Introduction As the end of July approaches, many families are preparing for the back-to-school season.…

Keep Your Rate and Buy Up

June 2026 | GTG Financial | Santa Rosa, CA

TL;DR: What’s in This Post

- How a client kept their COVID-era rate and still bought a new primary in Napa

- What lenders actually require to use rental income from a departing residence

- Why you cannot use a relative to sign the lease agreement

- How 75% of rental income factors into qualifying for the new loan

You cannot take your interest rate with you to a new home. But you do not have to give it up either. This deal is a good example of what is possible when the plan is set correctly going in.

The Deal

A client came to us wanting to purchase a home in Napa at $979,000 with 5% down. That puts us in high balance territory, but same guidelines apply. The unique piece of this deal is that they were going to keep their existing property in Santa Rosa and convert it to a rental while moving to Napa.

The reason they wanted to keep the Santa Rosa property: they originally purchased it in 2018 and we refinanced them during COVID into a very low interest rate. They cannot take that rate with them to the Napa home, but they are not willing to give up that asset with its low payment. The plan was to keep it, rent it out, and go cash flow positive while purchasing a new primary residence.

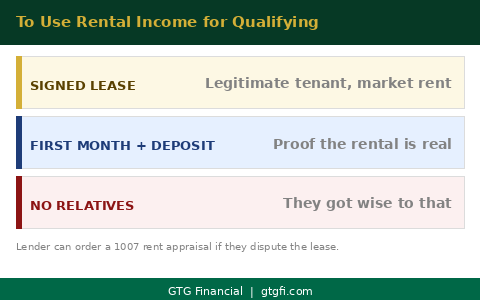

What the Lender Requires

When you are retaining a property and using rental income to offset its mortgage, the lender needs proof the rental is legitimate. That means a signed lease agreement, the first month’s deposit, and the security deposit in hand before closing.

And you cannot have a relative just sign a lease agreement. Lenders got wise to that a long time ago. If the fair market rent on a property is around $3,000 a month and you show up with a $6,000 lease from a family member, they are going to look at who the renter is. They can also order what is called a 1007, which is a schedule of rent appraisal on the departing residence, if they do not agree with the lease you have provided. The rent has to be legitimate and at market rate.

How the Numbers Work

The departing residence adds complexity to qualifying because the lender still counts that mortgage payment against you. The principal, interest, taxes, and insurance on the Santa Rosa property all have to be accounted for. To offset it, we need the rental agreement in place and showing that the rental income covers it.

One important detail: lenders only allow 75% of the rental income to count toward qualifying. So if the property rents for $3,000, we can use $2,250 of that against the departing residence mortgage. In this case the numbers work, but this is exactly why the plan has to be set from the beginning with everyone aware of how the dominoes need to fall.

The result: cash flow positive on the Santa Rosa asset and a new primary residence in Napa at 5% down.

They can’t take their interest rate with them to the new house, but they don’t want to get rid of that asset with the really low payment on it.

If you are sitting on a property with a low interest rate and wondering if there is a way to keep it and still buy up, reach out. That conversation starts with understanding whether the numbers work for your specific situation, and it is worth having before you assume you have to sell.

Glenn Groves

Mortgage Broker | GTG Financial | Santa Rosa, CA

NMLS #1124642 | gtgfi.com

GTG Financial, Inc. NMLS #1595076 | CA DRE #02029711. Equal Housing Opportunity. Not a commitment to lend. Subject to credit approval and underwriting. Individual results vary based on credit profile, loan amount, property type, and other factors. nmls consumeraccess.org

Related Posts