Understanding the Impact of Hurricane Season on Homeownership As we approach the peak of hurricane…

Rate Locks

June 2026 | GTG Financial | Santa Rosa, CA

TL;DR: What’s in This Post

- Why you cannot lock a rate before you have a property in contract

- What locking the rate sheet actually means and why it gives you more flexibility than most buyers expect

- When and how to revisit your rate before final docs are drawn

- What happens when a rate lock expires and what it costs to extend one

Most buyers spend weeks comparing rates before they make an offer. They call lenders, get quotes, watch the market. That is all useful context. But none of it locks anything. You cannot lock a rate until you have a property in contract. And the mechanics of how a rate lock actually works are different from what most people assume going in.

What a Rate Lock Actually Is

A rate lock is exactly what it sounds like. It locks your interest rate at a specific point in time for a specific period, most commonly 30 days. Once locked, the rate is frozen regardless of what the bond market does between then and your close date. You are secured at that rate for the term of the lock, assuming everything closes on time.

The key constraint: a lender will not lock a rate for you without collateral. Without a house. That means all the rate shopping you are doing before you find a property is useful for understanding the market, but nothing is locked. The lock only becomes available the moment you have a property under contract.

Custom lock periods are also possible. If you have a 21-day contract, a lender can sometimes match a 21-day lock. The shorter the lock period, the better the pricing tends to be. Every day of lock period costs the lender money on the back end, so shortening the window can translate to a real pricing advantage.

How to Use It Strategically

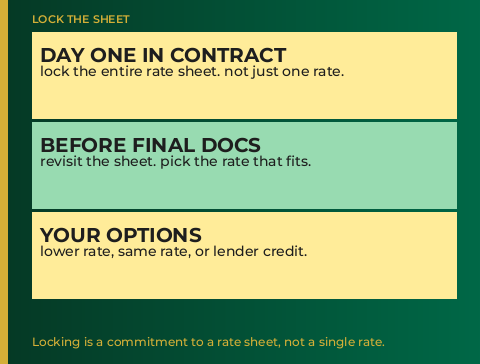

The most important thing to understand about a rate lock is that you are not locking a single rate. You are locking the entire rate sheet for that day. That distinction matters because it gives you options all the way to the finish line.

Here is how that plays out. You go in contract. You lock at whatever the par rate is that day, meaning no discount points and no lender credit. The lock holds while the deal moves forward through inspections, appraisal, and insurance review. Then, before final docs are drawn, you revisit the rate sheet you locked and make a decision based on everything you now know about the property.

Do you want to stay at that 6.5? Fine. Do you want to move to a 6.375? That is available. Or maybe now that you know you want to redo the kitchen, you move up to a 6.625 and have the lender pay some of your closing costs. Your payment is going to be a little bit higher, but you just reduced the amount of cash you needed at close. All of those options are still on the table because you locked the sheet, not just one rate.

Nine times out of ten, buyers want to lock as soon as they go in contract. Letting the rate float during escrow requires a tolerance for uncertainty that most buyers do not have, and the potential upside is rarely worth the risk.

What Happens When It Expires

If the loan does not fund before the rate lock expires, the lock is gone. From the lender’s perspective, funding is the finish line, not recording. If the lock expires before the loan funds, you are repriced at whatever the market is doing that day. That is a problem if rates moved against you during escrow.

Extensions are available, but they come at a cost. Extending a rate lock runs anywhere from $100 to $300 per day. Some lenders include free 3- or 5-day extensions as part of their broker relationship, and a good loan officer factors that into the timing conversation at the start. Who pays for an extension depends on who caused the delay. A seller delay is a concession conversation. A buyer delay is a cost that falls on the borrower.

This is all expectation setting and proper date management on our side. The lock expiration should never be a surprise — a good loan officer is watching those dates from the moment you lock, and if a transaction is running close to the wire, that conversation needs to happen before an extension becomes the only option.

The Bigger Picture

A rate lock is not just paperwork. It is a time-sensitive contract with real consequences on both ends. Locking at the right time protects you from rate movement during escrow. Choosing the right lock period saves money on pricing. And revisiting the rate sheet before final docs gives you flexibility that most buyers do not know they have going in.

If you are getting ready to make offers, or already in contract and have questions about where rates are and what a lock looks like right now, that is a ten-minute conversation.

Rates shown are for illustrative purposes only and do not represent current available rates. Contact Glenn Groves for current rate information.

Glenn Groves

Mortgage Broker | GTG Financial | Santa Rosa, CA

NMLS #1124642 | gtgfi.com

GTG Financial, Inc. NMLS #1595076 | CA DRE #02029711. Equal Housing Opportunity. Not a commitment to lend. Subject to credit approval and underwriting. Individual results vary based on credit profile, loan amount, property type, and other factors. nmls consumeraccess.org

Related Posts