July 2026 | GTG Financial | Santa Rosa, CA First-Time Buyer Down Payment: How Little…

Rates Dropped This Week. Two Events Could Take It All Back.

Issue 153 | April 21, 2026 | GTG Financial | Santa Rosa, CA

TL;DR — What’s in This Post

- Rates dropped an eighth point — here’s the two reasons why

- Why your 30-year rate is ~0.26% higher than it mathematically should be

- Two back-to-back events this week that could reverse last week’s gains

- What to watch Tuesday, Wednesday, and Thursday

- What this means if you’re buying in Sonoma County right now

- Lock or wait? The honest answer

Rates dropped an eighth of a point this week. That is the headline, and I do not want to dismiss it. On a $580,000 loan in Sonoma County, an eighth point matters in real dollars every month.

But do not get comfortable, and please do not pass this to your buyers as a trend. By the time you finish reading this, you will understand why last week’s movement could disappear by Thursday, why rates are sitting higher than the math says they should be, and what all of it means if you are buying or helping someone buy in the North Bay right now.

What Actually Moved Rates This Week

Two things came in soft and the bond market reacted to both.

The first was wholesale inflation. Here is the connection worth remembering. Inflation tracks how fast prices rise. When prices rise faster than expected, the people who hold bonds get nervous because a fixed return is worth less when everything around it costs more. They sell, yields go up, and mortgage rates climb with them. When inflation comes in cooler than expected, like the wholesale report did last week, the opposite happens. Bond investors jumped in to buy. More demand pushed prices up, yields dropped, and mortgage rates followed them lower.

The second was housing data. Existing home sales fell 3.6% in March, and builder confidence dropped to a seven-month low in April. That is bad news for the market on the surface. But here is the counterintuitive part: when housing slows, the broader economy tends to slow with it. A slower economy puts less pressure on prices. Less inflation pressure gives the bond market breathing room. Bad housing news today can translate to a small rate improvement tomorrow.

Both signals pointed the same direction last week. The bond market noticed.

Where Rates Stand Right Now

Rates as of April 21, 2026. All scenarios assume 30-year fixed, purchase or rate/term refinance, 780 FICO, 20% down. No origination points. Provided for consumer education only.

| Product | Rate / APR | Weekly Change | Notes |

|---|---|---|---|

| Conv. 30-yr | 6.250% / 6.285% | ↓ -0.125% | |

| Conv. HB 30-yr | 6.375% / 6.404% | ↓ -0.125% | |

| Jumbo 30-yr | 6.375% / 6.402% | ↑ +0.125% | |

| FHA 3.5% DP | 5.625% / 6.584% | ↔ No change | 3.5% min. down |

| VA 0% DP | 5.625% / 5.863% | ↔ No change | Veterans, 0% down |

FHA and VA rates held flat at 5.625% this week. The movement was on conventional loans only. Worth knowing before making any decisions based on a headline.

The Part Nobody Is Talking About Locally: The Mortgage Spread

Here is the deeper story behind why rates feel stuck even when inflation data looks good. Most people know mortgage rates follow the bond market. Here is the layer most people miss.

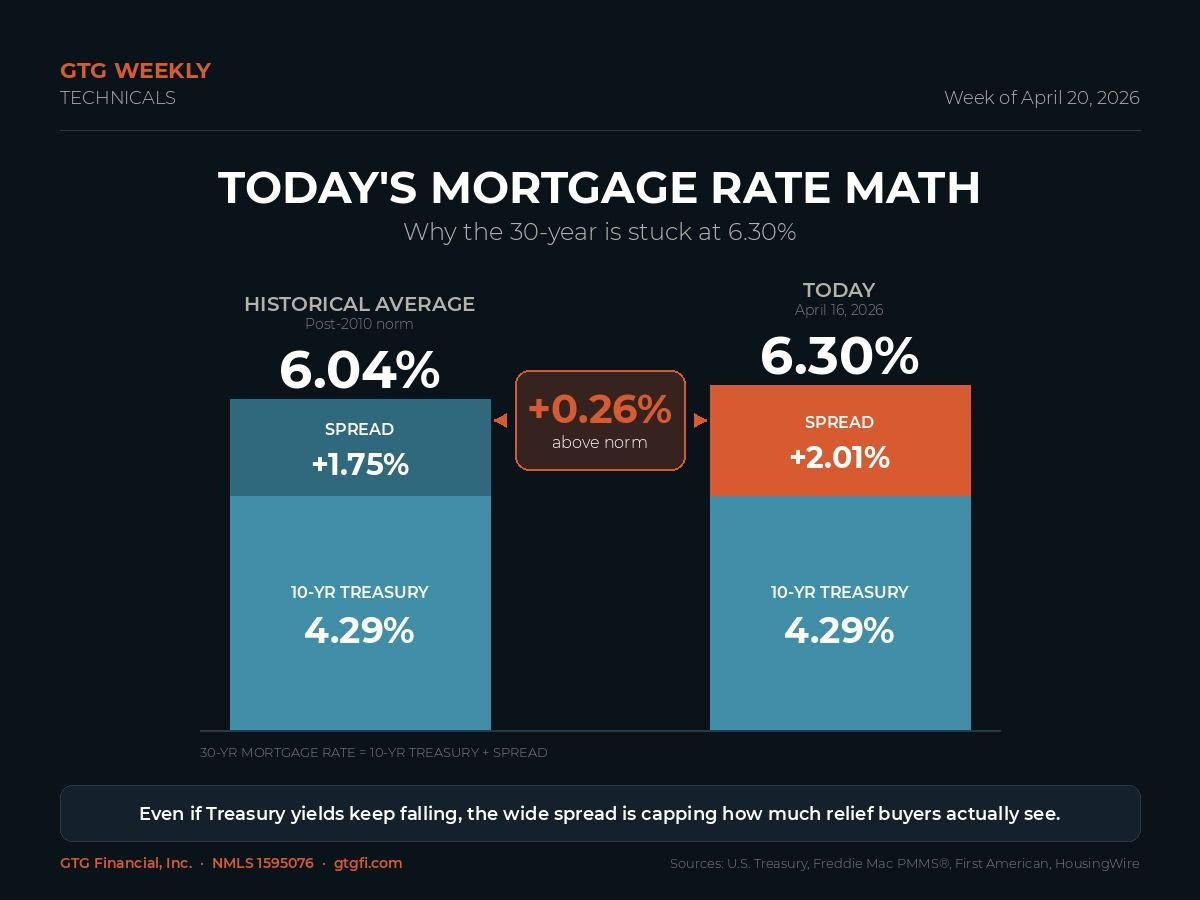

Mortgage rates do not just follow the 10-year Treasury yield. They follow the 10-year Treasury plus a gap called the mortgage spread. That spread represents the extra yield investors demand to hold mortgage bonds instead of safer government bonds. Since the end of the Great Recession, that spread has averaged around 1.75 percentage points.

Here is where the math gets telling.

The 10-year Treasury finished last week near 4.29%, sitting at a three-week low on the back of softer inflation data. Add the historical average spread of 1.75% and you would expect a 30-year mortgage to land around 6.04%. The actual 30-year rate came in at 6.30%. That puts the current spread at roughly 2.01%, about 26 basis points above the historical norm.

Think of the spread as a toll between where Treasury yields are and what your buyer actually pays. Right now that toll is running unusually high. Three reasons for it:

The Federal Reserve is still slowly selling off its mortgage bond holdings every month. Less Fed demand means investors require higher yields to compensate.

Foreign buyers of US mortgage bonds have pulled back. Tariff and trade uncertainty has made overseas investors more cautious, and they used to be a reliable source of demand.

Banks, the other major buyer category, have been largely on the sidelines since 2022 when the rate environment made mortgage bonds less attractive to hold.

The practical takeaway for Sonoma County buyers: even if Treasury yields drop another quarter point, you will likely only see a portion of that savings show up in your mortgage rate. Until the spread narrows back toward historical norms, there is a quiet ceiling on how much relief buyers will see even when broader bond market news looks good. This is the real story of 2026 rates, and it is why “wait for rates to drop” keeps disappointing the buyers who try it.

Two Events This Week That Could Reverse Everything

Kevin Warsh is in front of the Senate today for his confirmation hearing as the potential next Federal Reserve Chair. Warsh has publicly said he believes the Fed has room to cut rates because technology is helping bring inflation down. If the Senate moves forward with him, the market will start pricing in future rate cuts. If the hearing sends mixed signals or gets blocked, markets get skittish. Either outcome moves rates. Not every week comes with a headline like this.

Back to back, the US-Iran ceasefire expires Wednesday. Iran already closed the Strait of Hormuz over the weekend and oil prices moved higher this morning in response. Oil matters for mortgage rates because it touches everything: shipping, groceries, construction materials, transportation. When oil spikes, inflation expectations spike. When inflation expectations spike, mortgage rates follow. If the ceasefire falls apart and oil moves sharply, last week’s gains could disappear in a single afternoon.

Two big events on back-to-back days, both capable of moving rates in either direction. Volatility is the base case this week, not the exception.

What to Watch the Rest of This Week

Tuesday: Retail Sales and Pending Home Sales. Strong retail numbers mean consumers are still spending, which keeps inflation pressure on and rates elevated. Pending home sales will show whether buyers in Sonoma County and nationally are actually coming off the sidelines.

Wednesday: Mortgage Applications and the 20-year Treasury Auction. A weak auction is a quiet signal that pushes rates up quickly and often does not make the news until after rates have already moved.

Thursday: Jobless Claims. Continuing claims have been climbing. If that trend holds, it signals a softening labor market, which typically gives rates room to ease.

What This Means for North Bay Buyers

The answer is not the same for everyone. Here is how to think about it based on where you are in the process.

Buying in Santa Rosa and Sonoma County Right Now

If you are buying in Santa Rosa, Petaluma, Windsor, or anywhere in the North Bay, the honest read is to stay ready without being reactive. The median home price in Sonoma County sits around $710,000. Even a small rate movement has a meaningful impact on your monthly payment at that price point. But chasing rate movement week to week is not a strategy. The goal is to be financially prepared and pre-approved so you can move when the right property and the right conditions line up.

FHA Financing: Not Just for One Type of Buyer

FHA loans held at 5.625% this week with a minimum 3.5% down payment. A common misconception is that FHA financing is only for first-time buyers. It is not. FHA is available to qualified buyers regardless of whether you have owned a home before. If you have a solid credit profile and are looking for a lower down payment option in this market, FHA is worth a conversation no matter where you are in your homebuying journey.

Veterans Using a VA Loan in Sonoma County

VA financing held at 5.625% this week with zero down payment required and no private mortgage insurance. For veterans buying anywhere in the North Bay, this is one of the most favorable loan structures available in this market, and it did not move while conventional rates shifted around it.

If you have not gotten your pre-approval yet, now is a good time to start that process. Pre-approval does not lock a rate, but it puts you in a position to move quickly when inventory opens up and rate conditions are favorable. Waiting until you find the property is usually the more expensive approach.

Buyers Already in Contract

This week is worth paying close attention to. If the Warsh hearing and the ceasefire situation both land without major volatility, rates could hold or inch lower. If either one rattles the bond market, rate lock timing becomes a real conversation. That is a discussion worth having with your lender before something happens, not after. Ask specifically about your lock expiration date and what your options are if rates move in either direction this week.

Lock or Wait?

Rates got a small gift this week. Do not pass that gift to your buyers as a trend.

With the Fed Chair confirmation hearing and the Iran ceasefire deadline both landing in the same week, this is not a normal news cycle. If your buyer is qualified and ready, today’s pricing is something to lock, not something to sit on. Waiting to see what happens next week is not a strategy. It is a coin flip.

If you have questions about where rates stand right now or what any of this means for your specific situation in Santa Rosa or the surrounding Sonoma County area, reach out. This is what I spend my time on, and I am happy to walk through the numbers with you.

Glenn Groves

Mortgage Broker | GTG Financial | Santa Rosa, CA

NMLS #1595076 | gtgfinancial.com

GTG Financial, Inc. NMLS 1595076. Equal housing opportunity. Rate data provided for consumer education only and does not serve as a binding offer to extend lending. Subject to income, asset, and credit profile qualification. nmls consumeraccess.org

Related Posts