Introduction As June unfolds and summer is in full swing, many families are considering making…

Self-Employed Borrowers and the Write-Off Trap

June 2026 | GTG Financial | Santa Rosa, CA

TL;DR: What’s in This Post

- Why writing off income on your taxes can work against you when qualifying for a mortgage

- What a bank statement loan is and who it is actually designed for

- How to run the math on whether keeping your write-offs still makes sense

- What to do if you are self-employed and not ready to buy yet

If you are self-employed and trying to buy a home, the same discipline that keeps your tax bill low can be the exact thing standing between you and a mortgage approval. Understanding how lenders look at your income is the first step to navigating it correctly.

The Write-Off Trap

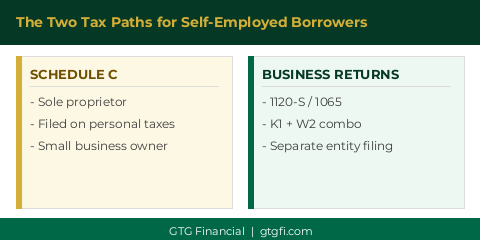

When you are self-employed, you typically fall into one of two filing categories. Either you file a Schedule C as a sole proprietor on your personal taxes, or you have a separate set of business tax returns, such as a 1065 or 1120-S. Either way, the door is wide open to have business expenses and write things off against your income.

That is a great thing come tax time. Less taxable income means less taxes paid. The double-edged sword is that it also means less qualifying income when a lender is reviewing your mortgage application. The number you declared as net income is not necessarily the end of the story. Depending on whether we are looking at a Fannie Mae, Freddie Mac, VA, FHA, or jumbo product, the rules on what can be added back vary. Depreciation, for example, is often an allowable add-back. But the more aggressively you have written things off, the more work it takes to get you to a qualifying number.

The Bank Statement Loan Alternative

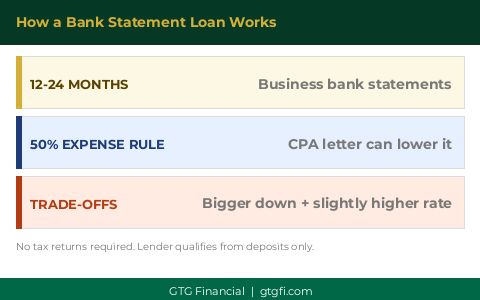

When the tax returns do not get you where you need to be, a bank statement loan is the most common alternative. Instead of reviewing your tax returns, the lender looks at 12 to 24 months of business bank statements and calculates your income based on total deposits. Tax returns are not part of the picture at this point.

The default assumption is that 50% of your deposits are expenses. So if you brought in $200,000 in deposits over the year, the lender uses $100,000 as your qualifying income. That number can often be improved. If your CPA provides a letter confirming that your actual expense ratio is lower, say 20 or 30%, the lender will factor that in and qualify you on a higher income figure.

The trade-off is real. Bank statement loans typically require a larger down payment, which can close the door on 3, 5, or sometimes 10% down products. And the interest rate will be somewhat higher than a conventional loan. That said, the program exists for a reason, and for the right borrower it is the right tool.

Running the Math on Your Write-Offs

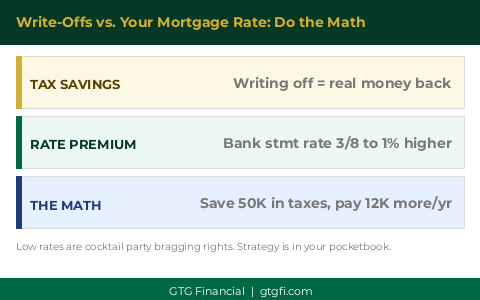

Here is where a lot of self-employed buyers get the strategy backwards. They hear that their bank statement loan rate is going to be a half percent or a full percent higher than a conventional loan, and they focus on that number. But the question worth asking is how much are you saving in taxes by writing everything off?

If writing off a significant portion of your income is saving you 40 or 50 thousand dollars a year in taxes, and the higher rate on a bank statement loan costs you an extra 12 thousand a year on your mortgage payment, the math still works heavily in your favor. Keep writing things off. The rate is a cocktail party number. What you feel in your wallet is the strategy.

On the other hand, if you are saving six thousand dollars in taxes by writing things off, but the higher mortgage rate costs you twelve thousand more per year, that is a different conversation entirely. The right answer depends on your specific numbers, which is exactly why it should be a conversation with your mortgage professional before you decide how to file.

Low rates are cocktail party bragging rights. What you’re actually feeling in your wallet, in your pocketbook, that’s the strategy we’re going after.

If you are self-employed and not sure whether you are ready to buy, the right move is still to have a mortgage professional look at your taxes now. This can easily be a two or three year process of setting things up correctly. The earlier you have that conversation, the more options you have going in.

Glenn Groves

Mortgage Broker | GTG Financial | Santa Rosa, CA

NMLS #1124642 | gtgfi.com

GTG Financial, Inc. NMLS #1595076 | CA DRE #02029711. Equal Housing Opportunity. Not a commitment to lend. Subject to credit approval and underwriting. Individual results vary based on credit profile, loan amount, property type, and other factors. nmls consumeraccess.org

Related Posts