June 2026 | GTG Financial | Santa Rosa, CA TL;DR: What's in This Post Why…

The VA Loan Pest Report Myth That’s Costing Veterans Deals in Sonoma County

VA Loans | April 2026 | GTG Financial | Santa Rosa, CA

TL;DR — What’s in This Post

- The pest report myth that steers realtors away from VA buyers

- What the VA minimum property requirements actually say

- How the NPMA-33 form works and when you can use it

- The appraiser caveat that can change the equation

- Why this matters especially in Sonoma County’s older housing stock

- What realtors need to know before advising veteran clients

One of the most common things I hear from realtors working with veteran buyers is some version of this: the house needs a lot of work, the pest report is going to be a problem, we should probably look at something else. Most of the time that advice is well-intentioned. A lot of the time it is also wrong.

There is a specific piece of VA loan guidance that a surprising number of realtors and even some lenders do not know about. It is not a workaround or a gray area. It is written directly into the VA minimum property requirements. And in a market like Sonoma County where a significant portion of the housing stock is approaching sixty years old, it comes up constantly.

The Myth That Is Costing Veteran Buyers Deals

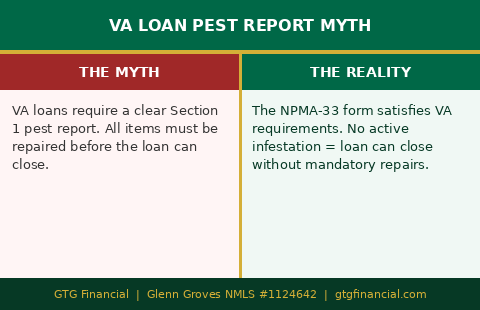

The myth goes like this: VA loans require a clear Section 1 pest report before a transaction can close. If there is dry rot, damage, or anything flagged in the Section 1 of a wood destroying pest inspection, the seller has to fix it. If they will not fix it, the deal is dead.

Realtors who believe this will steer their veteran clients away from older properties or fixer-adjacent homes before an offer is ever written. They are trying to protect their buyer from a deal that falls apart. The problem is that this version of the rule is not accurate, and following it costs veterans access to properties they could absolutely buy.

What the VA Actually Requires

The VA has a set of minimum property requirements that every home must meet for the loan to close. These requirements exist to protect the veteran buyer, not to create obstacles. The pest inspection requirement is part of those standards, but the standard is more flexible than most people assume.

In California, a VA transaction requires either a clear Section 1 pest report or something called the NPMA-33 form. The NPMA-33 is a Wood Destroying Pest Inspection Notice that gets signed off by the pest inspector who performed the original inspection. It documents what was found and certifies the condition of the property.

Here is the key: as long as there is no active infestation in the property, the NPMA-33 satisfies the VA requirement. The Section 1 items do not all have to be cleared. The seller does not have to fix everything on the report. The deal can move forward.

How the NPMA-33 Works in Practice

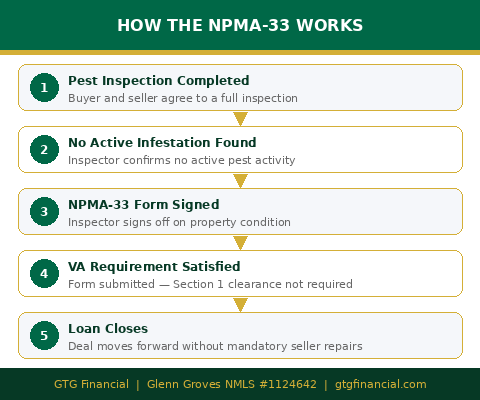

You still want a full pest inspection done. That does not change. The buyer should always know what they are getting into, and the inspection report gives them that picture. What changes with the NPMA-33 is what has to happen before closing.

Instead of requiring the seller to remediate every Section 1 item, the pest inspector signs the NPMA-33 acknowledging the condition of the property and confirming there is no active infestation. That document, submitted to the lender, satisfies the VA’s minimum property requirement. The loan can close with Section 1 items still present on the report.

This opens up a completely different set of negotiating options. The buyer and seller can negotiate concessions. The buyer can accept the property as-is with full knowledge of what the report found. The seller does not have to spend money on repairs as a condition of the sale. For older homes in particular, this is a meaningful shift in how the transaction can be structured.

In a market where a lot of housing is approaching sixty years old, the difference between needing a clear Section 1 and being able to use the NPMA-33 is the difference between a deal that works and one that never gets written.

The Appraiser Caveat

There is one scenario where this can get more complicated, and it is worth understanding before you rely on the NPMA-33 in a transaction.

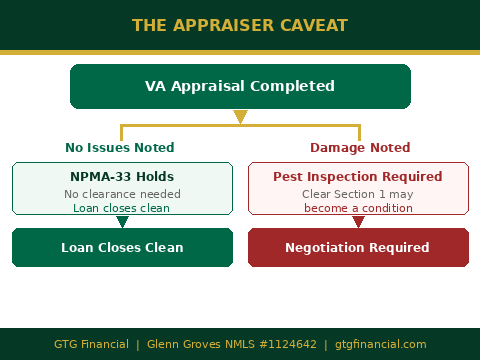

If the VA appraiser independently calls out a condition on the property during the appraisal, that changes things. When a lender receives an appraisal that notes dry rot, moisture damage, or pest-related issues, they are now aware of those conditions. At that point the lender will typically require a pest inspection, and depending on what that inspection finds, a clear Section 1 may become a condition of the loan.

The NPMA-33 works best when the pest report findings are not visible or obvious enough to catch the appraiser’s attention. In cases where there is significant visible damage, the appraiser notation can pull the pest clearance requirement back into the transaction. A lender who knows VA well will see this coming and can help you navigate it before it becomes a problem.

What Realtors in Sonoma County Need to Know

This is where I want to speak directly to real estate agents working with veteran buyers in the North Bay.

If you are advising a veteran client away from a property because of pest report concerns, you owe it to that buyer to make sure you fully understand what the VA actually requires before you give that advice. Veterans have earned a significant benefit. The VA loan is one of the most powerful mortgage tools available, and a veteran buyer with a strong profile can close on a property that other buyers would walk away from.

Steering someone away from a home they could buy because of a misunderstanding about pest inspection requirements is a disservice to your client. That buyer may end up settling for a different property, paying more, or staying on the sidelines longer than they needed to, all because of a rule that was not accurately understood.

The NPMA-33 is not a loophole. It is part of the VA guidelines. Knowing it exists and knowing when it applies is part of serving veteran buyers well. If you have questions about how it works in a specific scenario, that is exactly the kind of conversation a VA-experienced lender should be having with you before the offer goes in, not after.

The Bigger Picture for VA Buyers in the North Bay

Sonoma County has a housing stock that skews older. Properties built in the 1960s and 1970s are not unusual in Santa Rosa, Petaluma, Rohnert Park, and throughout the North Bay. Those homes often have deferred maintenance and pest report findings that would be flagged in a Section 1 inspection. Under a strict reading of VA requirements, those properties would be off the table.

Under a correct reading of VA requirements, many of those same properties are perfectly viable for a veteran buyer working with a lender who knows the program. The NPMA-33 is one piece of that. There are other VA guidelines, inspection standards, and minimum property requirements that experienced VA lenders navigate regularly, and that less experienced lenders treat as automatic deal killers.

The VA loan has a reputation in some real estate circles for being difficult. In my experience, most of that reputation comes from bad experiences with lenders who did not know what they were doing with the program. Done correctly, VA loans close cleanly, veteran buyers are protected, and sellers and realtors do not face any more complexity than they would with a conventional transaction.

If you are a veteran buyer in Santa Rosa or anywhere in the North Bay, or a realtor working with veteran clients, and you want to understand what a specific property situation actually looks like under VA guidelines, reach out. That is the kind of conversation I am here for.

Glenn Groves

Mortgage Broker | GTG Financial | Santa Rosa, CA

NMLS #1124642 | gtgfi.com

GTG Financial, Inc. NMLS #1595076 | CA DRE #02029711. Equal Housing Opportunity. This content is for educational purposes only. Not a commitment to lend. Subject to credit approval and underwriting. Rates and terms subject to change without notice. Individual results vary based on credit profile, property type, loan amount, and other factors. nmls consumeraccess.org

Related Posts