July 2026 | GTG Financial | Santa Rosa, CA First-Time Buyer Down Payment: How Little…

First-Time Buyer, $780K Home, 3% Down: What the AMI Math Actually Showed Us

Deal Deep Dive | April 2026 | GTG Financial | Santa Rosa, CA

TL;DR — What’s in This Post

- Real deal: $780K home, 3% down, Santa Rosa first-time buyers

- Why conventional beat FHA for this specific profile

- What the AMI benefit is and why these buyers almost used it

- The math that changed everything: $2,100 credit vs. $175/mo PMI

- Why removing one borrower from the loan hurt more than it helped

- The 12-month break-even that made the decision simple

First-time homebuyers come in with a list. Programs they read about online, benefits they heard about from a friend, strategies they found on Reddit. Most of the time that research is a starting point, not a plan. Part of my job is figuring out which of those ideas actually make sense for the specific loan in front of us and which ones look good on paper until you run the numbers.

This deal is a good example of that.

The Deal at a Glance

Example for educational purposes only. Not a commitment to lend. Subject to credit approval and underwriting. Rates and terms subject to change without notice. Individual rates vary based on credit profile, property type, occupancy, loan amount, and other factors.

| Detail | Number |

|---|---|

| Purchase Price | $780,000 |

| Loan Type | Conventional 30-year fixed, 3% down |

| Down Payment | $23,400 |

| Interest Rate | 5.99% |

| APR | 6.320% |

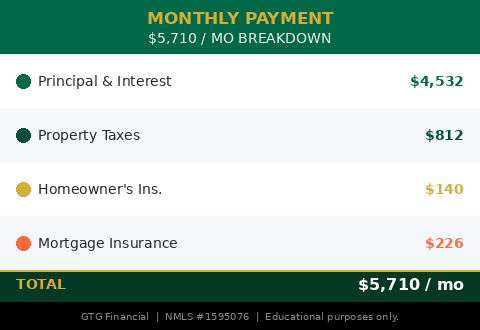

| Total Monthly Payment | $5,710 |

| FICO Score | 769 |

| Location | Santa Rosa, CA |

The total monthly payment of $5,710 breaks down across four buckets: principal and interest on the loan, homeowner’s insurance at $140 a month, property taxes at $812 a month based on the purchase price, and mortgage insurance at $226 a month. Property taxes are tied to the purchase price regardless of how much you put down, so a bigger down payment does not change that number.

Why Conventional Beat FHA for These Buyers

When we have first-time buyers with a smaller down payment, we look at three main options: conventional at 3% down, conventional at 5% down, and FHA at 3.5% down. Each one has a different cost structure and the right choice depends on the specific profile in front of us.

For this couple, a 769 FICO score and a strong income picture made conventional the clear winner. FHA carries mortgage insurance for the life of the loan in most cases, which adds up significantly over time. With a 769 score, these buyers were in solid shape to get favorable conventional pricing. The 3% down conventional structure gave them the lowest effective cost over time and kept more cash in their pocket at closing.

FHA is a strong tool for the right borrower. It is not automatically the best choice for first-time buyers, and it is not limited to first-time buyers either. The structure has to match the profile. In this case, conventional won.

The AMI Benefit: What It Is and Why These Buyers Wanted It

These borrowers came in knowing about the area median income benefit. They had done their homework, which I respect. The AMI is a threshold set by Fannie Mae, and you can look up the number for any zip code on the Fannie Mae website. If your household income falls at or below the AMI for your area, certain loan level price adjustments get waived.

Loan level price adjustments, or LLPAs, are pricing hits that get added to your interest rate based on factors like your FICO score and how much you are putting down. At 3% down, even with a 769 score, there are some LLPAs built into the rate. Waiving those can mean real money.

This couple had a combined income well over $200,000. They were nowhere near the AMI threshold together. But they saw that if they could get under it, they stood to benefit. The question was whether getting there was actually worth it.

The Math That Changed the Decision

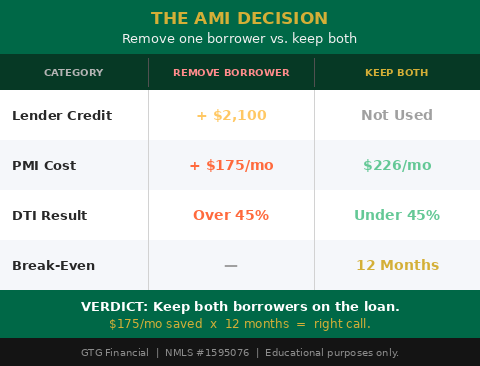

To fall under the AMI and waive those loan level price adjustments, we would have needed to remove one borrower from the loan entirely. With only one income on the application, their household income would drop below the threshold and the LLPAs would be waived.

That move would have picked up $2,100 in lender credit. On the surface that sounds like a straightforward win.

Here is where it got complicated.

By removing one borrower, we pushed the remaining borrower’s debt to income ratio over 45%. Mortgage insurance pricing is sensitive to DTI. When DTI crosses that 45% line, the PMI cost goes up. In this case it went up by $175 per month.

$2,100 in lender credit sounds great. $175 more per month for as long as you carry mortgage insurance is a different conversation entirely.

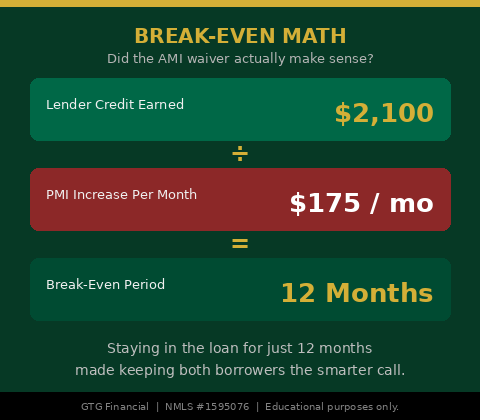

We ran the break-even math. If these buyers kept both borrowers on the loan and did not use the AMI waiver, how long before the lower PMI cost paid off compared to what they gave up in lender credit?

Twelve months.

They needed to stay in that loan for twelve months for the decision to take the cheaper mortgage insurance to make sense. Given that most buyers in Sonoma County either refinance or move within a few years, twelve months is a reasonable hold period. The math was clear.

We kept both borrowers on. Did not remove anyone from the loan. Did not take the AMI waiver.

What First-Time Buyers in Sonoma County Actually Need to Know

This deal illustrates something that comes up regularly with first-time buyers. There is real information out there about programs and benefits available to you, and you should absolutely know about them. But every program, benefit, and strategy has conditions attached to it. The question is never just whether you qualify for something. The question is whether using it actually helps you given your full picture.

A few things worth knowing if you are buying for the first time in the Santa Rosa area or anywhere in the North Bay:

The AMI benefit is real and worth exploring. For buyers whose household income genuinely falls under the area median income threshold, the LLPA waiver can meaningfully reduce your rate. Look up the AMI for your target zip code on the Fannie Mae site and see where you stand before writing it off.

Removing a borrower from a loan is a strategy that has legitimate uses. In some situations it makes sense to leave one spouse off the loan to preserve their credit capacity or avoid an income or debt issue. But it is not a free move. Every time you take someone off the application, you change the debt to income calculation for the person who stays on. That change has a cost, and that cost has to be weighed.

Break-even math is one of the most useful tools in a mortgage conversation. Whenever someone presents you with a trade-off, whether it is buying points to lower your rate, paying a larger down payment to eliminate PMI sooner, or using a program that comes with conditions, ask for the break-even. How long until this decision pays off? If the answer is longer than you plan to stay in the loan, the decision probably does not make sense.

The Bigger Picture for First-Time Buyers Right Now

A $780,000 home with $23,400 down is not the picture most first-time buyers have in their heads when they think about what it takes to buy here. Many assume they need 20% down, which on this property would be $156,000. The gap between what people think is required and what is actually required is one of the main reasons qualified buyers stay on the sidelines longer than they need to.

The North Bay is an expensive market. Sonoma County home prices put most buyers into high-balance conventional territory, and the monthly payment on a median-priced home is significant. But the conversation about whether you can buy here is different from the conversation about whether you should wait. Those are two separate questions and they deserve separate answers.

If you are a first-time buyer in Santa Rosa, Petaluma, Windsor, Rohnert Park, or anywhere in the North Bay and you want to understand what your actual picture looks like, the place to start is a real pre-approval conversation, not a mortgage calculator. The calculator tells you a payment. The conversation tells you whether the structure makes sense for where you are headed.

Reach out if you want to run the numbers on your specific situation. That is what I am here for.

Glenn Groves

Mortgage Broker | GTG Financial | Santa Rosa, CA

NMLS #1124642 | gtgfinancial.com

GTG Financial, Inc. NMLS #1595076 | CA DRE #02029711. Equal Housing Opportunity. Example for educational purposes only. Not a commitment to lend. Subject to credit approval and underwriting. Rates and terms subject to change without notice. Individual rates vary based on credit profile, property type, occupancy, loan amount, and other factors. nmls consumeraccess.org

Related Posts