Introduction As the end of July approaches, many families are preparing for the back-to-school season.…

Is Your Loan Jumbo?

May 2026 | GTG Financial | Santa Rosa, CA

TL;DR: What’s in This Post

- The three loan tiers in Sonoma County and exactly where each limit sits

- Why jumbo financing is the Wild West — and what that means for your rate and approval

- The practical math on a $1 million purchase and how to stay out of jumbo

- When flirting with the jumbo line, why your down payment is the key variable

In Sonoma County, you do not have to be buying a mansion to end up in jumbo territory. A median-priced home here puts a lot of buyers right at the line between conforming, high balance, and jumbo — and most of them do not realize it until they are already in the process.

Here is how to think about it before you get there.

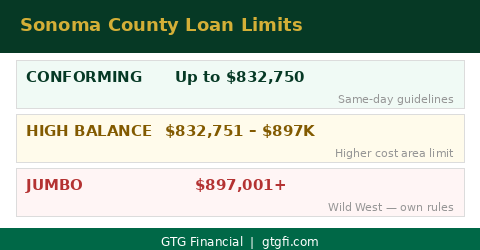

The Three Tiers: Where the Lines Are

Sonoma County is considered a high-cost area, which means we get a loan limit above the national conforming baseline. Here is where each tier sits right now.

The conforming limit is $832,750. If your loan amount is at or below that, you are in standard conforming territory — Fannie Mae and Freddie Mac guidelines, competitive pricing, and the full range of down payment options.

Between $832,751 and $897,000, you are in what is called a high balance loan. The guidelines are essentially the same as conforming — you can still put 5% down, same documentation requirements, same general process. The rate is a little more expensive because of where it sits, but it is not a different world. Marin County, for reference, has a high balance limit that goes past $1.2 million because it is an even higher-cost area.

Once your loan amount crosses $897,000, you are in jumbo financing. And that is where things change.

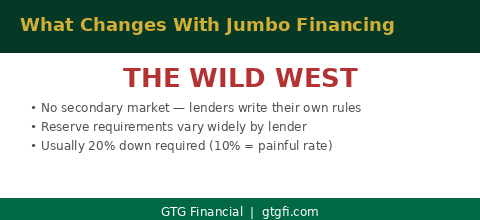

What Jumbo Actually Means

The simplest way to understand jumbo is this: with a conforming or high balance loan, every lender is underwriting to the same Fannie Mae and Freddie Mac guidelines. They can sell that loan on the secondary market. There is a standardized playbook.

There is no secondary market for jumbo. Each lender holds that loan in their own portfolio or securitizes it on their own terms. That means each lender writes their own rules. One might require 24 months of reserves. Another might have a minimum FICO score that is different from the next one. A rate that looks great on a website might come with qualification requirements that do not fit your situation at all.

It also means you need to shop more carefully. Two lenders quoting jumbo rates on the same day can look very different once you get into the details. This is one of the places where working with a broker who has access to multiple jumbo lenders makes a real difference, rather than going to a single institution and taking what they offer.

The $1 Million House Math

One of the most practical things to understand about the jumbo line is that your down payment is what determines which side of it you land on. The loan limit is based on your loan amount, not the purchase price.

Here is a concrete example. If you are buying a $1 million home and you want to stay out of jumbo, you need your loan to come in at or below $897,000. That means putting $103,000 down — just over 10%. At that point, you are a high balance loan. Plain Jane. Same guidelines as conforming, just a slightly higher rate than if you were below $832,750.

Jumbo usually requires 20% down. You can sometimes get away with 10%, but the rate on a 10% down jumbo loan is going to be noticeably worse. There is no mortgage insurance on jumbo loans, so the lender is absorbing the risk of the low down payment directly into the interest rate. It shows up in the number.

Where this gets interesting is when you are looking at purchase prices in the $1.1 to $1.2 million range. At that point the math starts requiring real cash to stay out of jumbo territory, and we will often run multiple scenarios side by side — conventional with jumbo versus high balance with a larger down payment — to see which one actually makes sense for your situation.

What to Take Away

The most common mistake I see with buyers flirting with these numbers is not knowing the tiers exist until they are already deep into a property. By that point, the emotional attachment is there and the math has to catch up. The better play is to understand upfront where the lines are, what your loan amount would look like at different purchase prices, and whether your down payment gives you flexibility or locks you into a specific tier.

Most of the time when I sit down with a buyer in this price range, there are more options than they realized. Sometimes a slightly higher down payment keeps them out of jumbo entirely and gets them a meaningfully better rate. Sometimes the jumbo product is actually the right call because the guidelines fit their situation and the rate is competitive. The answer is almost always in the math.

Your down payment determines which bucket you land in. Know the lines before you fall in love with a house.

If you are buying in Sonoma County and want to understand where you fall and what your options look like at your price point, reach out. That conversation is free and there is no obligation.

Glenn Groves

Mortgage Broker | GTG Financial | Santa Rosa, CA

NMLS #1124642 | gtgfi.com

GTG Financial, Inc. NMLS #1595076 | CA DRE #02029711. Equal Housing Opportunity. Not a commitment to lend. Subject to credit approval and underwriting. Loan limits referenced are current as of publication and subject to annual adjustment. Individual results vary based on credit profile, loan amount, property type, and other factors. nmls consumeraccess.org

Related Posts