July 2026 | GTG Financial | Santa Rosa, CA First-Time Buyer Down Payment: How Little…

Deal Deep Dive: Conventional Vs FHA + Rate Buydown

May 2026 | GTG Financial | Santa Rosa, CA

TL;DR: What’s in This Post

- How a 2-1 temporary rate buydown works and what it actually costs

- How the seller funded the entire buydown through a concession

- Why conventional beat FHA for this 740 FICO first-time buyer

- The full monthly payment breakdown on a $700,000 purchase at 3% down

- The lender curveball we hit on income and how we got around it

This deal funded in May 2025, so the rates you will see here reflect that market. Rates have moved since then. What has not changed is the strategy, and that is what I want to walk you through here.

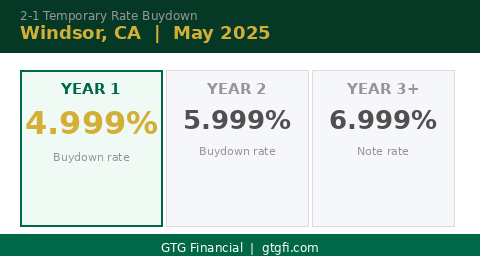

A first-time buyer in Windsor, California was purchasing a $700,000 home with 3% down. The note rate was 6.999 on a 30-year fixed. That is a real number, and for a lot of buyers it is a number that makes the payment feel heavy. But when we finished structuring this deal, year one felt like 4.999%. Here is exactly how that happened.

The Deal at a Glance

Purchase price was $700,000 in Windsor, California. The buyer put 3% down, which came to $21,000. They went conventional, not FHA, and their FICO score was 740. This was their first home.

When buyers are coming in with a minimum down payment, we typically look at three options side by side: 3% conventional, 3.5% FHA, and 5% conventional. From there we work backwards from what the buyer actually wants to accomplish, what their credit looks like, and what the monthly payment needs to feel like. In this case, the direction was clear pretty quickly, and I will get into why conventional was the right call in a moment.

The note rate was 6.999%, with an APR of 7.450%. Those numbers are a snapshot of May 2025 and I want to be upfront about that. The structure of the deal is what matters here, not the specific rate, because the same approach applies in any rate environment where seller concessions are available.

What a 2-1 Temporary Rate Buydown Does

A 2-1 temporary rate buydown does not change the note rate on the loan. The note rate stays at 6.999% on paper. What it does is reduce what the borrower actually pays in the early months of the loan, with the difference made up by a lump sum deposited at closing.

In this case, the buydown worked like this: year one, the buyer paid as if the rate were 4.999%. Year two, as if it were 5.999%. Starting with payment 25, they pay the full 6.999% for the remainder of the loan. The funds to cover that two-year discount have to come from somewhere, and that is where the seller concession came in.

The reason this structure makes sense for a lot of buyers right now is that income tends to grow over time. A buyer who is stretching a little in year one has more runway by year three. The payment does not jump on them suddenly. It steps up gradually, which is a much easier adjustment than absorbing the full rate from day one.

How the Seller Paid for It

The buyer did not pay for this buydown out of pocket. The seller did, through a concession negotiated as part of the purchase contract. The realtor on this deal worked hard going back and forth and was able to secure enough seller credit to cover the full cost of the 2-1 buydown, which came to approximately $16,000.

This is one of the most underused tools in a buyer’s negotiation kit right now. A seller concession toward a rate buydown is not the same as a price reduction. A price reduction lowers the purchase price. A concession toward a buydown directly reduces what the buyer pays every month in the near term, which is usually where the pressure is. For a buyer focused on cash flow in year one, that is often more valuable dollar for dollar than knocking something off the purchase price.

The key is knowing what to ask for and how to frame it. A good realtor and a good mortgage broker working together on the same page is what makes this work. Here, it came together cleanly.

Why Conventional Beat FHA for This Buyer

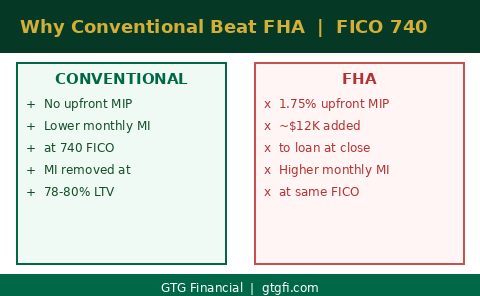

At 3% down, you are always going to have mortgage insurance on a conventional loan. But with a 740 FICO score, the cost of that mortgage insurance is meaningfully lower than it would be on an FHA loan. And unlike FHA, conventional does not charge an upfront mortgage insurance premium, which is a lump sum that gets added directly to your loan balance at closing.

On FHA, that upfront premium is 1.75% of the loan amount. On a $679,000 loan, that is nearly $12,000 added to what you owe before you make a single payment. Conventional eliminates that entirely for a borrower with strong enough credit.

The monthly MI on this loan was $243. That is the actual cost of the insurance in the payment, and it does not last forever. On a conventional loan, mortgage insurance can be removed once you have built enough equity in the property, typically when your loan-to-value reaches around 78 to 80%. We monitor that for our clients post-close so we can flag when it makes sense to either refinance or challenge the lender to remove it based on current value.

What the Monthly Payment Looked Like

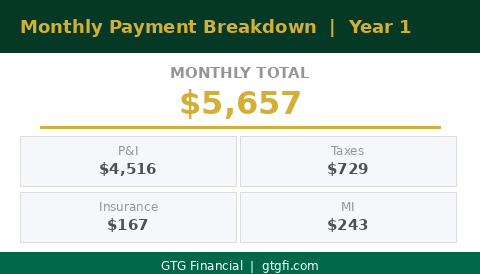

The total monthly payment on this deal was $5,657. That number is made up of four pieces. Principal and interest came to $4,516. Property taxes were $729 per month. Homeowners insurance was $167. And mortgage insurance was $243.

It is worth noting that the P&I figure reflects the year one buydown payment, not the full note rate payment. The actual P&I at 6.999% is higher. The buydown funds cover the difference each month in years one and two, so the out-of-pocket payment is $5,657, but the lender is receiving the full payment equivalent throughout.

For a first-time buyer stepping into a $700,000 home with $21,000 down, knowing exactly what the monthly obligation looks like is critical. There are no surprises in this number. Taxes and insurance are estimates that get reviewed at each annual escrow analysis, but the structure is transparent from day one.

The Lender Curveball We Had to Navigate

Nothing about the credit profile or the purchase structure was complicated. The curveball came from the lender we initially went to, and it had to do with how they were looking at income.

This buyer had variable income with overtime, and they had been at their current employer for about ten months at the time we were underwriting. The first lender looked at that and decided they could not use any of the variable income or overtime because the borrower had not been in that position for a full 12 months. Under a strict reading of the guidelines, there is a case for that position. But it was not the only way to read it.

We moved quickly. We found another lender who took a common-sense approach and averaged the variable income over the full 12 months the borrower had actually worked, even though the employer tenure was ten months. That was enough to qualify comfortably.

This is one of the real advantages of working with a broker instead of going directly to a single lender. When one lender hits a wall on something that should not be a deal-breaker, we can pivot fast. We are not married to one set of underwriting guidelines. We have access to a wide range of lenders and we know which ones handle situations like this well. For this buyer, that pivot saved the deal.

What to Take Away From This Deal

A 2-1 buydown is not a trick. It is a real tool that lowers your payment in the years when cash flow is tightest. When it is funded by a seller concession, it costs the buyer nothing extra at closing. And when your credit profile qualifies you for conventional over FHA, you eliminate one of the more expensive upfront costs in the FHA program.

Put those three things together and you have a buyer who got into a $700,000 home at 3% down, paid $5,657 a month in year one instead of a higher fully-indexed payment, and avoided nearly $12,000 in upfront MIP that would have piled onto their loan balance. That is a meaningful difference in the early years of homeownership.

The seller funded the buydown. The buyer got into the home. Year one felt like 4.999%.

If you are in Sonoma County or the North Bay and want to talk through whether a structure like this makes sense for your situation, reach out. That conversation is free and it usually clarifies a lot.

Glenn Groves

Mortgage Broker | GTG Financial | Santa Rosa, CA

NMLS #1124642 | gtgfi.com

GTG Financial, Inc. NMLS #1595076 | CA DRE #02029711. Equal Housing Opportunity. Not a commitment to lend. Subject to credit approval and underwriting. Rates and terms subject to change without notice. Rates shown reflect May 2025 market conditions and are not current. Individual rates vary based on credit profile, property type, occupancy, loan amount, and other factors. nmls consumeraccess.org

Related Posts