Introduction As we move deeper into the summer months, the real estate market often experiences…

Earnest Money Deposit

July 2026 | GTG Financial | Santa Rosa, CA

Earnest Money Deposit: What It Is, and When You Could Lose It

An earnest money deposit is a good faith deposit, usually 1 to 3% of the offer price, that you put down when you make an offer on a home. It goes into a neutral escrow account the seller cannot touch, and it is released as you clear your contingencies. If you back out after those protections are gone, the seller can keep it.

Reviewed by Glenn Groves, Mortgage Broker, NMLS #1124642 · GTG Financial, Inc. NMLS #1595076 · Serving Sonoma, Marin, and the greater North Bay.

TL;DR: What’s in This Post

- What an earnest money deposit is and how much it runs

- Where the money goes and who controls it

- How it’s released through your contingencies

- The one scenario where you can actually lose it

- A simple table: do you get your deposit back?

Making an offer on a home means putting real money on the table before you own anything, and that catches a lot of first-time buyers off guard. The earnest money deposit is the part that tends to cause the most worry. Here is exactly what it is, where it goes, and the one situation where you could actually lose it.

What Is an Earnest Money Deposit?

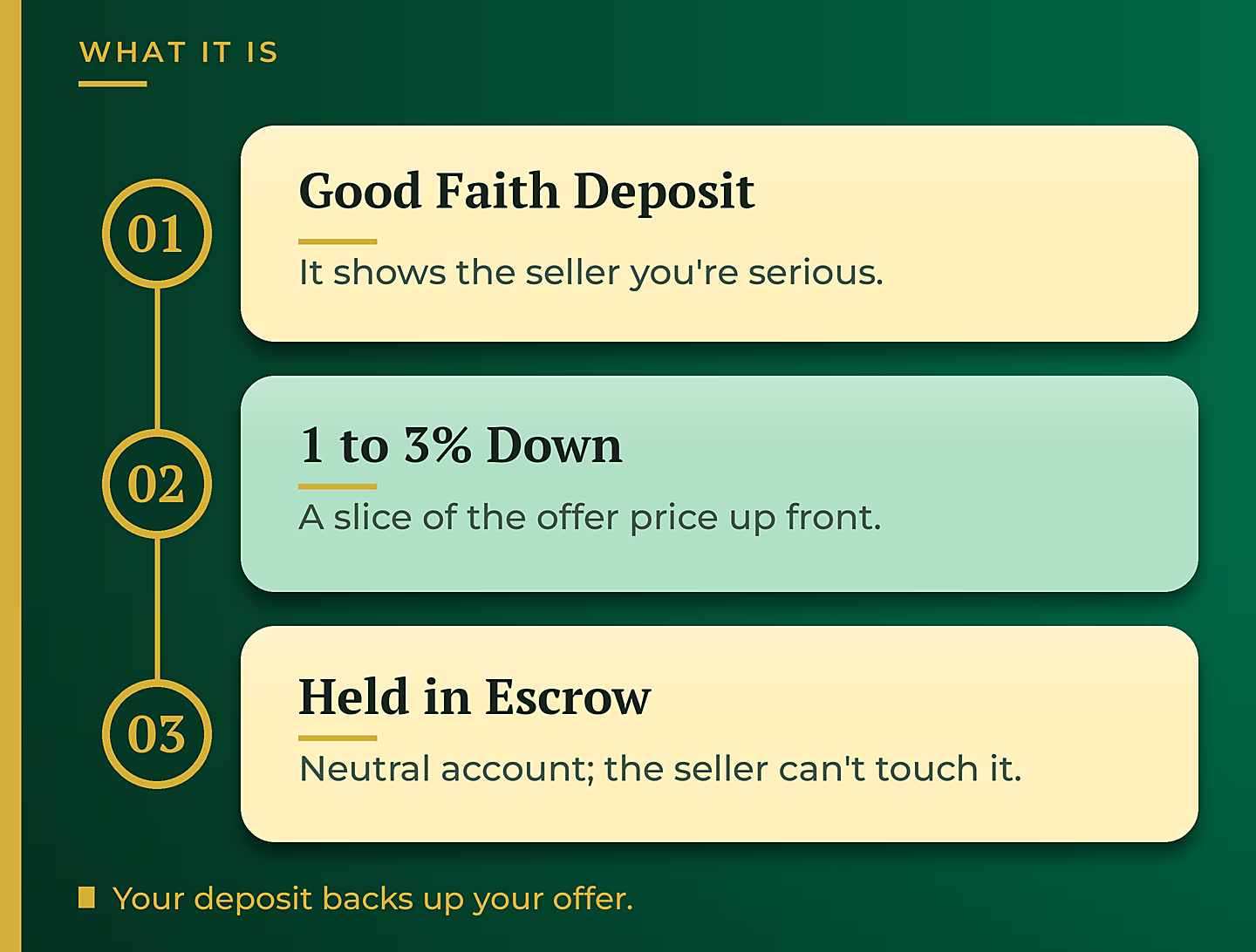

An earnest money deposit is a good faith deposit that shows the seller you are serious about your offer. It typically runs anywhere from 1 to 3% of the offer price. On an $800,000 home, which is around the average in much of the North Bay, that is roughly $8,000 to $24,000 put down up front.

That money does not go to the seller. It goes into a neutral third-party account with escrow, and the seller cannot touch it. A lot of first-time buyers get spooked here. They look at the number and think, wait, I have to deposit $20,000 when I have only seen the house twice? That reaction is completely normal, and understanding how the deposit works usually settles the nerves.

How Your Deposit Is Released

Your deposit slowly comes into play as you release your safety nets, which are your contingencies. The big three are inspection, appraisal, and loan. In plain terms: is the house in the shape you thought it was, is it worth what you thought it was, and can you actually qualify for the loan?

As you clear each of those checkpoints, you get closer to closing and your deposit becomes more firmly committed. This is the mechanism that protects you. As long as you are still inside one of those contingencies, you have a reason to walk away and keep your deposit.

Do You Get Your Earnest Money Deposit Back?

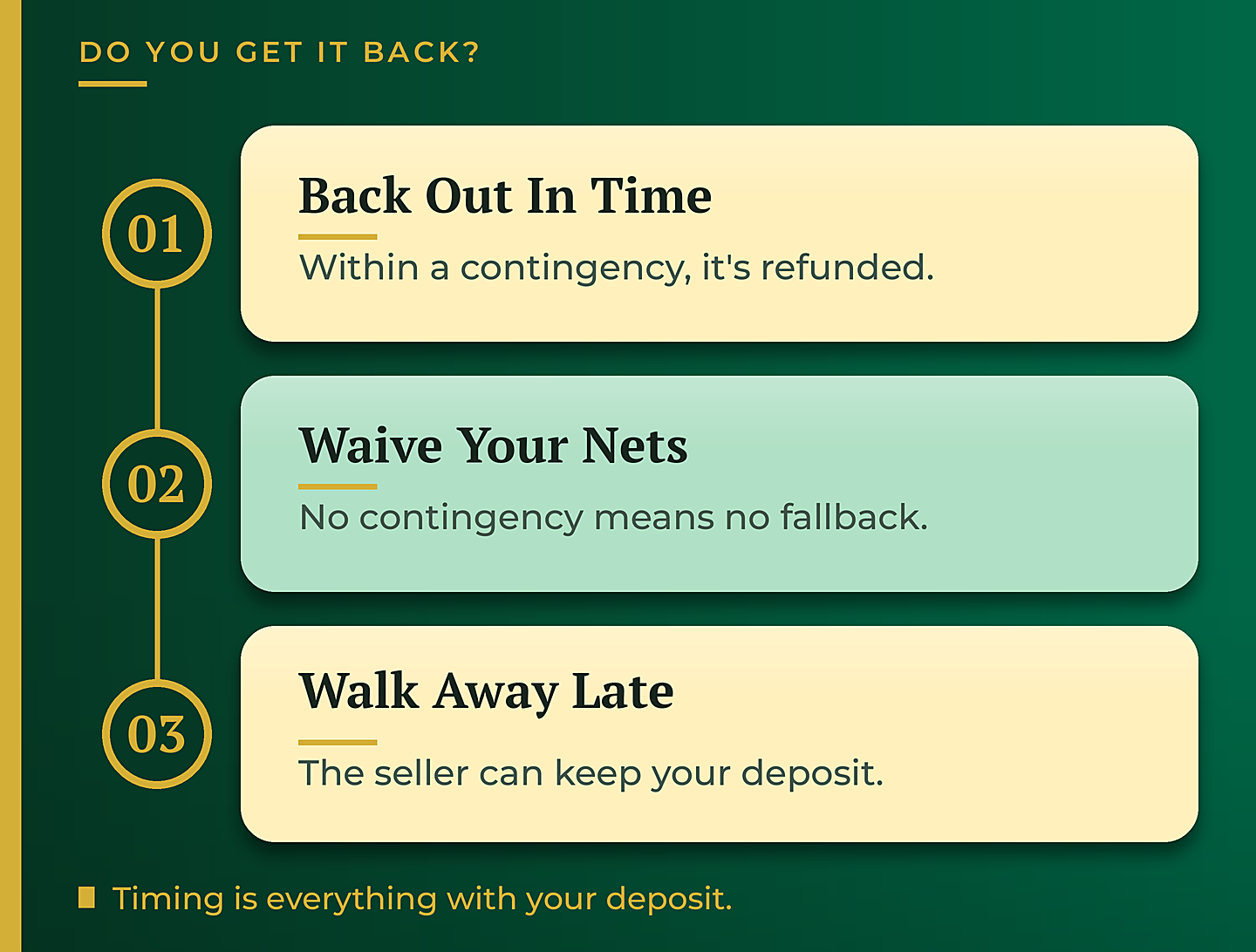

This is the question every buyer really wants answered. The short version: it depends on whether you back out while a contingency still protects you. Here is how the common scenarios play out.

| Situation | What happens to your deposit |

|---|---|

| Inspection turns up problems (contingency active) | You can back out and it is refunded |

| Appraisal comes in low (contingency active) | You can renegotiate or walk and keep it |

| Loan falls through (contingency active) | You can back out and it is refunded |

| You walk after releasing your contingencies | The seller can legally keep your deposit |

In other words, if the house checks out, the appraisal comes in, you are approved for the loan, and then at the 11th hour you decide you do not want to buy, the seller has every legal right to keep that deposit. But back out while a contingency still protects you, and you are covered.

Why the Deposit Is Worth Understanding

The earnest money deposit is not a fee and it is not lost money. In almost every normal transaction it becomes part of your down payment and closing costs at the end. The risk only appears if you waive your contingencies to make a more aggressive offer, or if you walk away late for a reason that is not protected.

That is why the deposit and your contingencies are really one conversation. The deposit is what is at stake, and the contingencies are the safety nets that protect it. Knowing exactly where you stand at each step is what keeps your money safe and your offer strong.

Frequently Asked Questions

What is an earnest money deposit?

It is a good faith deposit you put down when you make an offer on a home, usually 1 to 3% of the offer price. It shows the seller you are serious and is held in a neutral escrow account until closing.

How much is an earnest money deposit?

It typically runs 1 to 3% of the offer price. On an $800,000 home, that is roughly $8,000 to $24,000, though the exact amount varies by offer and by how competitive the market is.

Do you get your earnest money deposit back?

Usually yes, if you back out while a contingency still protects you, such as a failed inspection, a low appraisal, or a loan that falls through. If you walk away after releasing your contingencies, the seller can legally keep the deposit.

Where does the earnest money go?

It goes into a neutral third-party escrow account. The seller cannot touch it, and in a normal closing it is applied toward your down payment and closing costs.

The Bigger Picture

An earnest money deposit can feel intimidating, but it is really just proof that you mean business, held safely in escrow while your contingencies do their job. Understand how it is released and when it is at risk, and the number stops being scary.

If you are getting ready to make an offer and want to know exactly how your deposit and contingencies will work, reach out and we will walk you through it before you sign anything.

Glenn Groves

Mortgage Broker | GTG Financial | Santa Rosa, CA

NMLS #1124642 | gtgfi.com

This article is for educational purposes and is not legal or financial advice. Earnest money is at risk if you back out of a purchase without an active contingency; deposit amounts, contingency terms, and refund rights vary by offer, contract, and situation. Consult your real estate agent and a qualified professional about your specific transaction. Glenn Groves NMLS #1124642 | GTG Financial, Inc. NMLS #1595076 | CA DRE #02029711. Equal Housing Opportunity. Not a commitment to lend. nmls consumeraccess.org

Related Posts