Introduction As the end of July approaches, many families are preparing for the back-to-school season.…

What Mortgage Insurance Really Is (And How to Get Rid of It Faster)

May 2026 | GTG Financial | Santa Rosa, CA

TL;DR: What’s in This Post

- What mortgage insurance is and who it actually protects

- The two factors that drive MI pricing on a conventional loan

- When MI gets removed and what the lender is actually tracking

- How to challenge the value and potentially drop MI without refinancing

On a conventional loan with less than 20% down, nine times out of ten you are going to have mortgage insurance. Most people know that. Fewer people understand what it actually is, what makes it more or less expensive, and how to get rid of it faster than the lender’s default timeline would suggest.

That is what this post covers. No jargon, just the mechanics.

What Mortgage Insurance Actually Is

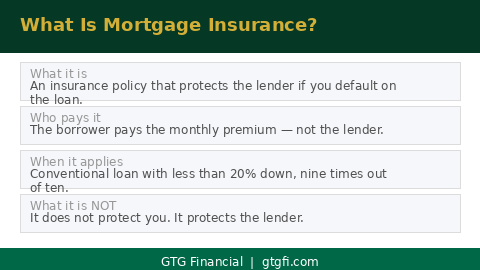

Mortgage insurance is a policy that protects the lender if you default on the loan. It does not protect you. If you stop making payments and the lender has to foreclose, the MI policy reimburses the lender for their loss. You are the one paying the premium every month.

This is the part that trips a lot of people up. They assume MI is there to help them in some way, like homeowners insurance or life insurance. It is not. It is the lender managing their risk on a loan where they have less equity as a cushion. The borrower pays for that protection on the lender’s behalf.

The most common scenario where MI applies is a conventional loan with less than 20% down. That threshold is not arbitrary. At 20% equity, the lender has enough of a cushion that statistically, the risk of loss in a default scenario drops significantly. Below that, lenders generally require MI to compensate.

What Drives the Price

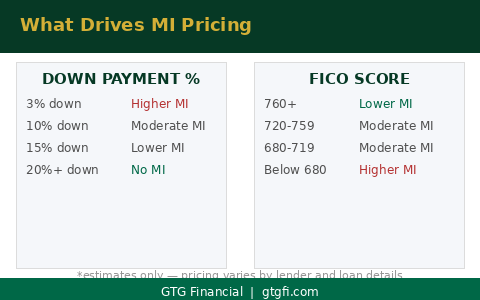

Two things move MI pricing more than anything else: how much you are putting down and what your FICO score is. Those two factors can work against each other or in your favor, depending on the combination.

A lower down payment means more risk for the lender, which means higher MI. A lower FICO score means the same thing. But you can offset one with the other. A borrower with a 680 FICO putting 15% down is not going to have expensive MI. The higher down payment compensates for the mid-range credit score. On the flip side, a borrower with an 800 FICO putting 3% down is also going to have reasonable MI because the credit profile offsets the thin down payment.

Where MI gets expensive is when both factors are working against you at the same time: low down payment and a lower credit score. In that situation you will qualify for the loan, but the MI cost is real and it shows up in the monthly payment. The scenarios above are illustrative estimates only. Actual MI rates vary based on the lender, the loan amount, and the full credit profile.

When MI Gets Removed

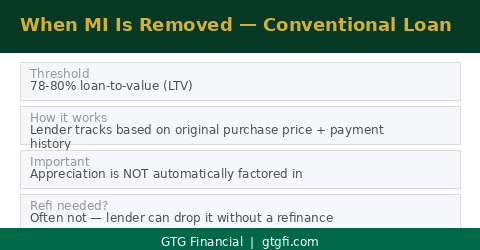

On a conventional loan, MI is not permanent. Once your loan balance drops to somewhere between 78 and 80% of the original purchase price, the lender removes it. You do not have to refinance. The lender tracks this based on your payment history and the original purchase price, and at that threshold, MI comes off.

The key word in that last sentence is original. The lender is looking at what you paid for the house, not what it is worth today. If your home has appreciated since you bought it, that appreciation is not automatically factored in. The lender’s calculation is based on the original price plus your natural paydown over time. That distinction matters, and it is where the next section comes in.

The other thing worth knowing is that you do not need to do anything complicated to trigger this. Once the math gets there based on the lender’s amortization schedule, the MI should come off. Some lenders require you to request it in writing at 80% rather than dropping it automatically at 78%. It is worth confirming with your servicer how they handle it so it does not sit on your payment longer than it needs to.

The Move Most People Do Not Know About

If your home has appreciated since you bought it, you may be able to use that appreciation to get MI removed earlier than the standard amortization schedule would get you there. The mechanism is a value challenge, and it does not require a refinance.

Here is how it works. After you have been in the loan for at least two years, you can contact your loan officer and ask whether you are eligible to challenge the value. The lender will typically order either a full appraisal, which runs around $500, or an automated valuation model. If the new value puts your loan balance at 78 to 80% of that updated number, the lender can remove MI based on the current value rather than the original purchase price.

We have gone through this process with a number of clients, particularly those who bought in the last few years when values moved meaningfully. In several of those cases we were able to get MI removed without the client having to refinance, which meant they kept the rate they had. For anyone sitting on a rate from 2020 or 2021, that matters a lot.

The main requirement is the two-year seasoning. Some lenders may have additional criteria, so this is a conversation to have with your loan officer rather than something you can trigger on your own. Results vary based on where values have gone in your specific market and how the numbers land against your current balance. But it is absolutely worth asking about, and a lot of people never do.

What to Take Away

Mortgage insurance is a real cost that shows up in your monthly payment, but it is not a permanent one. Understanding what drives the price helps you make smarter decisions before you close. And knowing that you can challenge the value after a couple of years gives you a path to getting rid of it sooner than the lender’s default timeline, without having to refinance to do it.

If you have an existing loan with MI and you have been in the property for two or more years, it is worth a conversation. If you are shopping for a home now and trying to figure out what MI will cost on your specific profile, that is a 10-minute call. Either way, the information is free.

You are the one paying for MI every month. You should also be the one deciding when it comes off.

Reach out if you want to talk through your situation. We are in Sonoma County and the North Bay and work with buyers and homeowners throughout California.

Glenn Groves

Mortgage Broker | GTG Financial | Santa Rosa, CA

NMLS #1124642 | gtgfi.com

GTG Financial, Inc. NMLS #1595076 | CA DRE #02029711. Equal Housing Opportunity. Not a commitment to lend. Subject to credit approval and underwriting. MI pricing examples shown are estimates only and do not represent a quote or guarantee. Actual MI rates vary based on credit profile, loan amount, down payment, lender, and other factors. Individual loan terms and pricing vary. nmls consumeraccess.org

Related Posts