone says they are waiting to buy because rates are too high, I want them to also think about what they are paying right now and whether that cost is going up or staying flat.

What to Actually Focus On

People get very focused on the interest rate when they are thinking about buying. I understand why. It is a visible number and it feels like something you can time. But in practice, trying to time the rate market is something most people get wrong, and it keeps them out of a property that would have been the right decision at the time.

What actually matters comes down to two things. First, what is the monthly payment and are you genuinely comfortable with it? Not stretching, not hoping income catches up, but actually comfortable with what goes out every month. Second, how much cash do you have to work with? Not just the down payment, but closing costs, prepaid items, reserves, and whatever buffer you want to keep after closing.

If both of those boxes check out, and you actually want to live in the property, the rate is a secondary consideration. You can refinance a rate. You cannot go back and buy the house you passed on two years ago at the price it was then.

Where rates are right now, we are in a reasonable range. My expectation is that they continue to hover somewhere between the mid-to-high sixes and the low fives over the coming years. That is not a guarantee and it is not a reason to rush. But it is also not the emergency that some buyers are treating it as. If the payment works and the cash is there, the rate is something you manage over time, not something you wait out indefinitely.

What to Take Away

If you have been sitting on the sidelines, I am not here to pressure you into a decision. Buying a home has to make sense for your situation, your income, your cash, and your life. But if the reason you have been waiting is that you are hoping for a market correction that has not come in 15 years, or a rate drop that may or may not happen on the timeline you need, it is worth having a real conversation about what the numbers actually look like for you right now.

Most of the time when I sit down with someone who has been on the sidelines, the numbers are closer than they think. They have been avoiding the conversation because they assumed it would not work. Sometimes they are right and we put together a plan for six to twelve months from now. More often, there is something we can structure today.

If you are comfortable with the payment and the cash is there, buy the house. You can refinance a rate. You cannot buy back time.

If you are in Sonoma County or the North Bay and want to run the numbers for your situation, reach out. That conversation is free and there is no obligation.

Glenn Groves

Mortgage Broker | GTG Financial | Santa Rosa, CA

NMLS #1124642 | gtgfi.com

GTG Financial, Inc. NMLS #1595076 | CA DRE #02029711. Equal Housing Opportunity. Not a commitment to lend. Subject to credit approval and underwriting. Market conditions and interest rate commentary are illustrative and not a guarantee of future performance. Individual results vary based on credit profile, loan amount, property type, and other factors. nmls consumeraccess.org

Related Posts